- Moving the markets

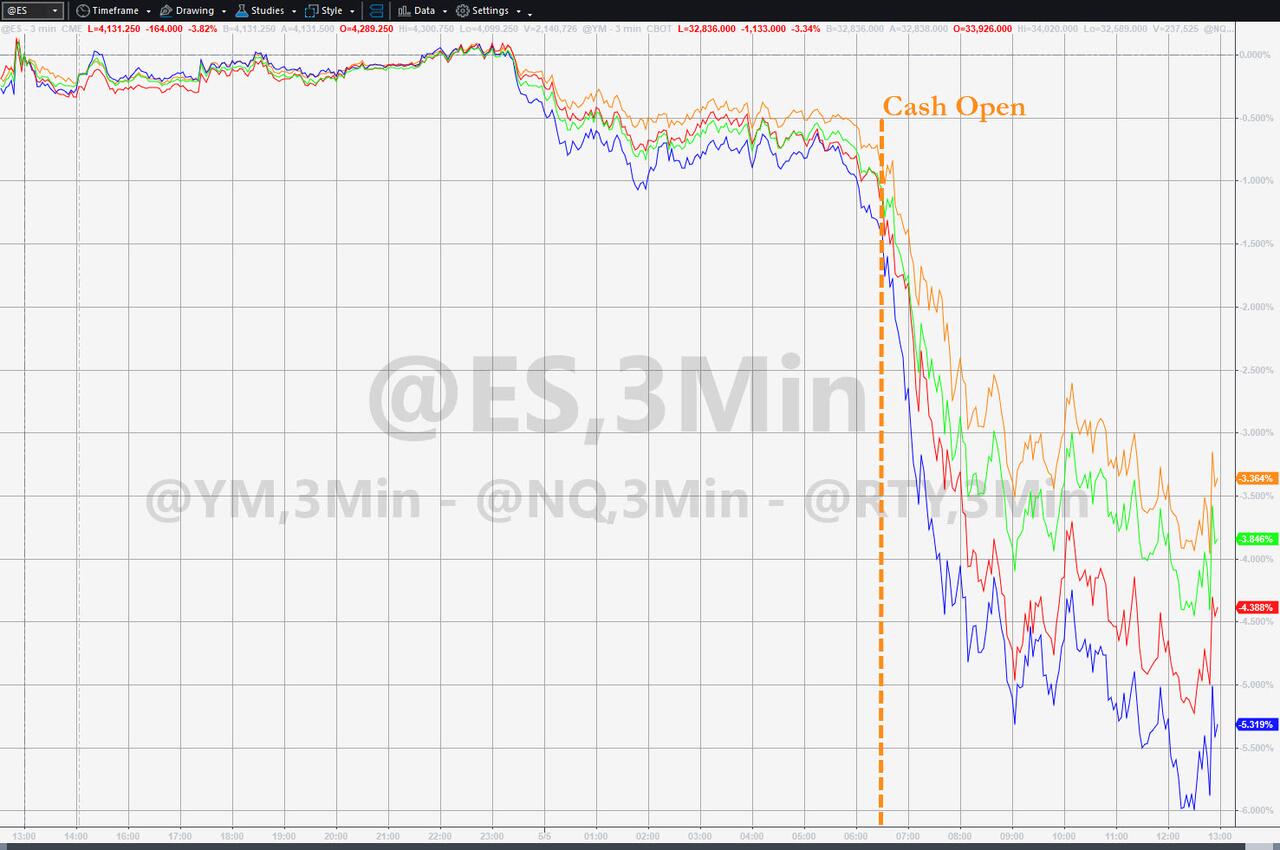

Today’s bloodbath in equities makes yesterday’s “rebound of hope” look like a dead cat bounce, as dip buyers were not to be found anywhere. “Stunning” best describes this sudden reversal, which erased yesterday’s profits and then some.

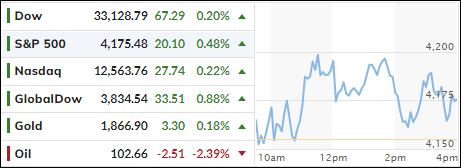

With the Dow tumbling over 1,000 points, domestic equities notched their worst day of the year on top of the already stunning losses YTD. This chart, courtesy of FinViz.com, shows the wild ride we have seen in 2022:

With lower highs and lower lows dominating, and my Domestic TTI now hovering below its long-term trend line by -4.22%, we are clearly stuck in bear market territory and are watching endless rebound attempts.

