[Chart courtesy of MarketWatch.com]

- Moving the market

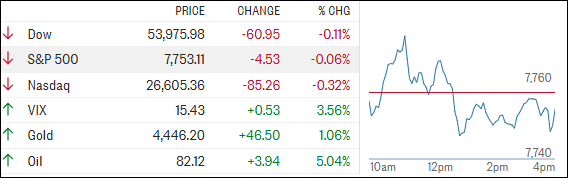

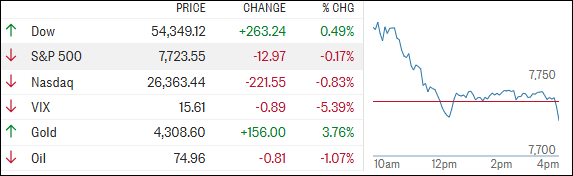

Markets spent most of the day waiting for clarity on the Iran situation and, unfortunately, clarity never showed up for work.

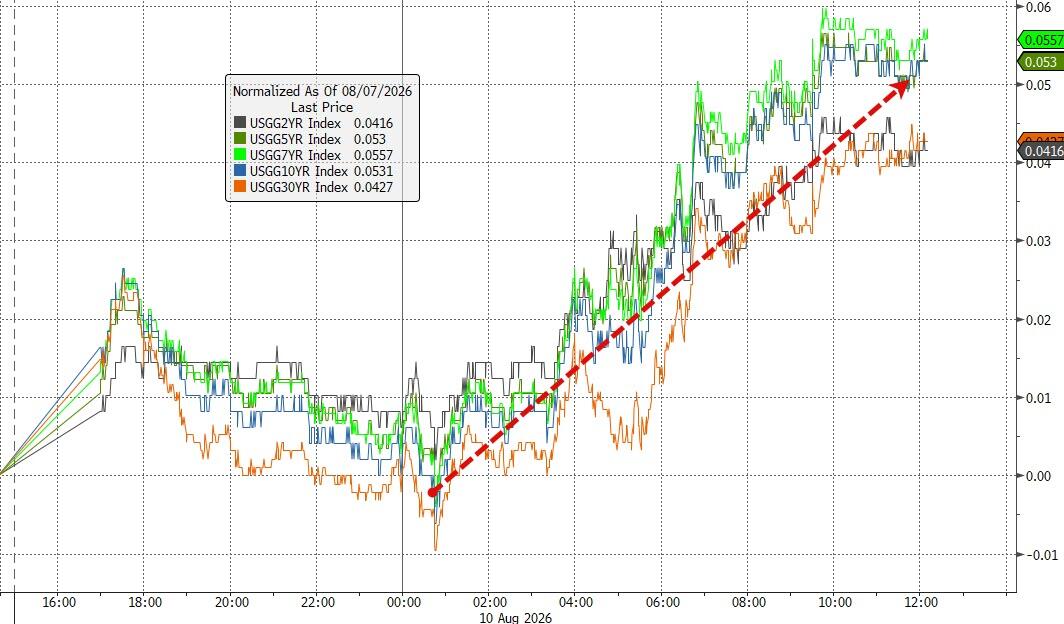

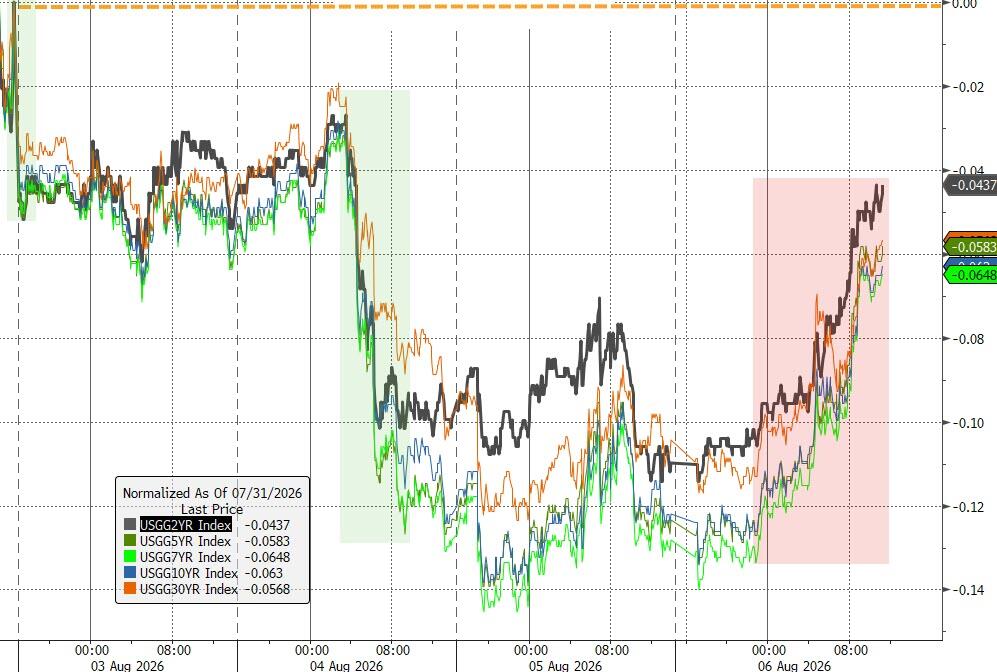

