- Moving the market

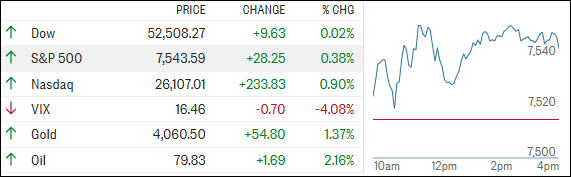

The S&P 500 and Nasdaq got off to a strong start today, led higher by semiconductor stocks after June inflation came in cooler than expected.

The Consumer Price Index (CPI) fell 0.4% for the month, bringing the annual inflation rate down to 3.5%, well below economists’ expectations of 3.8%.

The softer inflation data immediately fueled hopes that the Federal Reserve may not need to be as aggressive with interest rates.

Expectations for a rate hike at the July meeting dropped sharply, while traders continued to price in a better-than-even chance of a move in September.

{kind=link}

While today’s CPI report suggests that the inflation spike tied to the Iran conflict may be easing, investors aren’t ready to declare victory just yet.

Geopolitical tensions remain elevated, and traders continued to keep a close eye on oil prices after U.S. crude briefly climbed above $80 per barrel.

{kind=link}

Fresh concerns emerged after President Trump announced plans to reinstate a blockade on Iranian shipping through the Strait of Hormuz, a key global energy chokepoint.

Not everything was rosy, however. IBM shares plunged 25% after the company warned that second-quarter profits would fall short of expectations due to weak demand in its software and infrastructure businesses. Ouch.

{kind=link}

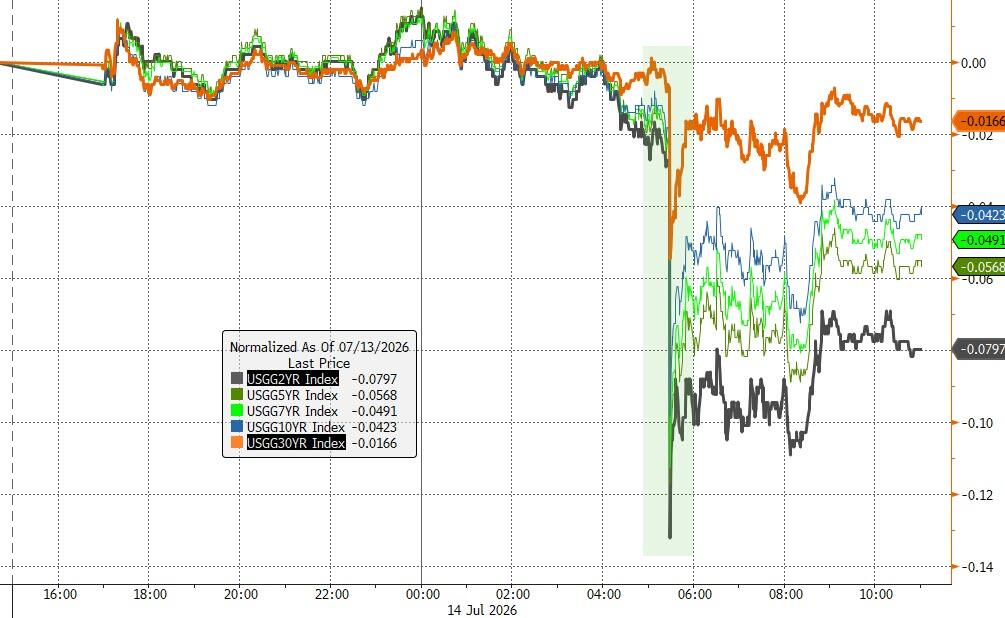

Despite those headwinds, falling bond yields and renewed buying in Mega-Cap and AI-related stocks helped support the broader market.

{kind=link}

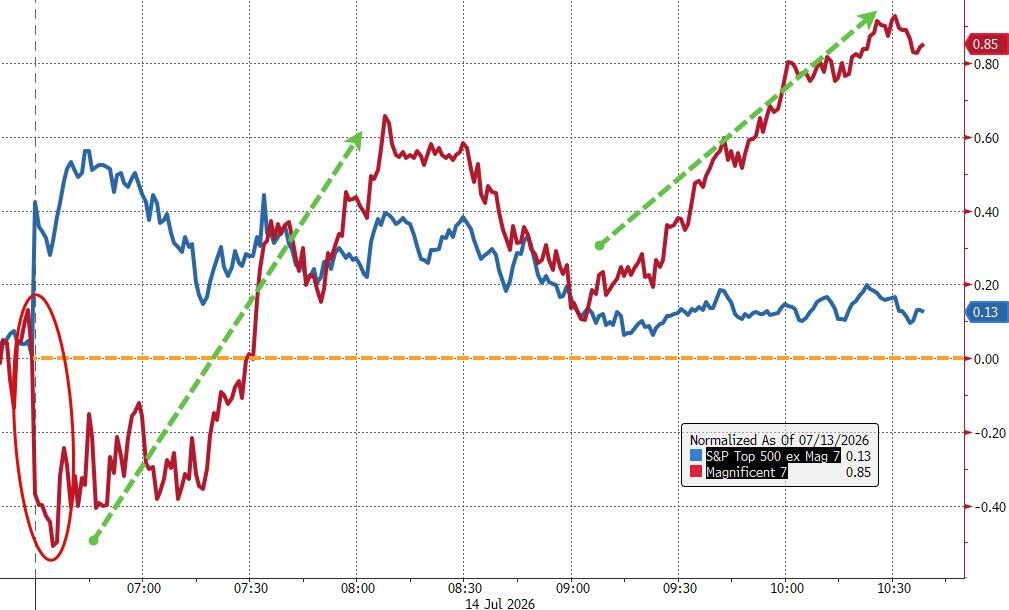

The Mag 7 once again outperformed the other 493 stocks in the S&P 500, overcoming a rough start to the session and leading the major indexes higher.