While there was no place to hide, our selected sector ETFs, took only a small hit, with our latest addition, TBF, being the only one to score a solid gain of +2.81%.

As ZeroHedge noted:

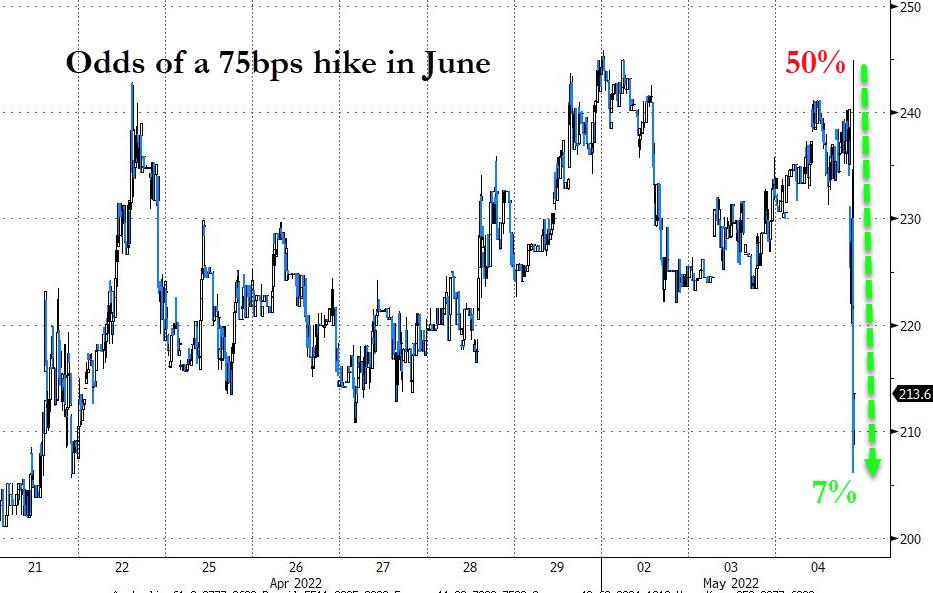

- Remember yesterday was the best performance for a Fed rate-hike day since 1978!

- And today, the Nasdaq 100 Index fell 6% at its lows, the most since March 2020…

- …fully reversing yesterday’s post-FOMC gains

In the past week we have had:

