Below, please find the latest High-Volume ETF Cutline

report, which shows how far above or below their respective long-term trend

lines (39-week SMA) my currently tracked ETFs are positioned.

This report covers the HV ETF Master List from Thursday’s

StatSheet and includes 322 High Volume ETFs, defined as those with an average

daily volume of more than $5 million, of which currently 281 (last week 274)

are hovering in bullish territory. The yellow line separates those ETFs that

are positioned above their trend line (%M/A) from those that have dropped below

it.

In case you are not familiar

with some of the terminology used in the reports, please read the Glossary of Terms.

If you missed the original

post about the Cutline approach, you can read it here.

Markets

Melt Up Due To Better Than Expected Jobs Report

[Chart courtesy of MarketWatch.com]

Moving

the markets

The jobs report proved to be the dominating

market force today, as October lost its luster as a bull market killer. The US

economy added 128k jobs, which was far better than the expected 85k. Another bullish

surprise were the upside revisions in employment gains in August and September,

which combined were 95,000 more than previously reported.

Manufacturing suffered due to the strike at

GM causing a decline of almost 42k automaker jobs but, now that the strike is over,

a rebound of similar magnitude is expected next month.

The oddity that stocks continue to rally as bond

yields rise, despite the Fed’s easing policy, seems contrary to conventional wisdom—and

it is. This scenario has, short-term, not worked out well for the low volatility

ETF SPLV, which has not participated in the current rally, as it did for the first

9 months of this year.

As a result, the S&P 500 (SPY +11.34%) is

closing in on SPLV’s performance (+13.23%), but it has not caught up yet, however,

given current circumstances, I will make some adjustments to our holdings.

Not all of today’s melt-up was due to the

jobs report, as variety of officials were called up to keep the mood bullish.

ZH summed up the events in this timeline:

0830ET Jobs Beat – Dow +100

0915ET Fed’s Kashkari dovish: “we’re not

at maximum employment.. in free lunch zone” – Dow +20

0920ET Mnuchin: “constructive talks,

working hard” – Dow +30

0930ET Fed’s Rosengren hawkish: further

monetary accommodation not needed – Dow unch

0935ET Fed’s Clarida neutral: “we will

be data-dependent, economy/consumer in good place” – Dow unch

0936ET Fed’s Kaplan dovish: “growth in

US is decelerating, need skills-based immigration”

0937ET Kudlow: White House wants tax cuts for

middle class, Trump optimistic on trade deal – Dow unch

0945ET Kudlow: “enormous progress on IP

theft” – Dow +30.

0950ET Record high for S&P and Nasdaq

0955ET Kudlow: “US-China trade call may

be happening now, Ag & FX parts virtually completed” – Dow +20

1000ET ISM Manufacturing MISS, 3rd month of

contraction (bad news is good news) – Dow +50

1050ET Mission Accomplished – Dow futs take

out post-Powell high stops

1215ET Dow futs stops run and fade begins

into EU close

1325ET Fed’s Daly neutral/hawkish:

“annual wage growth of about 3% is good news” – Dow unch

1450ET Fed’s Williams neutral/hawkish:

“economy is in a very good place, it is strong” – Dow -10

1600ET RECORD CLOSE FOR S&P AND NASDAQ

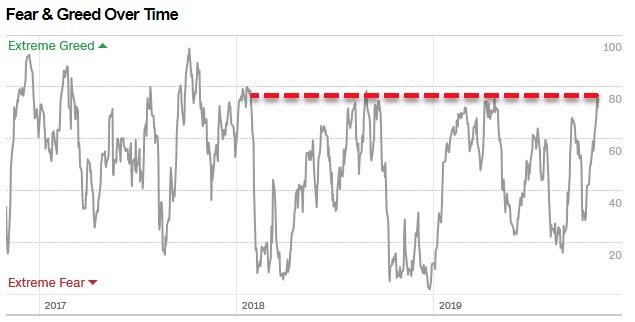

Of course, the Fear

& Greed index paints a different picture and has risen to a height last

seen in January of 2018. Every time this indicator has reached current levels,

it abruptly changed direction. Will it be different this time?

ETF Data

updated through Thursday, October 31, 2019

Methodology/Use of this StatSheet:

1. From the universe of over 1,800 ETFs, I have selected only those with a

trading volume of over $5 million per day (HV ETFs), so that liquidity and a

small bid/ask spread are assured.