{kind=link}

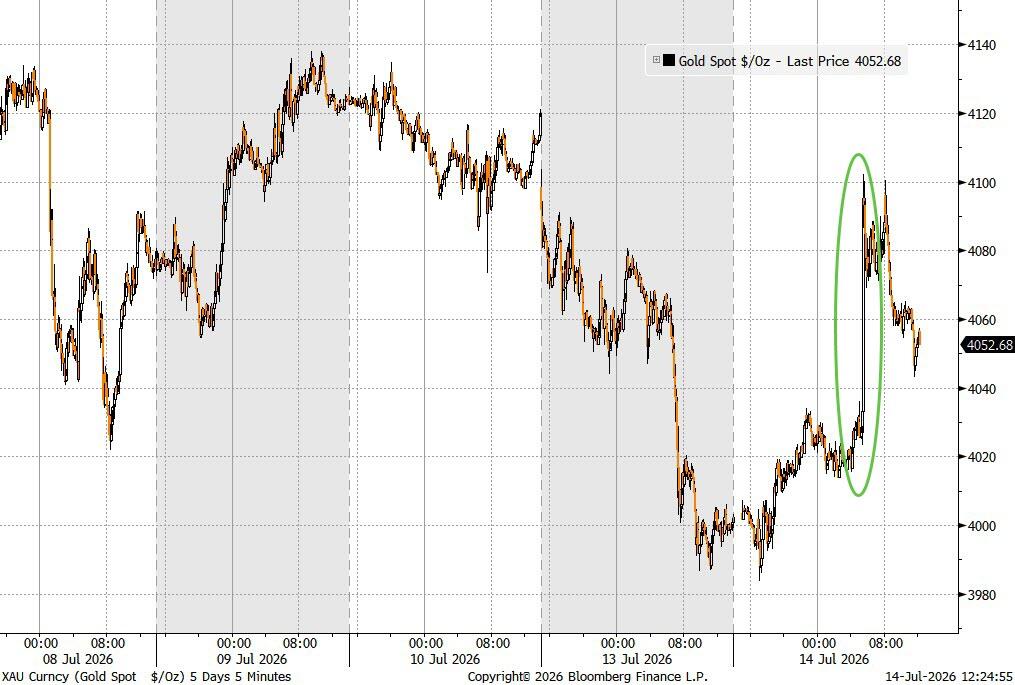

The dollar also weakened, providing a tailwind for alternative assets. Gold surged back above the $4,000 level, while bitcoin rallied from roughly $61,000 toward $65,000, marking its highest level in three weeks.

{kind=link}

{kind=link}

{kind=link}

There were plenty of crosscurrents for traders to navigate today, but the market handled them surprisingly well. The big question now is whether the upcoming earnings season can provide enough fuel to keep this rally moving higher.

2. Current domestic “Buy” Cycle (effective 5/20/2025); International “Buy” Cycle (effective 5/8/25)

Our domestic bullish cycle that began on November 21, 2023, concluded on April 3, 2025, following a market downturn triggered by President Trump’s tariff policy announcement.

This development caused significant declines across major indexes and broader market indices. However, markets subsequently rebounded, culminating in a new domestic “Buy” signal taking effect May 20, 2025.

Concurrently, our International Trend Tracking Index (TTI) experienced parallel volatility. On April 4, 2025, it breached critical thresholds, prompting a “Sell” recommendation. This position reversed as global markets recovered, with the International TTI regaining sufficient momentum to issue a new “Buy” signal effective May 8, 2025.

3. Trend Tracking Indexes (TTIs)

Positive momentum in the S&P 500 and Nasdaq helped the Dow shake off its early weakness and claw its way back to the break-even line.

Technology stocks led the charge, but the bullish sentiment spread well beyond tech, lifting metals and even bitcoin along the way.

Our TTIs finished the day mixed. The international index posted a gain, while the domestic index edged slightly lower.

This is how we closed 07/14/2026:

Domestic TTI: +8.16% above its M/A (prior close +8.55%)—Buy signal effective 5/20/25.

International TTI: +6.43% above its M/A (prior close +6.28%)—Buy signal effective 5/8/25.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

———————————————————-

WOULD YOU LIKE TO HAVE YOUR INVESTMENTS PROFESSIONALLY MANAGED?

Do you have the time to follow our investment plans yourself? If you are a busy professional who would like to have his portfolio managed using our methodology, please contact me directly to get more details.

Contact Ulli