- Friday: biggest drop since June 2020

- Wednesday: biggest surge since May 2020

- Thursday: biggest drop since June 2020

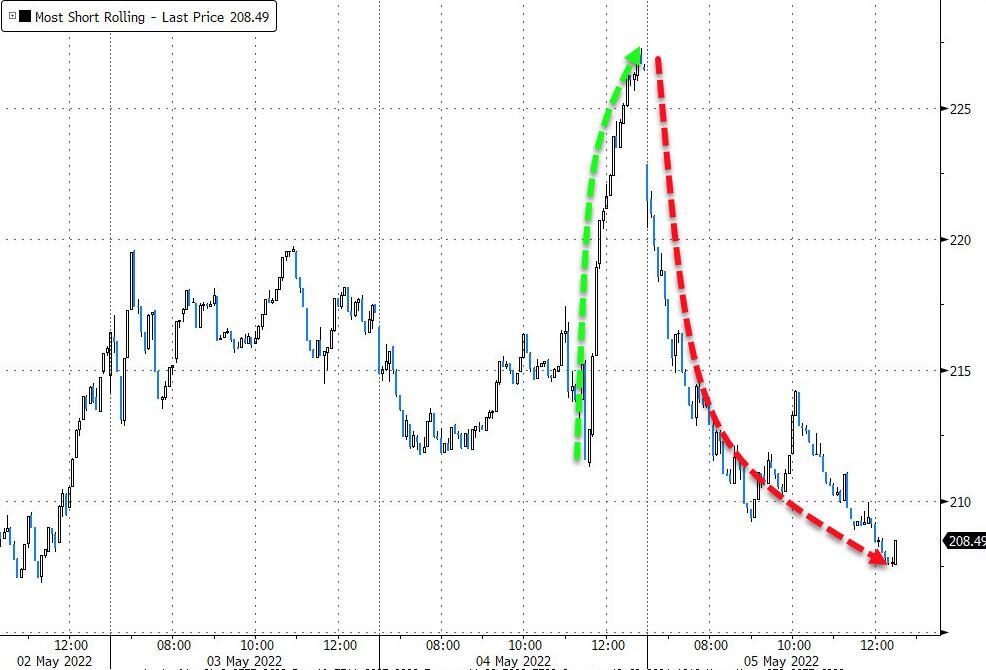

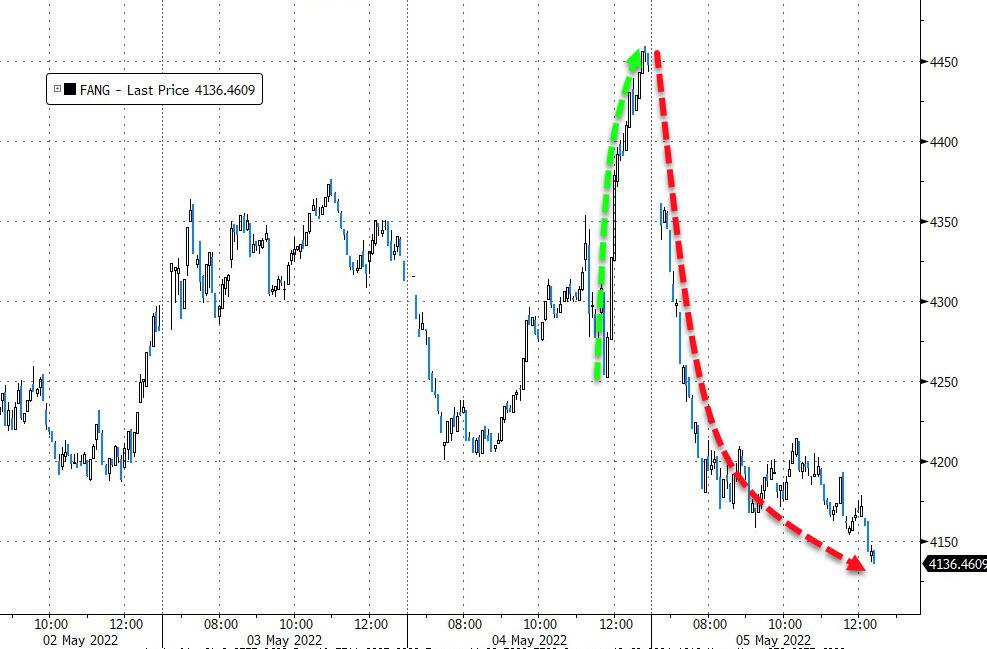

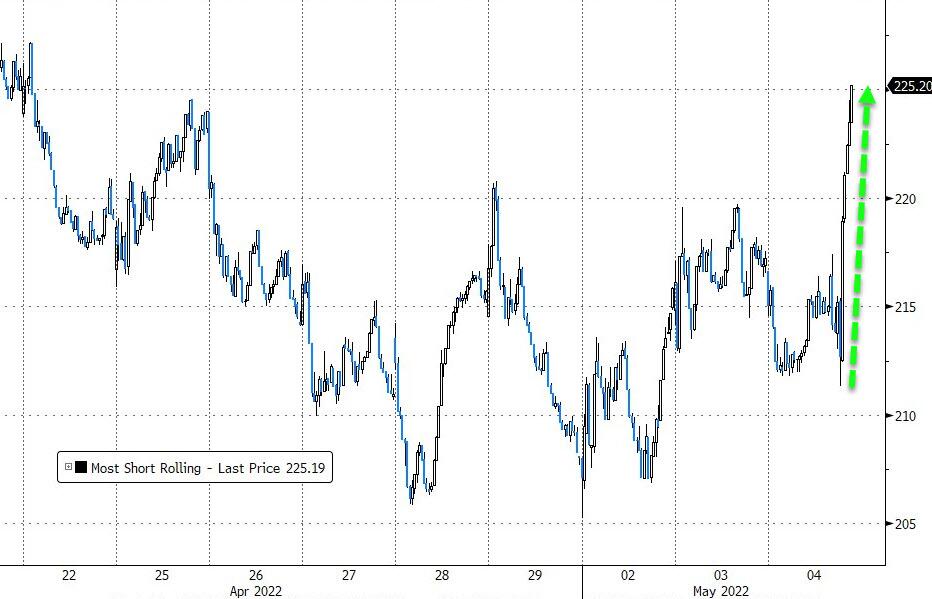

And, not helping matters today was the huge unwind of yesterday’s massive short-squeeze causing FANG stocks to chuck-up the hardest.

