- Moving the markets

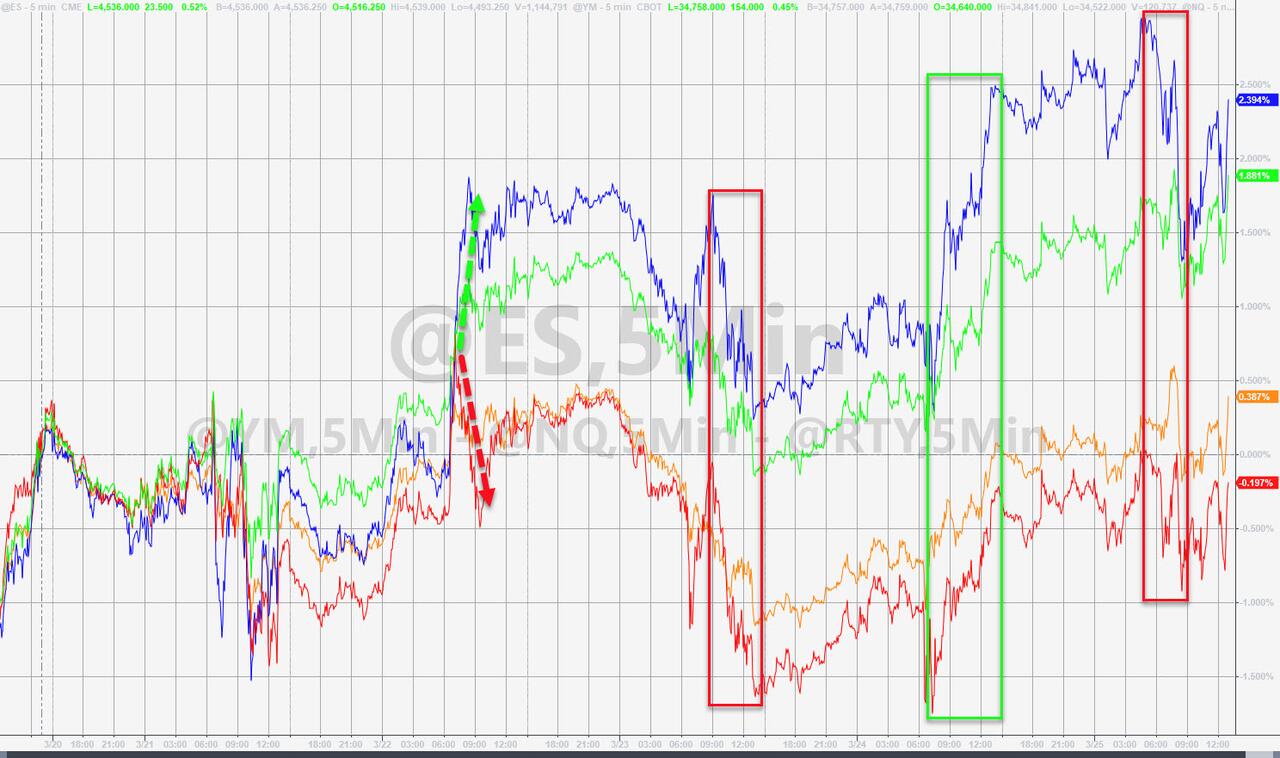

While the Dow peeked above its unchanged line early on, that visit was an ephemeral one because the index shortly thereafter joined the S&P 500 and Nasdaq in the red. The slipping and sliding continued throughout the session with dip buyers being conspicuously absent.

Things got worse mid-day after Russia reported that they were ready for a “final stage” of the Donbas liberation and that other tasks had been completed, as ZH reported:

The markets having soared on optimism yesterday amid chatter of Russian forces retreating, Ukrainian President Zelensky poured some cold water on that hope by noting that Russia is sending new forces during a speech to the Norwegian parliament. He also warned that he sees risk in the Black Sea from Russian mines.

His comments follow a statement from the Kremlin said there are no breakthroughs in talks with Ukraine.

