- Moving the market

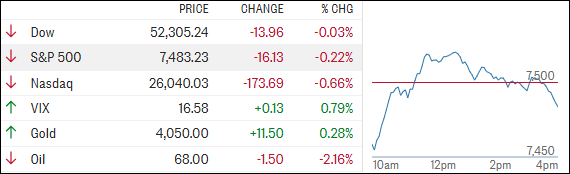

Semiconductor stocks took a breather today, putting early pressure on the Nasdaq after an exceptionally strong first half of the year.

Micron slid 6% and Sandisk dropped 8%, although both remain sharply higher for the year. Nvidia and Broadcom also finished lower, down roughly 2% and 1%, respectively.

The weakness appeared to be driven largely by profit-taking as traders locked in gains following the sector’s remarkable run.

Chipmakers and AI-related stocks have been major drivers of the market’s impressive performance during the first half of 2026, and Tuesday’s rally only added to the group’s momentum. In fact, the second-quarter semiconductor surge added an estimated $2 trillion in market value across companies such as Micron, Intel, and AMD.

Investors also kept a close eye on the Federal Reserve. Speaking at the European Central Bank conference in Portugal, Fed Chairman Kevin Warsh offered little insight into the Fed’s next policy move but did acknowledge that “we’ve seen that prices are too high.”

While his comments didn’t provide any clear signals about the upcoming meeting, they were enough to keep traders attentive.

By the closing bell, the market’s early optimism had largely faded, with the major indexes finishing modestly in the red.

Bond yields and the U.S. dollar both edged higher, but not enough to derail precious metals. Gold and silver rallied during the session, although both gave back part of their intraday gains before the close.

Meanwhile, Bitcoin enjoyed one of its strongest days in weeks, climbing back above $60 after bouncing off a key 2025 support level. The move is encouraging for crypto bulls, but the next test will be whether the token can break through its recent resistance zone.

{kind=link}

Overall, it was a relatively quiet session, even as the ongoing liquidation of the Japanese yen pushed the currency to fresh 40-year lows—an extraordinary development that continues to unfold largely beneath the market’s radar.

Tomorrow will be a shortened session on Wall Street. I won’t publish a market commentary, but I will post the Thursday StatSheet at the usual time of 6:30 p.m.

Have a wonderful Fourth of July weekend! And as we head into the holiday break, the big question is: Will investors return next week ready to push stocks to new highs, or is a summer pause finally in store?

2. Current domestic “Buy” Cycle (effective 5/20/2025); International “Buy” Cycle (effective 5/8/25)

Our domestic bullish cycle that began on November 21, 2023, concluded on April 3, 2025, following a market downturn triggered by President Trump’s tariff policy announcement.

This development caused significant declines across major indexes and broader market indices. However, markets subsequently rebounded, culminating in a new domestic “Buy” signal taking effect May 20, 2025.

Concurrently, our International Trend Tracking Index (TTI) experienced parallel volatility. On April 4, 2025, it breached critical thresholds, prompting a “Sell” recommendation. This position reversed as global markets recovered, with the International TTI regaining sufficient momentum to issue a new “Buy” signal effective May 8, 2025.

3. Trend Tracking Indexes (TTIs)

It was a pretty quiet day in the markets. The major indexes gave up their early gains, gold followed a similar pattern, and bond yields were essentially flat.

Meanwhile, our TTIs moved in opposite directions, with the domestic TTI finishing higher and the international TTI slipping slightly.

This is how we closed 07/01/2026:

Domestic TTI: +8.95% above its M/A (prior close +8.62%)—Buy signal effective 5/20/25.

International TTI: +6.28% above its M/A (prior close +6.99%)—Buy signal effective 5/8/25.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

———————————————————-

WOULD YOU LIKE TO HAVE YOUR INVESTMENTS PROFESSIONALLY MANAGED?

Do you have the time to follow our investment plans yourself? If you are a busy professional who would like to have his portfolio managed using our methodology, please contact me directly to get more details.

Contact Ulli