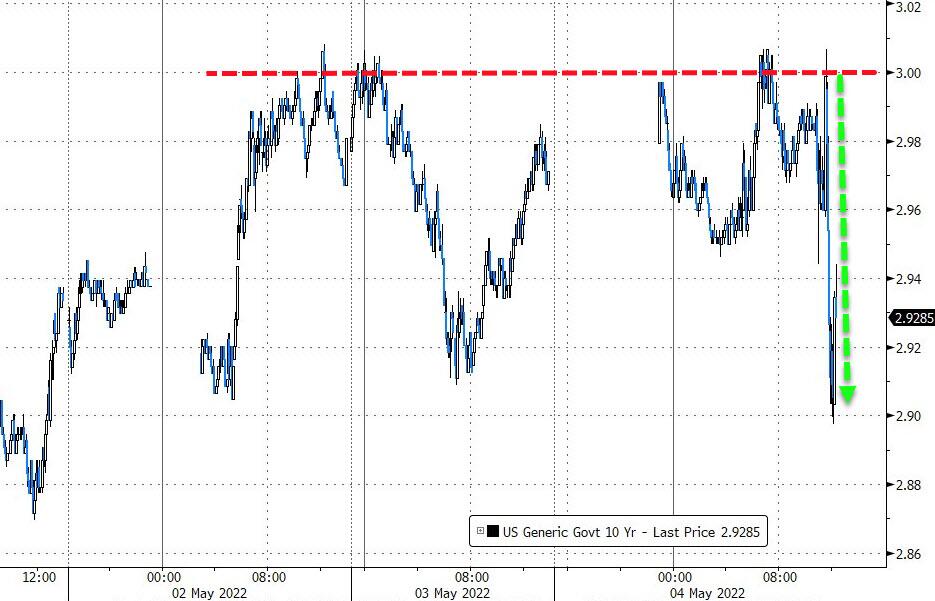

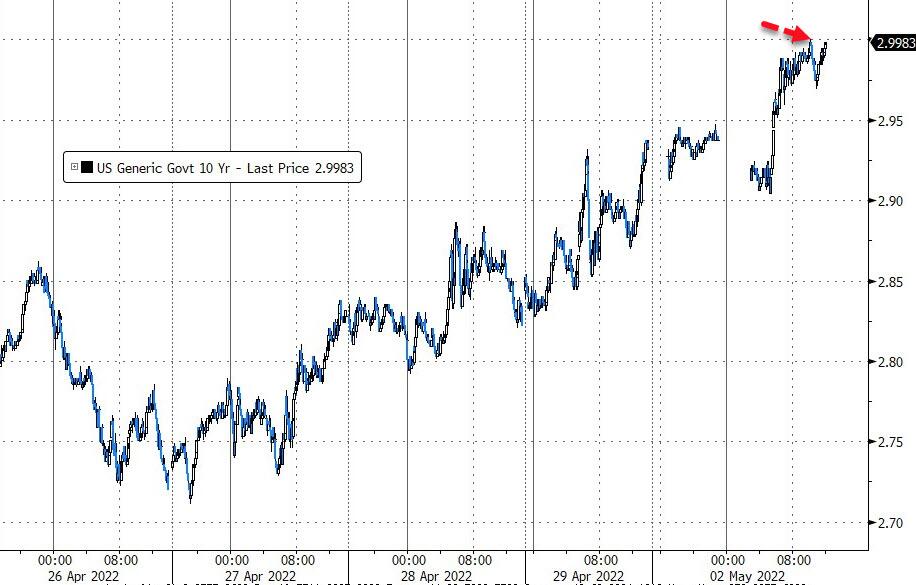

Spiking bond yields were at the center of today’s debacle with the 10-year breaking through the 3% barrier and closing up 8.2 bps at 3.045%.

