- Moving the market

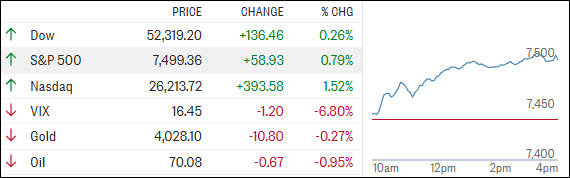

Stocks moved higher today, led by a strong rally in chipmakers, as Wall Street closed out a solid first half of the year and an impressive second quarter.

It’s been anything but a smooth ride. The major indexes pushed to new all-time highs, but not without plenty of turbulence along the way.

Traders had to navigate sharp swings in energy prices tied to tensions in the Middle East, along with growing questions about just how sustainable the current pace of AI spending really is.

Looking ahead, many traders believe the bull market still has room to run, provided tensions between the U.S. and Iran don’t escalate again. There’s also a growing sense that leadership could broaden beyond the market’s biggest winners, with investors rotating into more reasonably valued sectors and stocks.

June offered a mixed picture beneath the surface. Small Caps and the Dow were the month’s strongest performers, while concerns about the costs and profitability of AI investments weighed modestly on the Nasdaq and S&P 500. Even so, the pullbacks were relatively mild and did little to derail the broader uptrend.

The shift in interest-rate expectations has been one of the year’s biggest surprises. Just a few months ago, markets were pricing in several Fed rate cuts for 2026.

Today, expectations have swung dramatically, with some investors now preparing for the possibility of rate hikes as inflation concerns linger and policymakers maintain a hawkish tone.

{kind=link}

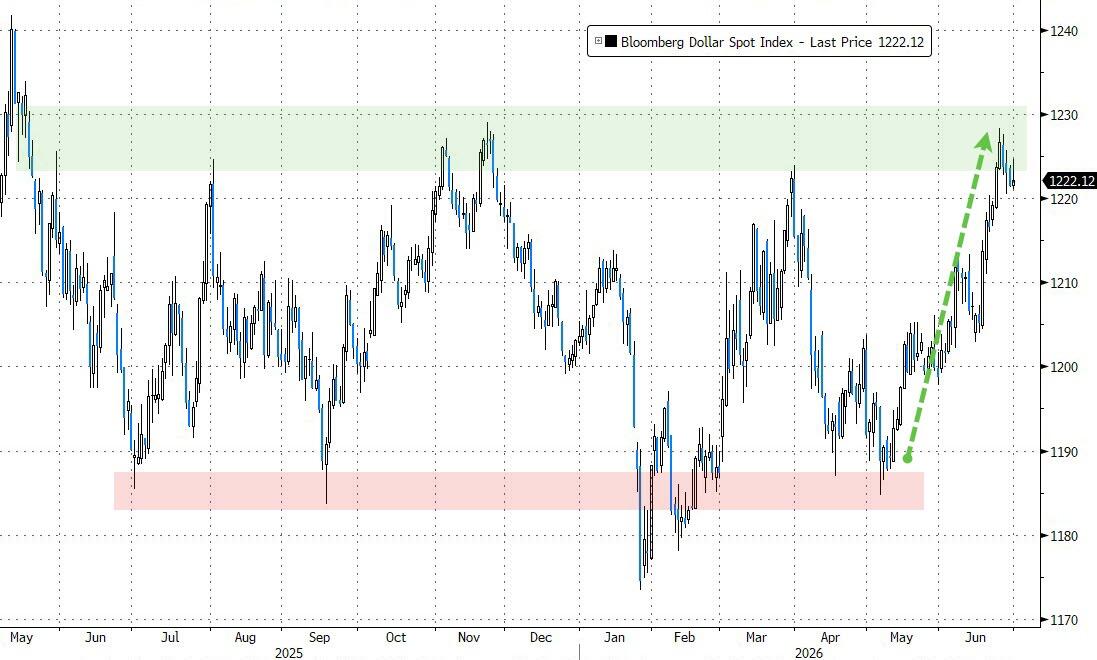

Meanwhile, the U.S. dollar extended its rally for a fourth straight quarter, climbing back toward the upper end of its two-year trading range. A stronger dollar continued to pressure gold, which posted its fourth consecutive monthly decline. Bitcoin also struggled, recording its weakest start to a year since 2022.

{kind=link}

Perhaps the biggest takeaway is that while fears of an energy-driven economic shock have faded as oil prices retreated from above $90 to around $70 per barrel, concerns about higher interest rates remain very much alive. In short, the energy shock may be behind us, but the rate shock is still front and center.

As we head into the second half of the year, will broader market participation keep the bull market going, or will higher rates eventually start to weigh on investor enthusiasm?

2. Current domestic “Buy” Cycle (effective 5/20/2025); International “Buy” Cycle (effective 5/8/25)

Our domestic bullish cycle that began on November 21, 2023, concluded on April 3, 2025, following a market downturn triggered by President Trump’s tariff policy announcement.

This development caused significant declines across major indexes and broader market indices. However, markets subsequently rebounded, culminating in a new domestic “Buy” signal taking effect May 20, 2025.

Concurrently, our International Trend Tracking Index (TTI) experienced parallel volatility. On April 4, 2025, it breached critical thresholds, prompting a “Sell” recommendation. This position reversed as global markets recovered, with the International TTI regaining sufficient momentum to issue a new “Buy” signal effective May 8, 2025.

3. Trend Tracking Indexes (TTIs)

The bulls stayed firmly in control today, pushing the major indexes to yet another positive close. The S&P 500 and Nasdaq wrapped up a strong quarter, although both finished June slightly in the red.

Metals turned in a mixed performance, with gold mostly holding steady while silver and copper posted solid gains.

Our TTIs headed in opposite directions, as the domestic indicator slipped modestly while the international indicator managed to squeeze out a small gain.

This is how we closed 06/30/2026:

Domestic TTI: +8.62% above its M/A (prior close +8.77%)—Buy signal effective 5/20/25.

International TTI: +6.99% above its M/A (prior close +6.76%)—Buy signal effective 5/8/25.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

———————————————————-

WOULD YOU LIKE TO HAVE YOUR INVESTMENTS PROFESSIONALLY MANAGED?

Do you have the time to follow our investment plans yourself? If you are a busy professional who would like to have his portfolio managed using our methodology, please contact me directly to get more details.

Contact Ulli