Growing doubts about a near-term U.S.-Iran breakthrough kept investors cautious, while higher oil prices took center stage. With WTI crude jumping about 5% to $82, bond yields moved higher and risk appetite cooled.

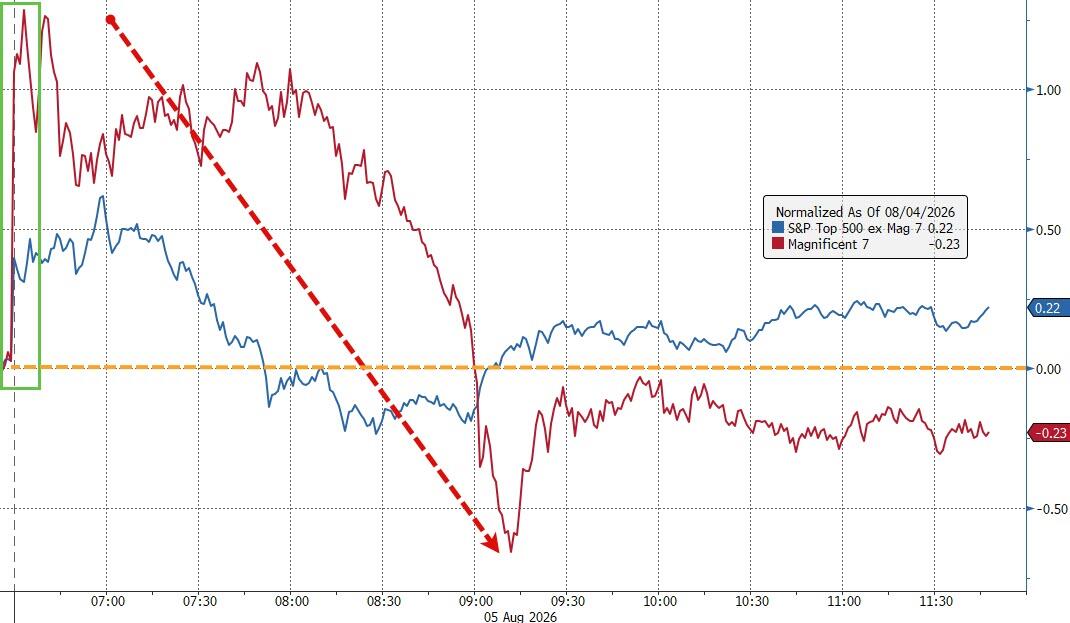

The major indexes drifted lower as the recent short-covering rally appeared to run out of fuel.