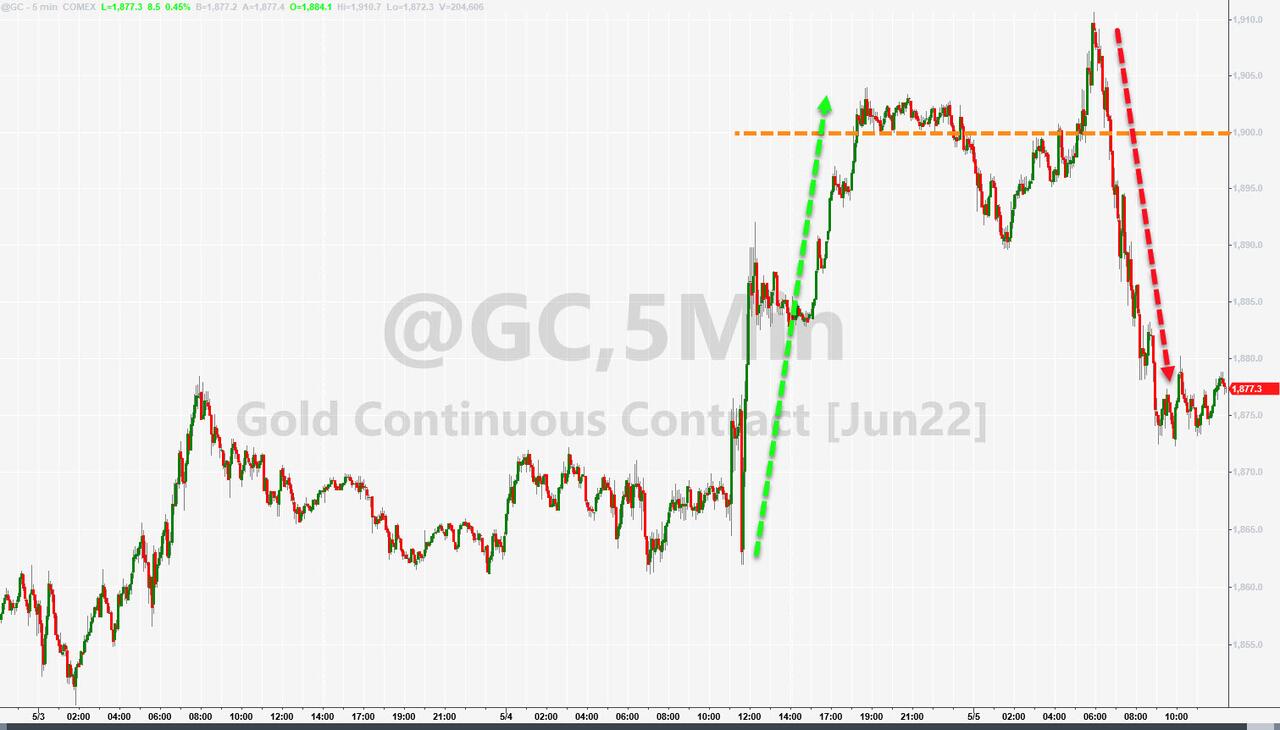

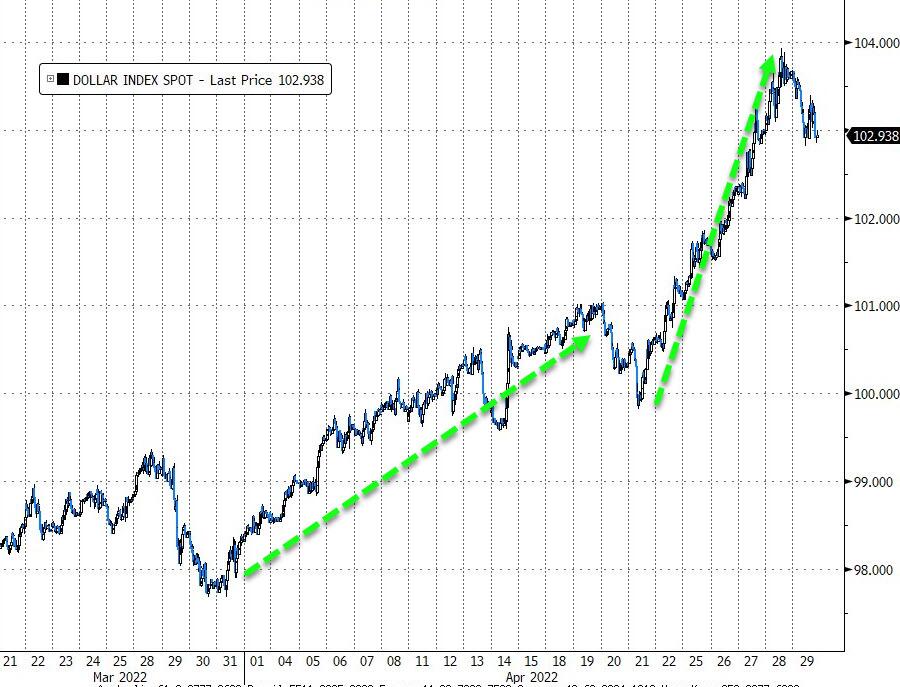

The US Dollar rebounded after yesterday’s losses, Gold jumped but could not hold on to early gains, but Crude Oil ended the day higher.

It was a wild and crazy session in the markets, and I believe this type of uncertainty is far from being over.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}