ETF Tracker StatSheet

You can view the latest version here.

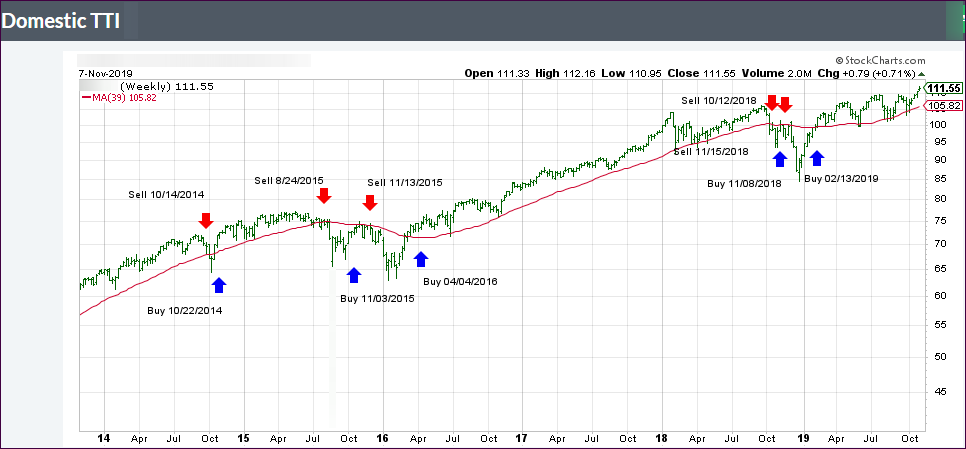

SEARCHING FOR CLARITY

- Moving the markets

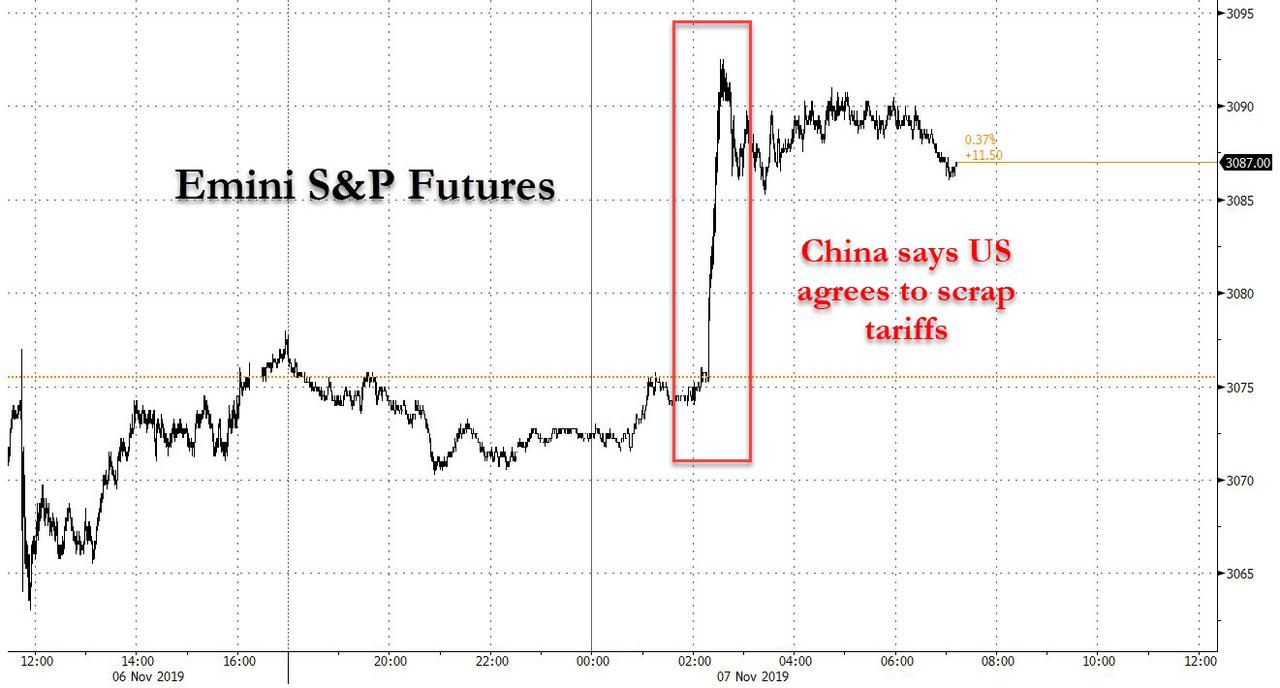

The futures market took the early lead by heading south after Trump’s confirmation that he has not agreed to roll back tariffs with China, which was opposite of what economic advisor Larry Kudlow had stated.