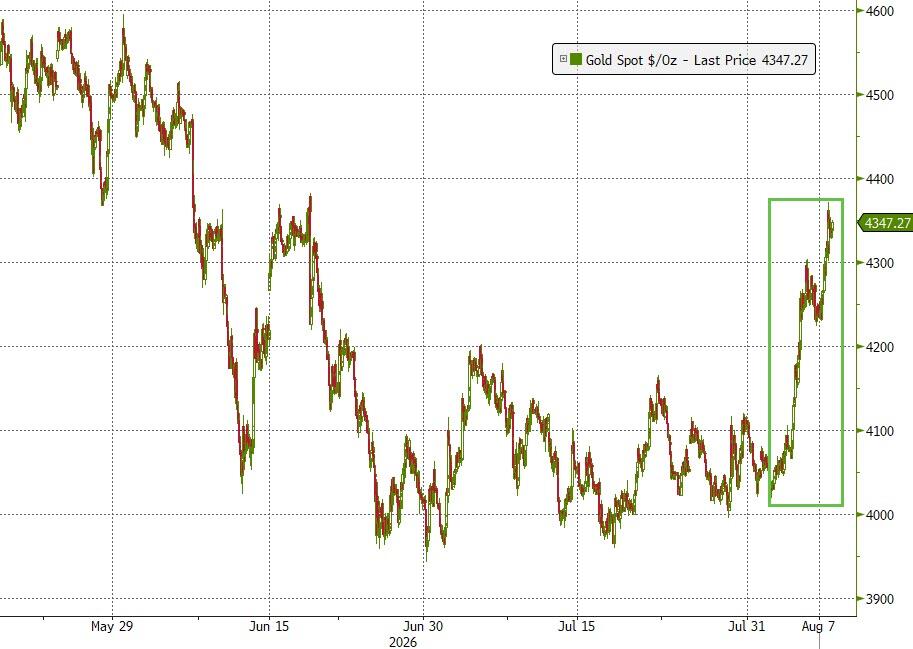

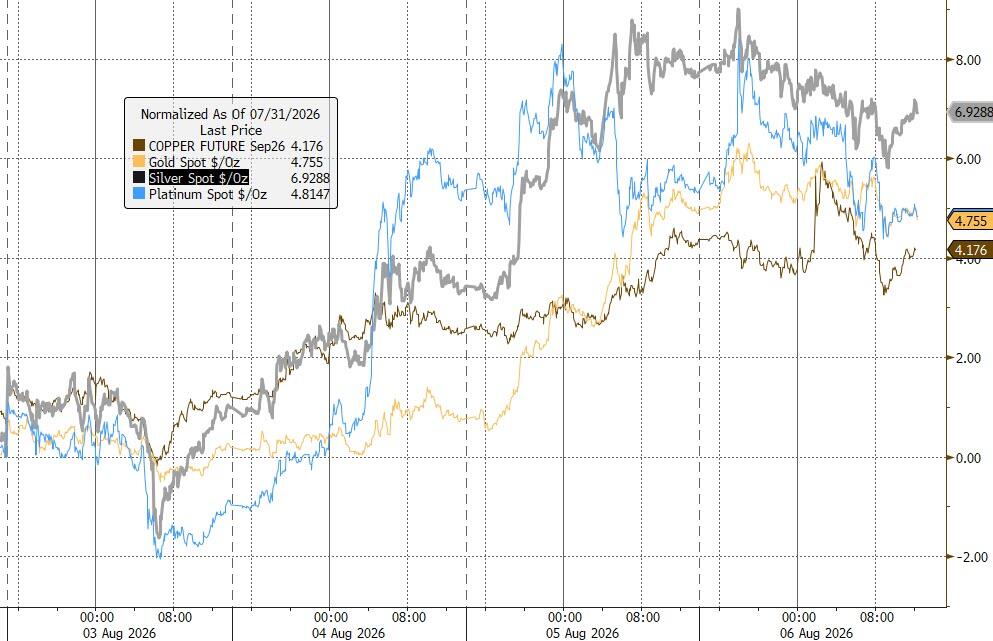

Meanwhile, precious metals continued to attract attention. Gold pushed back above $4,350 despite a stronger dollar, while silver stole the spotlight with a gain of more than 3%.