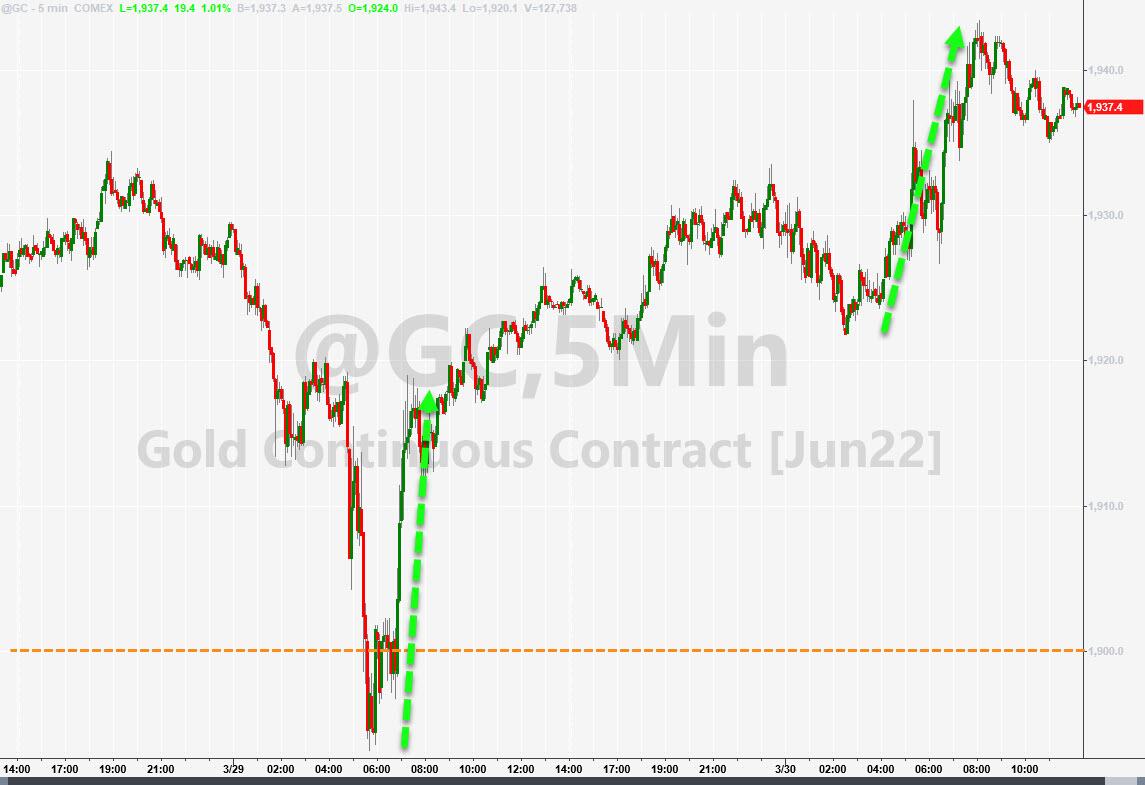

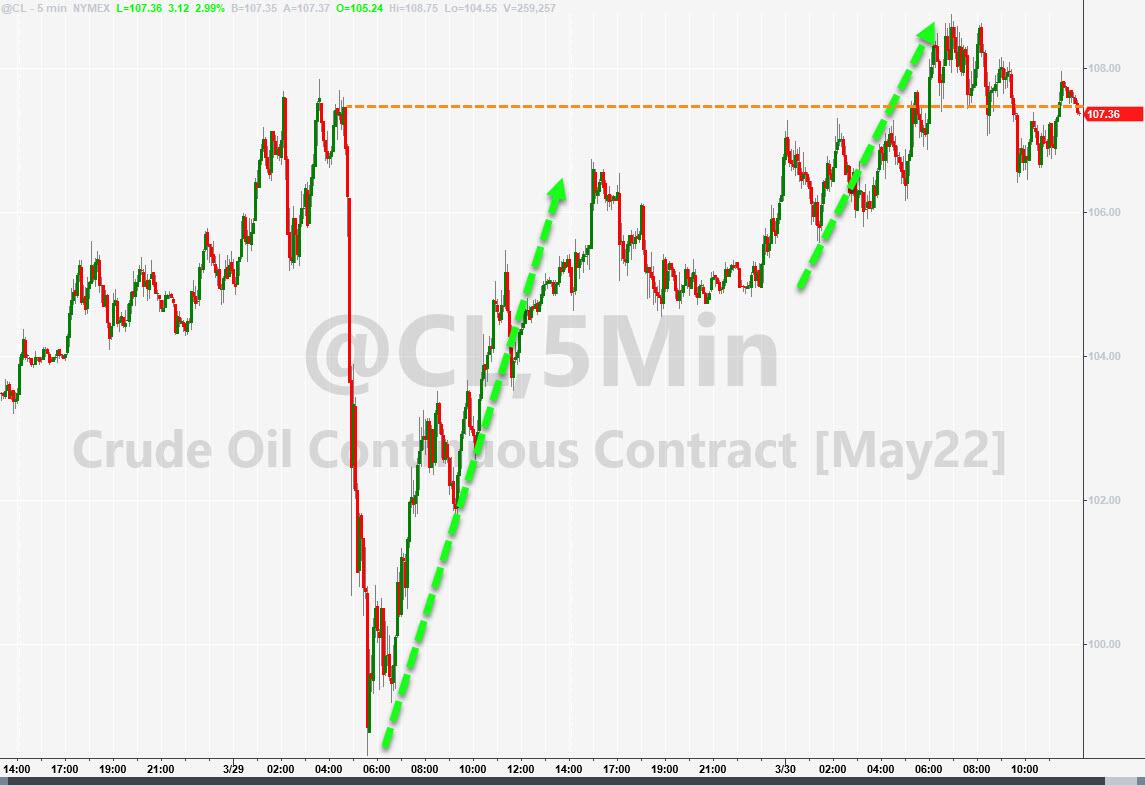

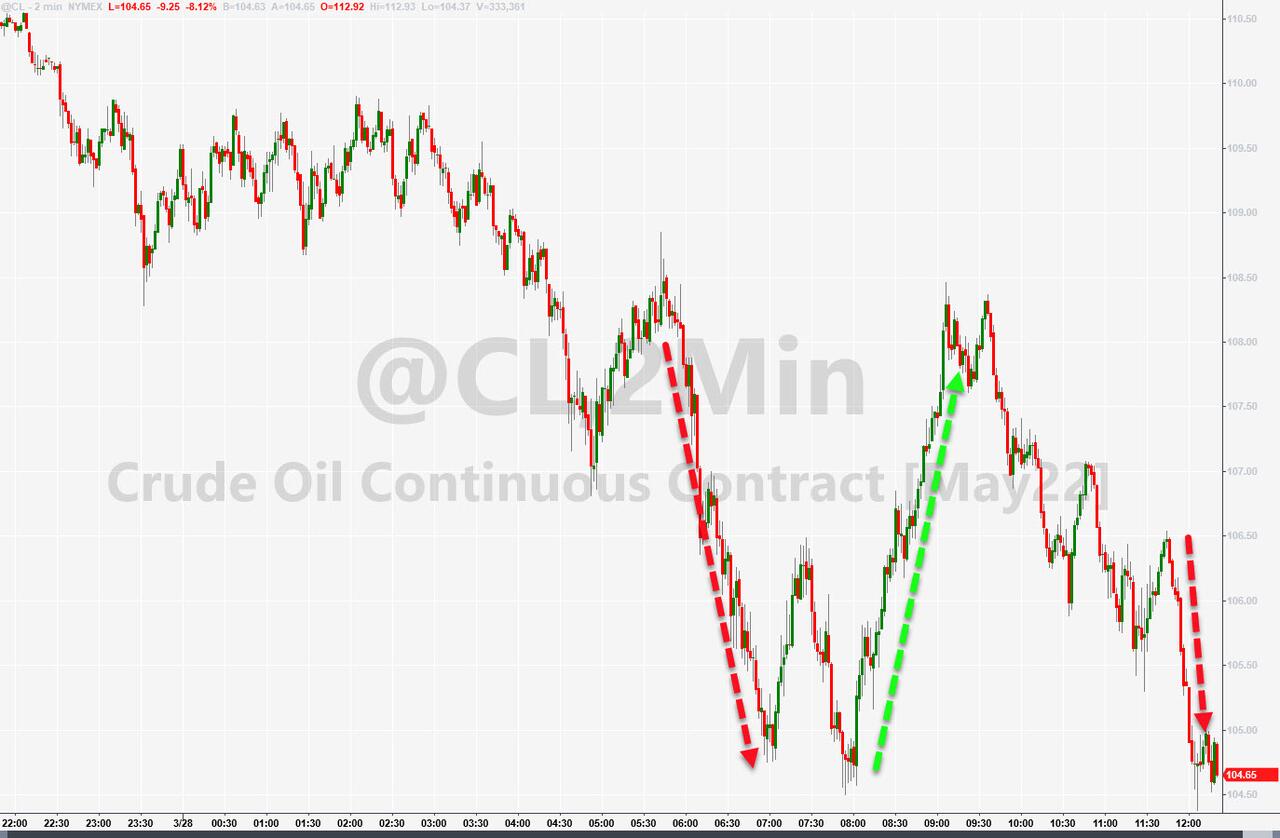

