1. Moving the Markets

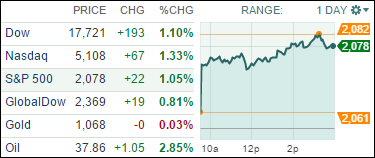

Stocks skyrocketed as traders remain hopeful that a year-end ‘Santa Claus rally’ will finally push the major indexes back into positive territory for the year and avoid Wall Street’s first down year since 2008. Investors remain cautious though, as the so-called rally from Saint Nick, may not have yet completely taken flight.

Of course, as we’ve seen in the recent past, equities are tied to the fortunes of oil, which rallied today and pulled the indexes higher. Not much has been gained over the past 2 months despite the S&P closing at 2078 today, which is still 2 points below the price it ended November and 1 point below the price we closed at in October. In other words, the market is just making up previous losses.

Nevertheless, Wall Street is hoping that a year-end rally holds, because if it doesn’t, there’s a good chance that both the Dow and S&P 500 could suffer their first calendar year decline since 2008 when stocks fell more than 30%.

We heard some positive news in the housing market today for investors, but maybe not for future home buyers. U.S. home prices rose 5.2% in October, compared to a year earlier. The housing market appears to be maintaining momentum, according to a key benchmark released Tuesday. The major markets that stood out on rising prices were Denver, Portland and San Francisco. At the bottom of the totem pole was Chicago, Washington D.C. and Cleveland.

And finally, energy stocks bounced back today, led by Chesapeake Energy Corp (CHK) and Consol Energy Inc (CNX).

All of our 10 ETFs in the Spotlight joined the party, with the leader being Healthcare (XLV) with +1.22%, while the Select Dividend ETF (DVY) lagged with +0.61%.

State Street Global Advisors (SSgA), a unit of State Street and the asset manager behind the iconic SPDR S&P 500 ETF (SPY), recently launched an equity fund dedicated to tracking the performance of the biggest dividend paying stocks listed in the US.

State Street Global Advisors (SSgA), a unit of State Street and the asset manager behind the iconic SPDR S&P 500 ETF (SPY), recently launched an equity fund dedicated to tracking the performance of the biggest dividend paying stocks listed in the US.