ETF Tracker StatSheet

You can view the latest version here.

REALITY DOMINATES OPTIMISM

- Moving the markets

Optimistic traders, who followed the latest firehose of news headlines and pushed the major indexes higher at the opening, had to face reality eventually, because actual happenings erased the early enthusiasm.

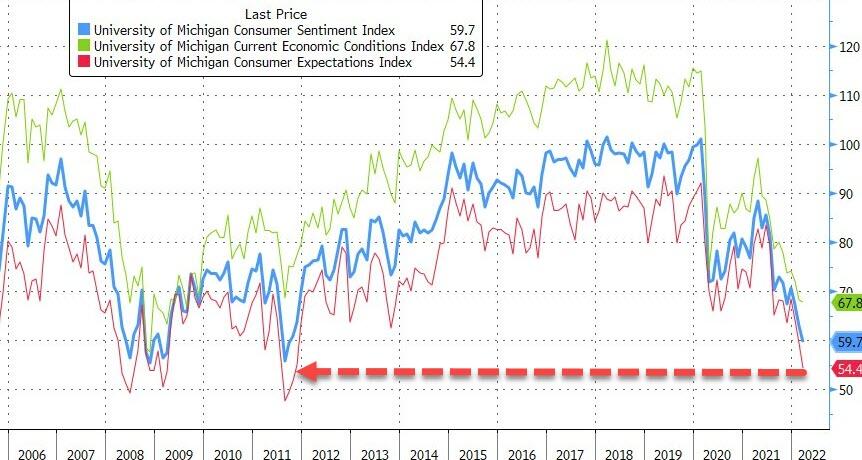

Not helping matters was the fact that the number of unhappy Americans had increased, as measured by the US Sentiment index. Joined by current economic conditions and inflation expectations, the numbers dropped to lows last seen in 2011, as this chart by Bloomberg shows.

