ETF Tracker Newsletter For June 26, 2026

ETF Tracker StatSheet

You can view the latest version here.

AI JITTERS SHAKE GLOBAL MARKETS AS TECH SELLOFF PICKS UP SPEED

- Moving the market

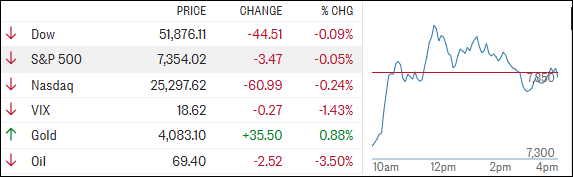

The S&P 500 started the session pretty flat, but the tone quickly shifted as concerns around AI spending picked up steam.

Reports that OpenAI may delay its IPO raised eyebrows, especially since it hints at slower access to capital — and potentially less aggressive infrastructure spending going forward.

That uncertainty spilled over into the broader tech space, where selling pressure really started to build. The hit was felt globally, but Asia took it the hardest.

SoftBank, a major OpenAI backer, led the slide with a sharp 12% drop. South Korea wasn’t spared either, with the Kospi tumbling nearly 6% and the Kosdaq falling about 4% as the tech rout spread across the region.

Europe followed suit, with major indices finishing lower as the global tech selloff deepened.

Adding to the uneasy mood, shifting expectations around Fed policy — not just what they might do next, but why — have created a backdrop that feels ripe for ongoing volatility.

That said, it’s not all gloom. Better-than-expected consumer sentiment and a more favorable inflation outlook offered a bit of support and helped steady nerves somewhat.

Zooming out, the market story this year is more nuanced than it might seem. While mega-cap tech has had a strong run, the equal-weighted S&P 500 is actually outperforming — a sign that gains have been broader than just the usual big names.

For the week, oil took a hit but showed signs of life with some late volatility. The Nasdaq dropped about 4%, weighed down heavily by sharp losses in the Mag 7, while the Dow and Russell 2000 held up better. Bond yields moved lower across the board, while the dollar pushed higher overall despite some recent softness.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

In other corners, Bitcoin slipped below $60K and is now testing key support levels from early June, while gold continues to hover near the $4,000 mark.

{kind=link}

One thing to keep in mind: this market is increasingly being driven by leverage. A lot of the recent upside — especially in AI-linked names — came from aggressive positioning through options and leveraged ETFs.

That works great on the way up, but it can just as quickly amplify the downside when sentiment shifts.

My big question is: if enthusiasm around AI starts to cool, how much of this market strength can actually hold up?

Read More