2. Trend Tracking Indexes (TTIs)

Buy or Sell decisions for Domestic and International ETFs (section 1 and

2), are made based on the respective TTI and its position either above or below

its long-term M/A (Moving Average). A crossing of the trend line from below

accompanied by some staying power above constitutes a “Buy” signal. Conversely,

a clear break below the line constitutes a “Sell” signal. Additionally, I use a

7.5% trailing stop loss on all positions in these categories to control

downside risk.

3. All other investment arenas do not have a TTI and should be traded

based on the position of the individual

ETF relative to its own respective trend line (%M/A). That’s why those signals

are referred to as a “Selective Buy.” In other words, if an ETF crosses its own

trendline to the upside, a “Buy” signal is generated. Since these areas tend to

be more volatile, I recommend a wider trailing sell stop of 7.5% -10% depending

on your risk tolerance.

If you are unfamiliar with some of the terminology, please see Glossary of Termsand new subscriber information in section 9.

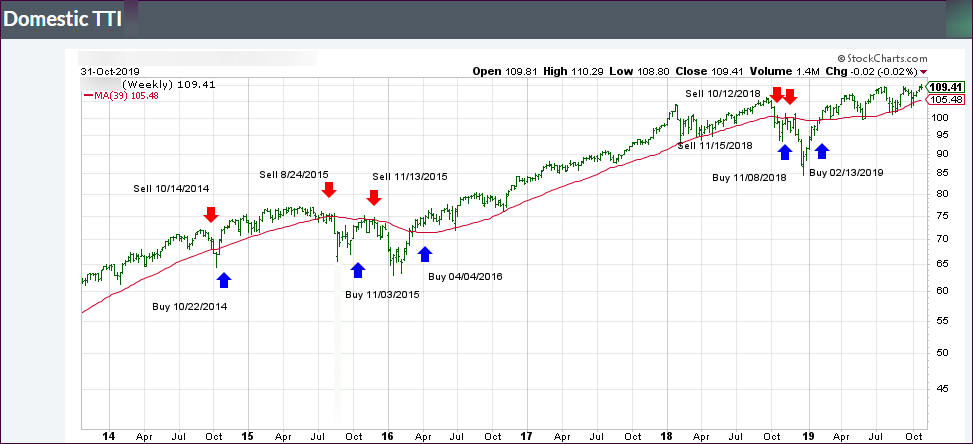

1. DOMESTIC EQUITY ETFs: BUY

— since 02/13/2019

Click on chart to enlarge

Our main directional indicator, the Domestic Trend Tracking Index (TTI-green line in the above chart) is now positioned above its long-term trend line (red) by +3.98% after having generated a new Domestic “Buy” signal effective 2/13/19 as posted.

Despite the Fed’s market

pleasing efforts yesterday, it appears that the US-China trade talks, or rather

the lack thereof, have enough power left to affect market direction. Such was

the case this morning when a report said that “Chinese officials have doubts

about the prospects for a long-term trade deal with the US.”

Attempting to dampen the subsequent

fall of equities, Trump came out and announced that a “transitional deal”

would be still signed soon, although the warring parties need to pick a new

site for this event, as the previous host, Chile, canceled the mid-November

summit.

Just the fact that the Dow

was down a “shocking” 240 points this morning caused all kinds of action by the

administration, as economic advisor Kudlow came out and attempted to jawbone

the markets higher with goodies like “US-China talks going smoothly.” It

did have a momentary positive effect, as this

chart shows.

Then the blame game

continued with Trump seething that “China’s not our problem, The Fed is.”

You almost have to laugh at the silly notion that it seems no longer acceptable

to have a minor correction, let alone a normal downturn as part of the business

cycle. But that’s the world we live in, and we must deal with it.

In the end, the month of

October, also known as the bull market killer, turned out better than expected,

although it started out on a negative note with a 2-day sell-off. That was

short-lived, and we seesawed higher with the S&P 500 closing the month with

a respectable +1.9% gain.