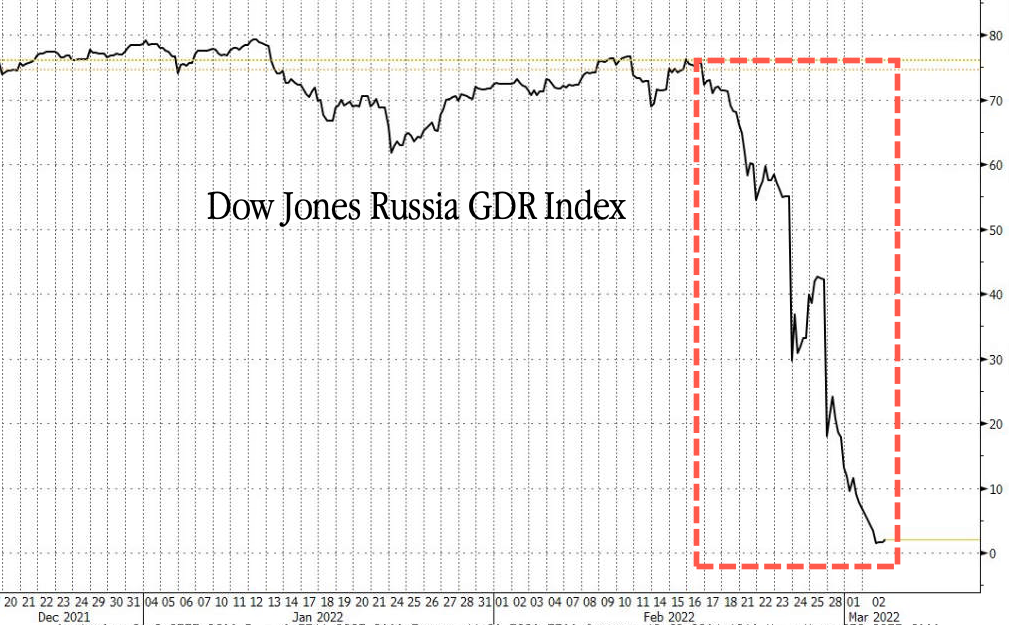

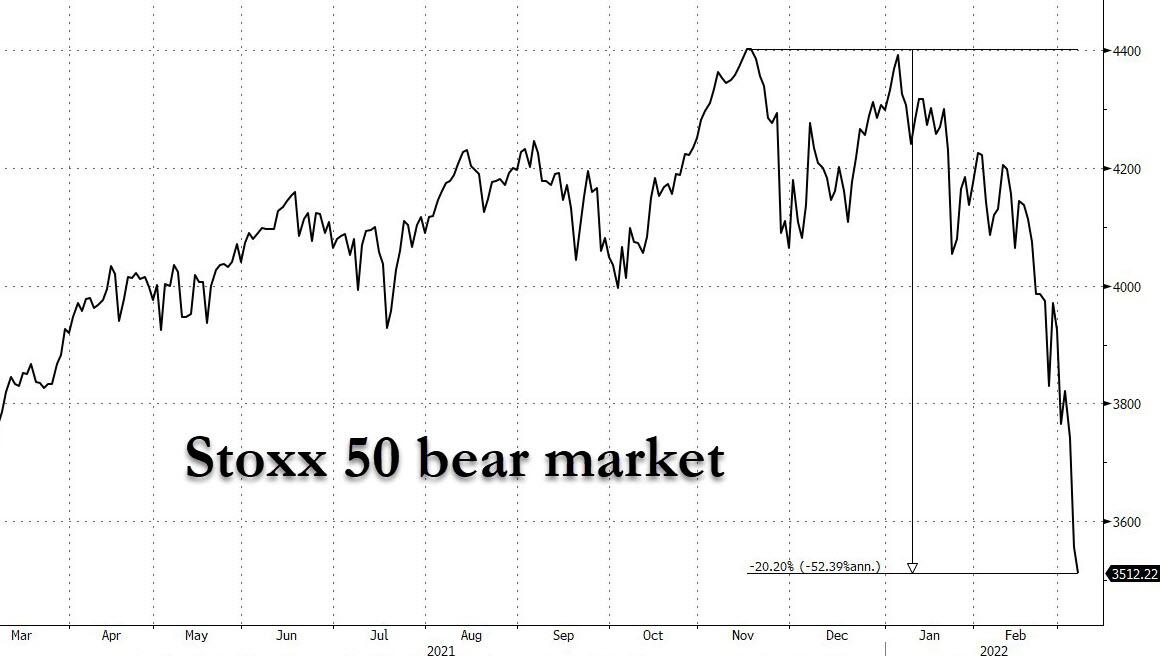

That translated into another early rally biting the dust with the Dow notching its 5th straight week of losses due to the Russia-Ukraine war uncertainties keeping the bears in charge.

Added MarketWatch:

Russian President Vladimir Putin said Friday “certain positive shifts” have occurred in the talks between the Kremlin and Ukraine, however, a ceasefire has not been negotiated. Meanwhile, President Volodymyr Zelenskyy reportedly said Ukraine has reached a “strategic turning point” in its war with Russia.

In other words, nothing has been resolved and the adage that “hope is not an investment strategy” was validated again. For the week, the Dow lost 2%, the S&P 500 dropped 2.9%, and the Nasdaq fared the worst by giving back 3.5%.