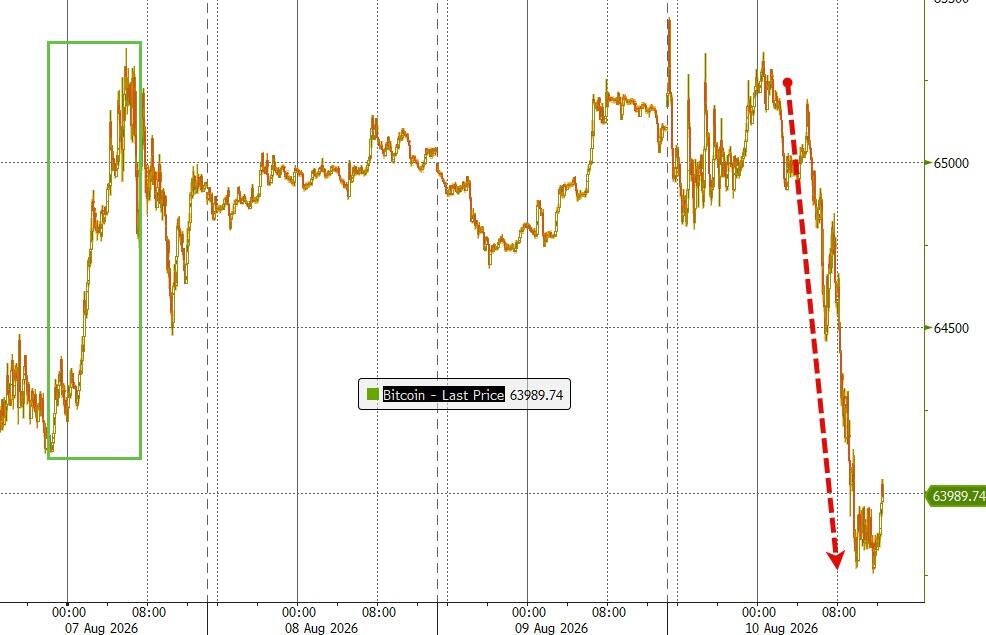

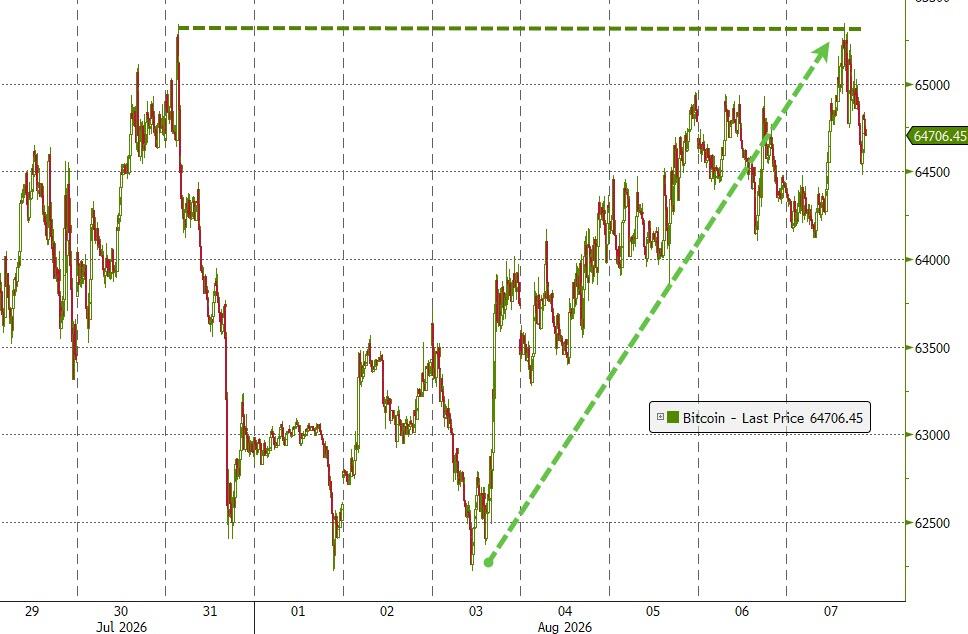

Bitcoin was the outlier, slipping modestly below $64,000.

In the end, it felt like one of those market days where everyone was waiting for the next headline, and nobody wanted to make the first big move.

Until a new catalyst emerges, we may be stuck in a holding pattern.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}