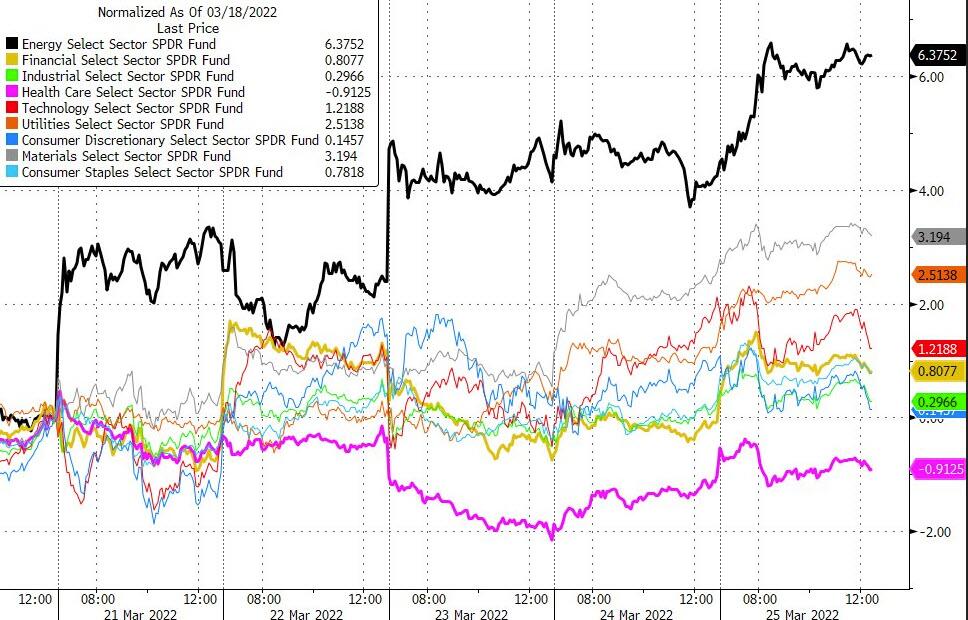

That was good news for Gold, with precious metal jumping and closing the day with a +1.15% gain, while Crude Oil joined the party by advancing +2.84%.

