ETF Tracker StatSheet

You can view the latest version here.

Treading Water

- Moving the markets

Throughout the past week, the major indexes having been treading water, and today was no exception. The S&P 500, while peeking again into record territory, managed to eke out a weekly gain of 0.37%. During this session, we saw the index pump, dump, and pump again before fading into the close.

As was to be expected, yesterday’s poor CPI report was still on traders’ minds, with one technical analyst from Piper Sandler attempting to put a lipstick on that pig:

While the May CPI report came in above estimates, the market was not too surprised and digested the data as transitory for now, the Treasury market appeared to be in agreement with the temporary inflation outlook.

Sure, it was confusing to see the bond market’s lack of recognition of these inflationary trends yesterday, as yields were dropping instead of rising, which would have been a normal reaction. However, the power of the Fed’s resolve that these current tendencies are to be considered “transitory” is a view that pleases Wall Street and therefore has contributed to the continued ramp in equities and the plunge in bond yields.

While “growth” and “value” moved in sync today, for the week “growth” came out ahead, but YTD, “value” still remains the winner.

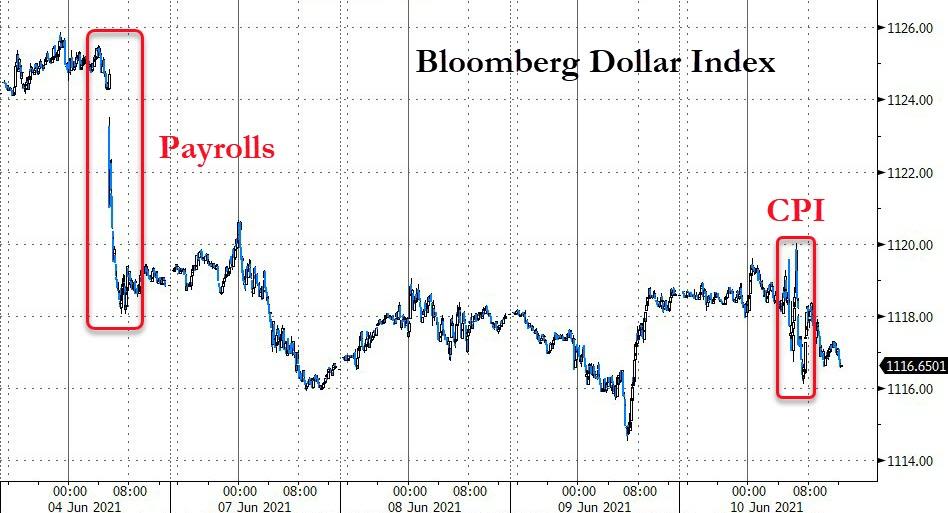

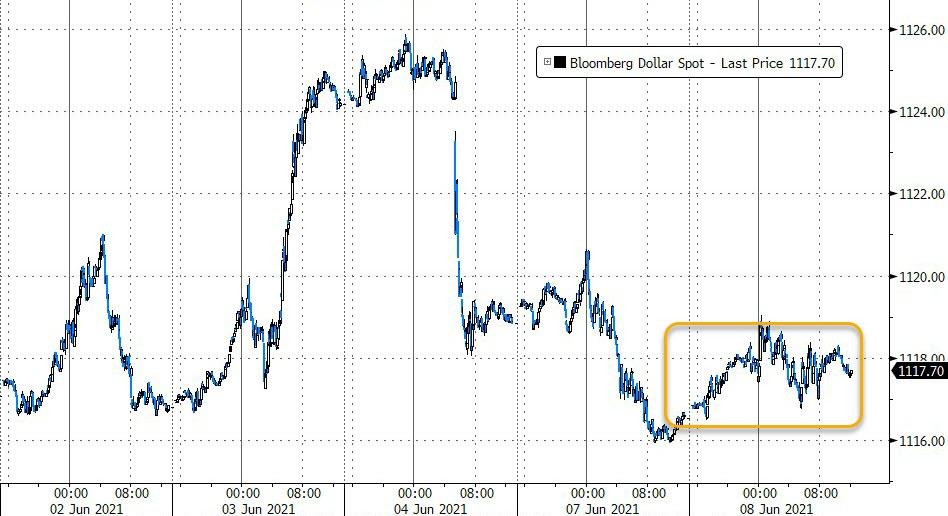

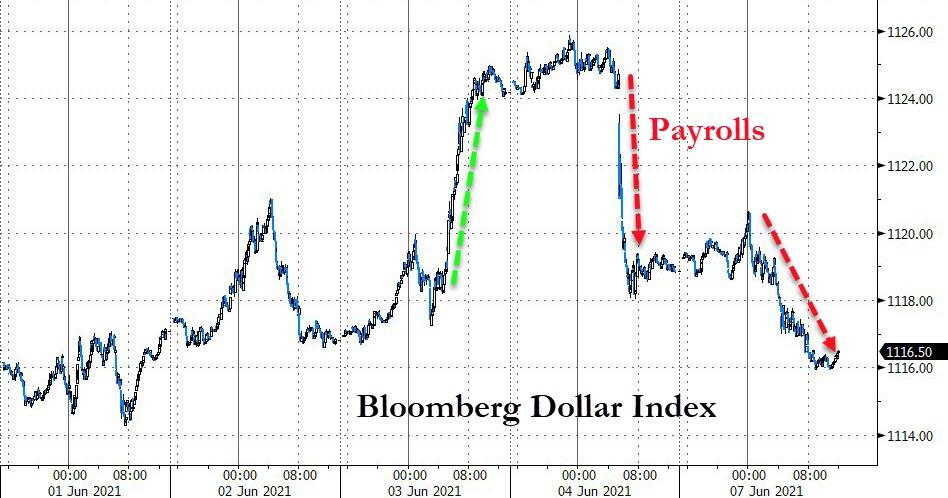

Over the past five trading days, bond yields collapsed the most in a year, as ZeroHedge pointed out, with the 10-year now reaching a level last seen the beginning of March. The US Dollar Index, after meandering all week, spiked sharply. That came as a surprise as lower yields usually pull the dollar down, but it goes to show you how much things are out of whack.

The fallout from the dollar’s surge was Gold, which got slammed by almost 1% with the precious metal again losing its $1,900 level.

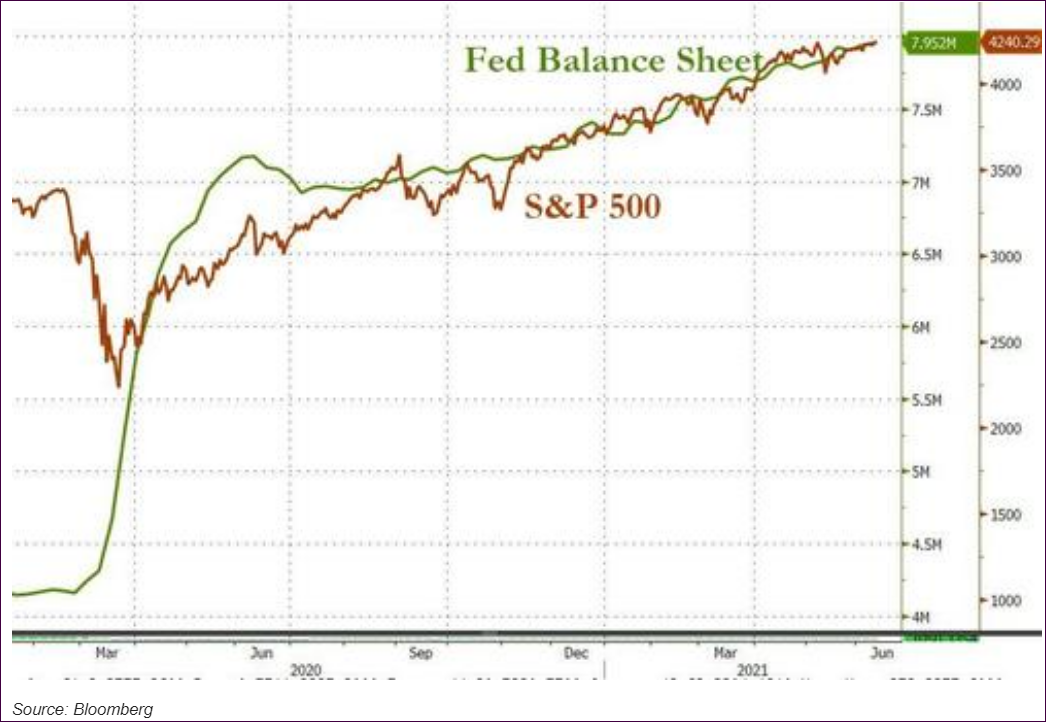

Assisting the S&P 500 in making new highs is the fact that the Fed’s balance sheet continues to expand. It has reached almost $8 trillion this week, for the first time ever, and has basically doubled since the pandemic panic response, as ZeroHedge pointed out:

And this reckless monetary expansion continues to go on, despite the collapse of Covid, leaving me pondering “what’s next?”

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}