- Moving the market

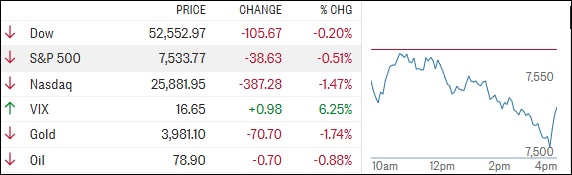

Stocks struggled to gain traction today, with the S&P 500 and Nasdaq coming under pressure early as a sell-off in chip stocks overshadowed an otherwise encouraging batch of earnings reports.

In fact, earnings season is off to a strong start. Of the 40 S&P 500 companies that have reported so far, more than 87% have beaten expectations.

The major banks, often viewed as a barometer of overall economic health, set a positive tone earlier this week by delivering second-quarter results that comfortably topped forecasts.

The economic data painted a mixed but generally resilient picture. The U.S. consumer continues to hold up despite ongoing pricing pressures.

Weekly jobless claims came in at 208,000, better than the 218,000 economists were expecting, while retail sales matched forecasts with a 0.2% increase.

On the flip side, housing data, consumer sentiment, and pending home sales all came in softer than expected.

Elsewhere, markets kept a close eye on geopolitics and commodities. Oil initially surged following reports of intensified U.S. strikes against Iran overnight, only to give back those gains later in the session.

{kind=link}

Despite the drama, crude has essentially gone nowhere over the past three days. The dollar bounced higher, gold fell below the $4,000 level, and bitcoin drifted lower before finding support near $64,000.

{kind=link}

{kind=link}

{kind=link}

Meanwhile, the AI trade appears to be hitting a rough patch. Traders are beginning to question where the next leg of growth will come from as returns remain elusive, financing costs rise, local communities push back against data-center expansion, and power and water availability become increasingly important constraints.

Taken together, these crosscurrents could keep markets stuck in a sideways trading range until we get greater clarity on earnings, economic growth, and the future of the AI investment boom.

The question now is: will strong earnings be enough to reignite the market’s momentum, or is a longer period of consolidation ahead?

2. Current domestic “Buy” Cycle (effective 5/20/2025); International “Buy” Cycle (effective 5/8/25)

Our domestic bullish cycle that began on November 21, 2023, concluded on April 3, 2025, following a market downturn triggered by President Trump’s tariff policy announcement.

This development caused significant declines across major indexes and broader market indices. However, markets subsequently rebounded, culminating in a new domestic “Buy” signal taking effect May 20, 2025.

Concurrently, our International Trend Tracking Index (TTI) experienced parallel volatility. On April 4, 2025, it breached critical thresholds, prompting a “Sell” recommendation. This position reversed as global markets recovered, with the International TTI regaining sufficient momentum to issue a new “Buy” signal effective May 8, 2025.

3. Trend Tracking Indexes (TTIs)

Only the Dow managed to open in positive territory, but it couldn’t escape the broader market weakness.

A sell-off in chip stocks weighed heavily on the S&P 500 and Nasdaq, ultimately pulling all three major indexes into the red by the closing bell.

Metals and bitcoin also came under pressure, though our TTIs held up remarkably well. The international TTI finished essentially flat on the day, while the domestic TTI posted a solid gain of about 1%.

This is how we closed 07/16/2026:

Domestic TTI: +8.99% above its M/A (prior close +7.91%)—Buy signal effective 5/20/25.

International TTI: +6.69% above its M/A (prior close +6.76%)—Buy signal effective 5/8/25.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

———————————————————-

WOULD YOU LIKE TO HAVE YOUR INVESTMENTS PROFESSIONALLY MANAGED?

Do you have the time to follow our investment plans yourself? If you are a busy professional who would like to have his portfolio managed using our methodology, please contact me directly to get more details.

Contact Ulli