- Moving the markets

President Trump set the tone early on for today’s rally by suggesting that “today will be a good day in the stock market,” and just in case the computer algos missed his prediction, he created more excitement via his remark that “the China deal is moving forward ahead of schedule.”

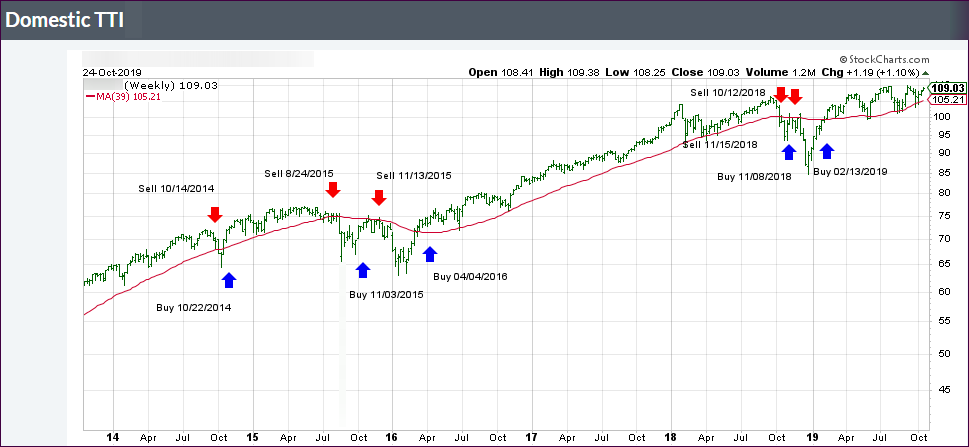

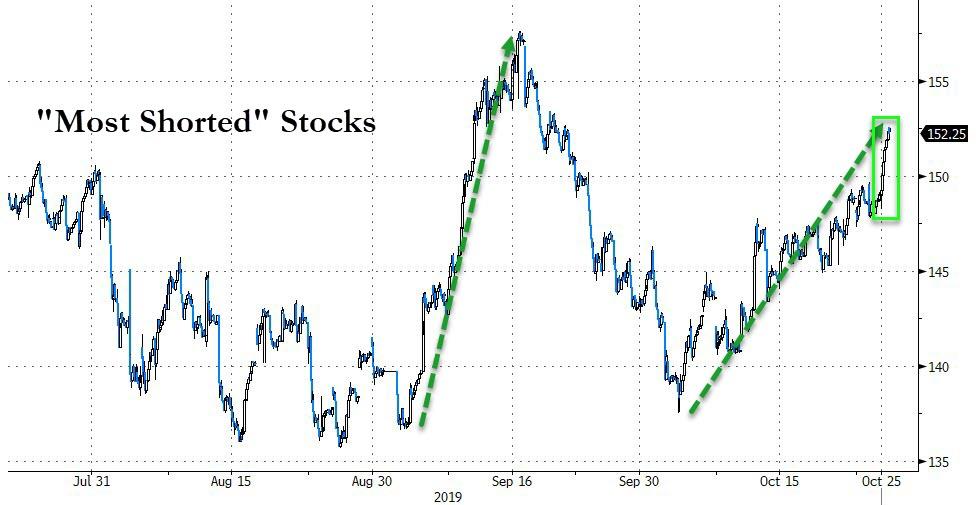

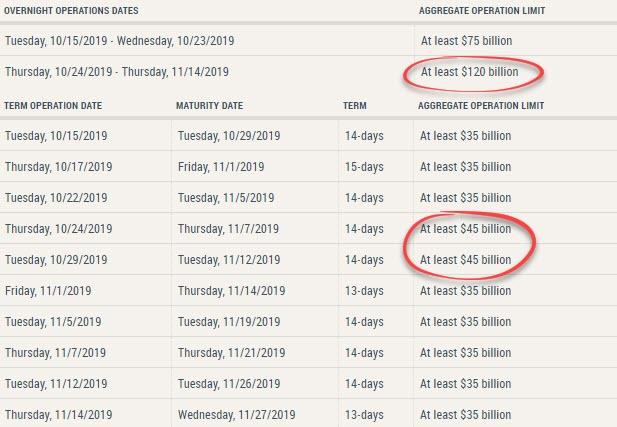

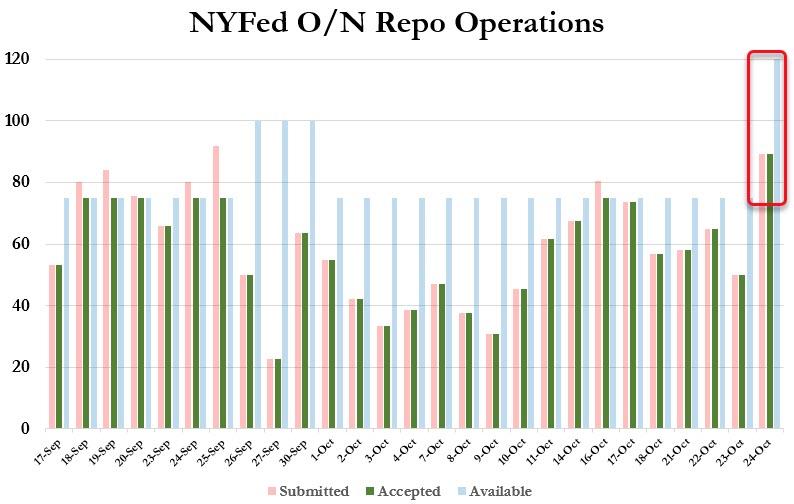

Of course, we know by now that things like global liquidity and short squeezes rule supreme when it comes to pushing markets higher, as this chart shows.

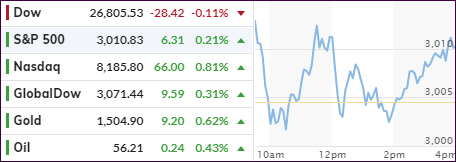

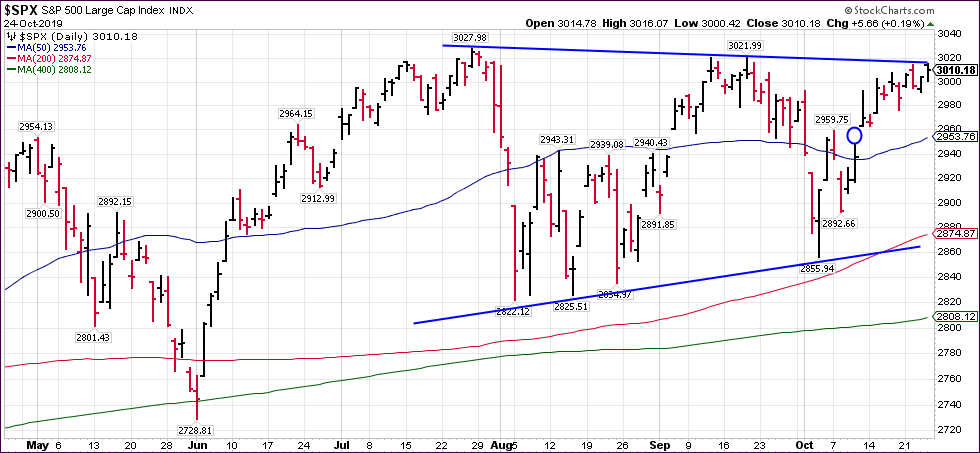

All the above turned out to be enough to extend the S&P’s move into record territory, while the Dow and Nasdaq were just hovering below their respective record closes set in late July. Of course, traders’ focus remained on the still outstanding earnings reports, of which 162 S&P 500 companies will release their report cards this week.

Earnings from one of the bigger names, like AT&T, were market pleasing with the media giant topping third quarter expectations, while announcing a plan to grow earnings per share by at least 33% by 2020.

Other news, which did not affect markets were the Fed’s meeting on interest rates with the verdict due out Wednesday. A quarter point reduction is expected, and the Fed will have to deliver or the markets sure will have a tizzy fit.

It’s noteworthy, that today was the third day in a row during which bond yields jumped (today by about 5 basis points), and the markets rallied anyway. Usually, rising bond yields tend to pull down equities, but we appear to be stuck in a moment in time, where the opposite is occurring.

That has been a negative, as I posted on Friday, for the low volatility ETF (SPLV), which gave back -0.49% for the day, while the S&P 500 (SPY) managed to score a gain of +0.58%.

Yet, YTD for our current ‘Buy’ signal, the SPLV still has notched superior gains (+12.20%) and remains ahead of SPY (+10.31%), but the victory margin has narrowed. When rates head back south again, however, we will see the pendulum swing back the other way.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}