- Moving the markets

The major indexes set new closing records, unimpressed by the ongoing impeachment saga, the result of which has been simply brushed aside.

Market concerns are virtually non-existent, since the Republican-controlled Senate will be the final judge with expectations being that they will vote against having Trump removed from office.

In other words, from a market perspective, the impeachment is meaningless and a non-event.

Positive vibes, that the US-China trade “truce” will hold, continues to lend support to equities with traders considering recent economic data points as temporarily stabilized.

Even today’s Existing Home Sales Report, showing an unexpected tumble in November, could not shatter confidence.

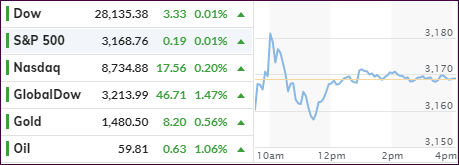

Of course, the ongoing short squeezes gave an assist to the bullish theme, as they have done for the past 4 days straight, even though today we only saw an opening and closing ramp, as Bloomberg’s chart shows.

On deck for tomorrow is options expiration day, which can cause more market fluctuations than normal, but it’s unlikely it will have any effect on the major trend.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}