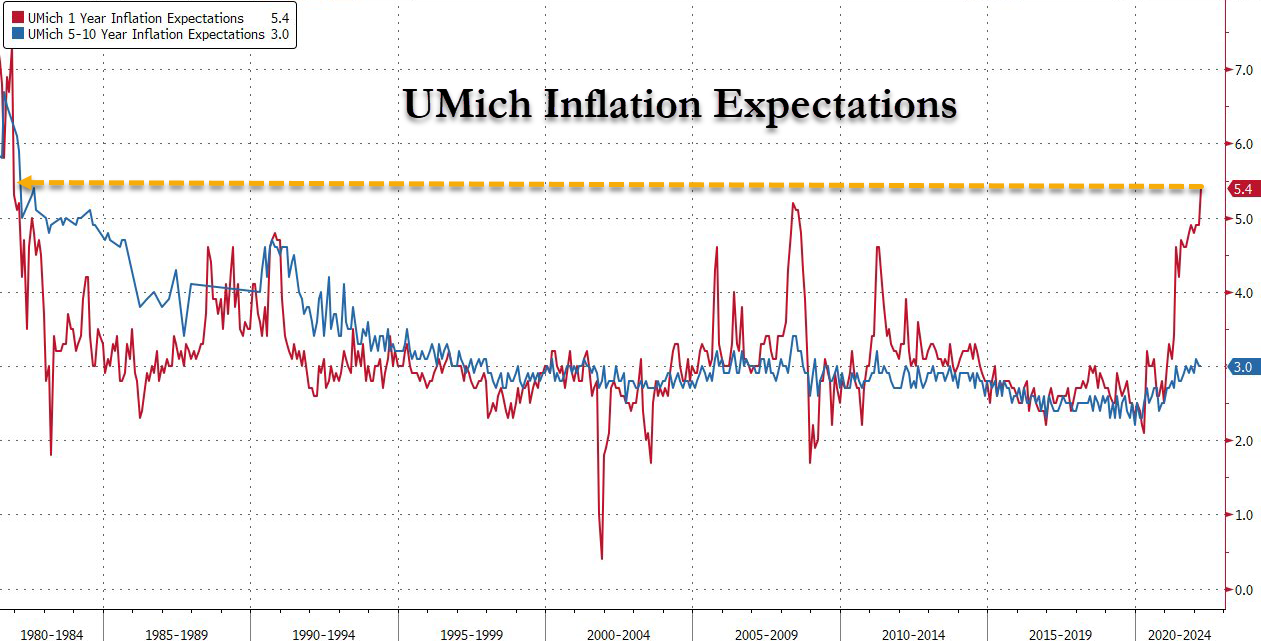

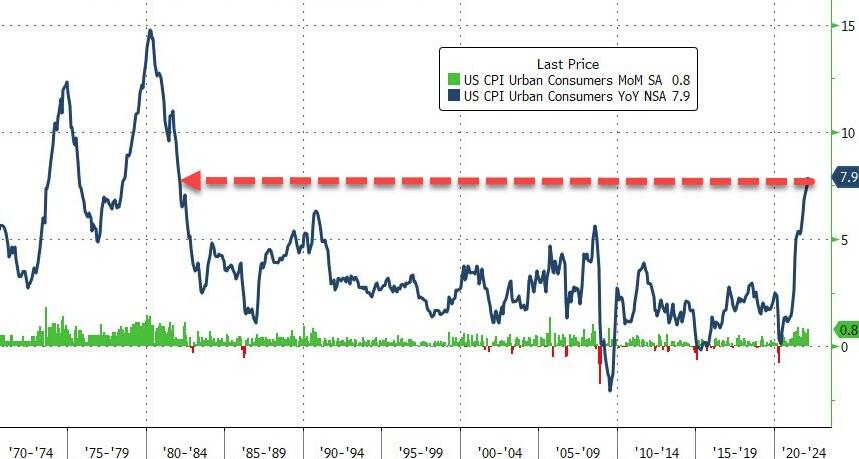

Some biased news reports are now pushing the narrative that YoY consumer price increases were Putin’s fault, a notion that was quickly dismissed and supported by this chart.

While bond yields soared in Europe all week, the situation was not much better here in the US, where yields as well spiked higher thereby causing bond prices to crumble. This turned into a nightmare for those holding bonds to offset equity weakness, a theory that has bit the dust on many occasions in the recent past.

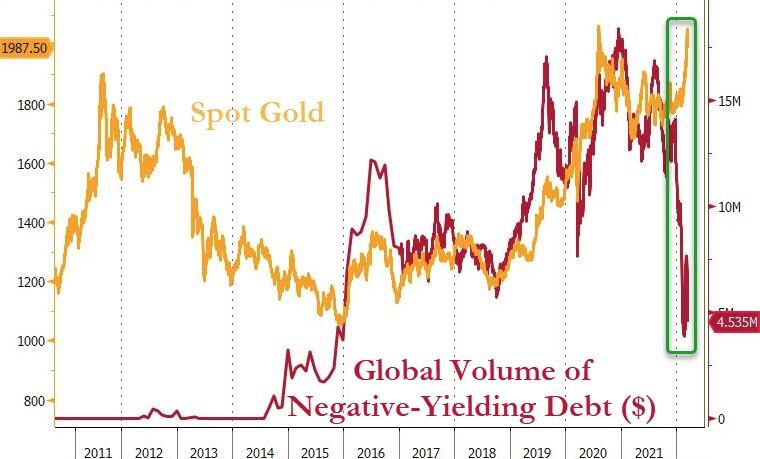

Gold slipped early on, rebounded but still lost its $2k level by a small margin, but it remains the real “safe haven” once again, as negative yielding debt worldwide is simply not the place to be.

After all, would you loan someone $100, with him promising to pay you back $98? That’s what negative yielding debt translates into.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}