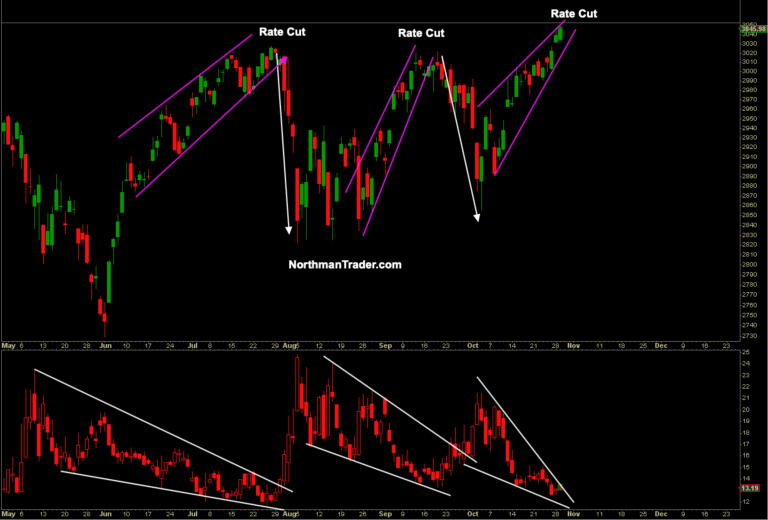

It’s low volatility cousin,

SPLV, did not fare as well and got blindsided by bond yields, which rose

despite the Fed’s easing efforts. Just like in September, this

chart shows the rebound in the 10-year yield (blue arrows), which affected

SPLV negatively due to its interest rate component. Even though, SPLV gave back

-0.58% this month, it remains ahead of the S&P 500 in YTD ‘Buy’ cycle

performance.

As was expected, the Fed cut

interest rates by 0.25%, and analysts were salivating all over the language in

the accompanying statement, in order to see what might have been said different

this time.

The wording shifted slightly

to a more hawkish stance from:

“…will continue to

monitor the implications of incoming information for the economic outlook and will

act as appropriate to sustain the expansion, with a strong labor market and

inflation near its symmetric 2 percent objective.”

To:

“The Committee will

continue to monitor the implications of incoming information for the economic

outlook as it assesses the appropriate path of the target range for the

federal funds rate.”

Then Fed chair Powell

suggested that “I think we would need to see a really significant move

up in inflation that’s persistent before we even consider raising rates to

address inflation concerns.” That was the icing on the cake that got the computer

algos started, and the major indexes spiked and closed in the green.

To no surprise, interest

rates dropped today with the 10-year bond yield sliding over 6 basis points, which

gave a nice assist to the low volatility ETF SPLV, which added +0.73% vs. the

more modest performance of the S&P 500 (SPY), which rose +0.33%.

The question now is “can equities

trek higher without the Fed’s assistance?” It appears right now that there

will be no cut in December (76% odds), so that hope factor is off the table for

the time being.

Despite Trump tweeting that

we have “The Greatest Economy in American History,” the factual GDP numbers

paint a slightly different picture. The US economy, according to ZH, grew at

a 1.9% annualized rate, well above the 1.6% expected, but still below the

already weak Q2 print of 2.0%, and matching the second weakest reading of the

Trump administration.

Yet, the S&P 500 hovers

in record territory, which makes it abundantly clear, contrary to common view,

that the stock market and the economy are totally disconnected from each other.

After an early bounce, the markets

pulled back with the Nasdaq suffering the most after Google’s disappointing earnings,

which followed a few days later after Amazon showed a quarterly report card

that was not up to expectations. I was surprised to see this little of a

fallout from these 2 behemoths, which usually impact market direction more

severely.

It seems traders were more

focused on the overall earnings picture, which continued its trend of better-than-feared

results. Individual misses, even by large companies, were simply accepted as an

outlier.

The US-China trade debacle

was on the radar as well, but after yesterday’s positive noises, the “phase one”

deal may not be ready for signing by the time Trump and Xi Jinping meet in Chile

next month, according to a Reuters report. That does not surprise me, after

all, the dangling trade carrot is merely being used to move markets in the desired

direction and not to signal any agreement with substance.

The mixed picture on the economic

front featured two events with opposite outcomes. First, we learned that Pending

Home Sales surprised to the upside by scoring its biggest annual gain since 2015.

This positive event, however, was upset by the fact that Consumer Confidence

tumbled to a 7-month low to its lowest since March.

In the end, the major indexes

meandered around their respective unchanged lines, as awareness struck traders

that not only does tomorrow’s Fed announcement still carry an element of uncertainty,

but also reminded them of what happened the

last two times rates were lowered.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}