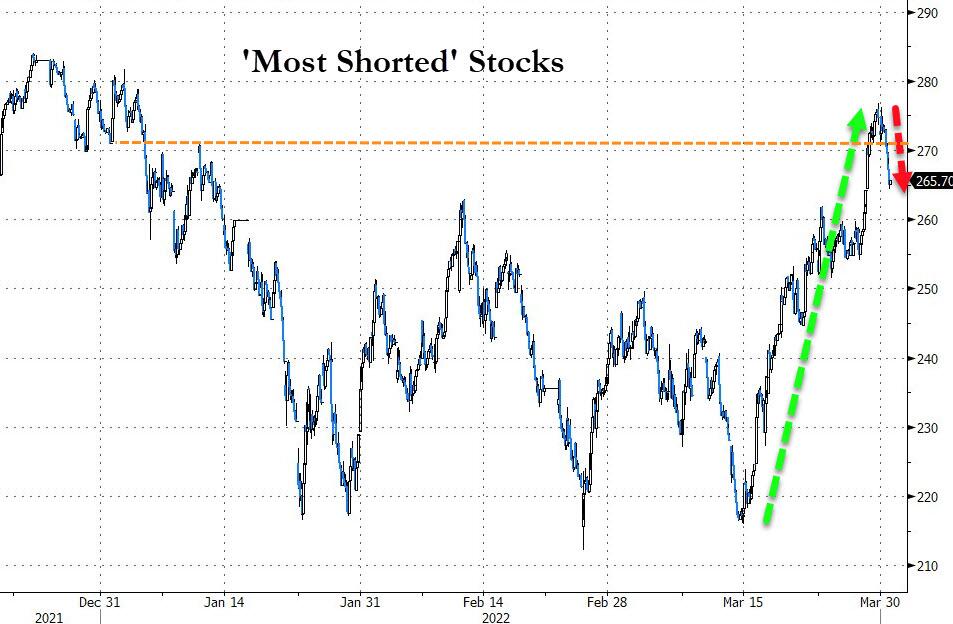

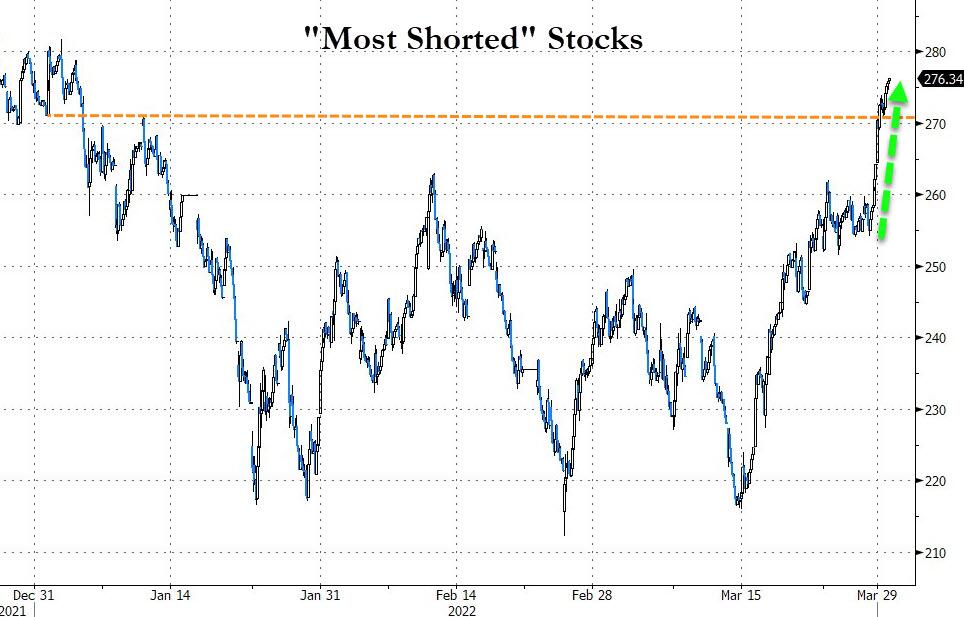

And just like that, yesterday’s peace optimism got put on hold assisted by some hawkish talk by various Fed mouth pieces. Even a decent ADP jobs report could not offset the reality of the moment. A short squeeze attempt hit a brick wall leaving the major indexes to follow the path of least resistance.