The early dump was quickly reversed, however, as the major indexes scrambled back towards their respective unchanged lines. They hung around for the remainder of the session with only a small gain to show for the day but closing higher for the week.

As I posted yesterday, the driver for the past 5 days or so has been the continued pumping of alleged positive trade news, even if they were “revised” later, as was the case today.

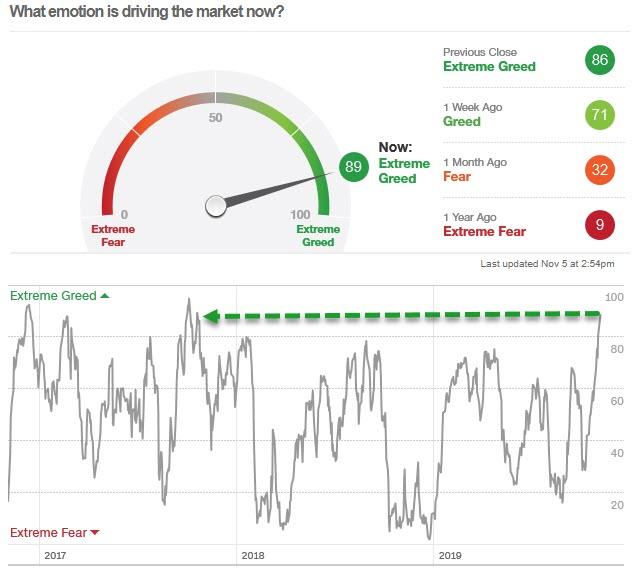

It is a sure sign of bullishness in the marketplace when doubts about previous trade agreements don’t affect effect equities negatively. In other words, fresh clouds over trade talks are not eliminating the cheery outlook traders seem to have.

Even the computer algos, designed to react instantly to questionable announcements, seem not to be impacted, maybe due to the planned “phase one” pact still being on schedule.

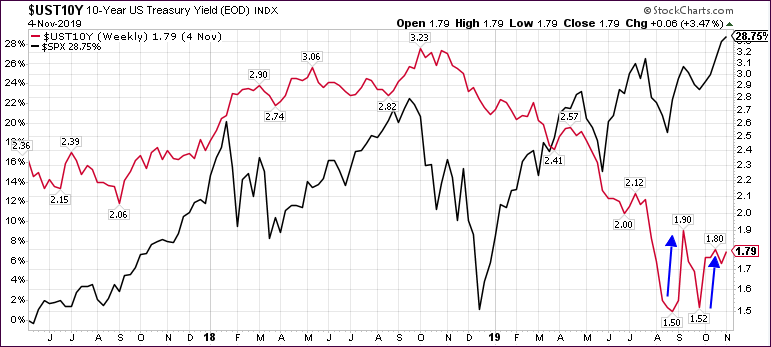

While all seems rosy in equity land, the bond market echoes a different view. Yields on the 10-year catapulted recently and reached a high last seen in August. If rising yields morph into a bond market meltdown, the current stock rally could fade in a hurry.

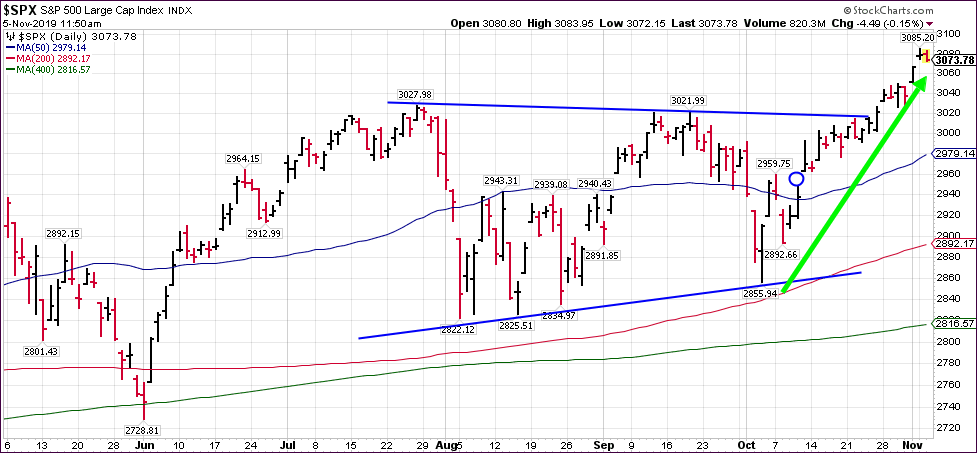

However, for right now the trend is up, and we’ll enjoy the ride, because we know that “liquidity” is our friend and continues to be the primary driver for equities.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}