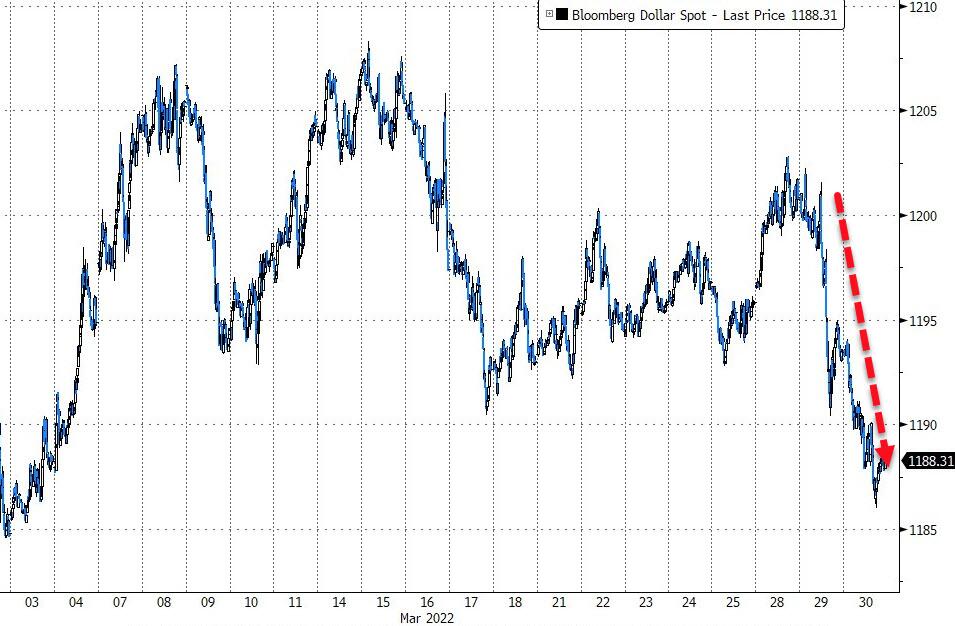

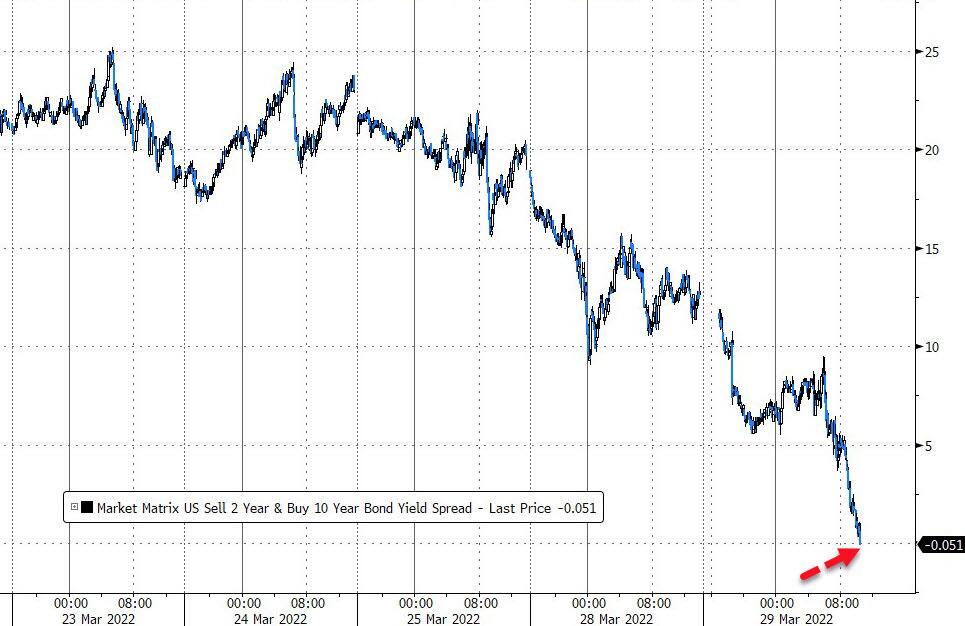

For a change, bond yields backed off their recent highs with the 10-year dropping 5 bps. The US Dollar fell back to almost touch the lows of the month.

In terms of future rate hikes, and subsequent rate cuts, this chart presents the latest update with the markets now expecting 9 more hikes in 2022, creating a recession, which then will be followed by 3 cuts in 2023/24. The latter is what stocks have been focusing on.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}