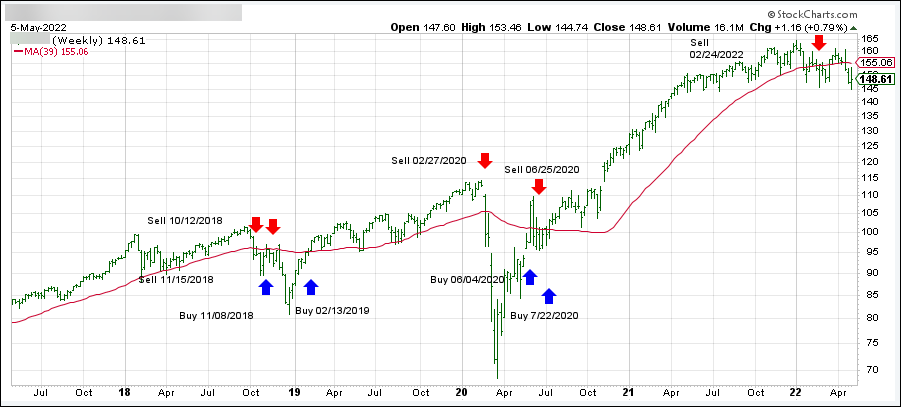

- Moving the markets

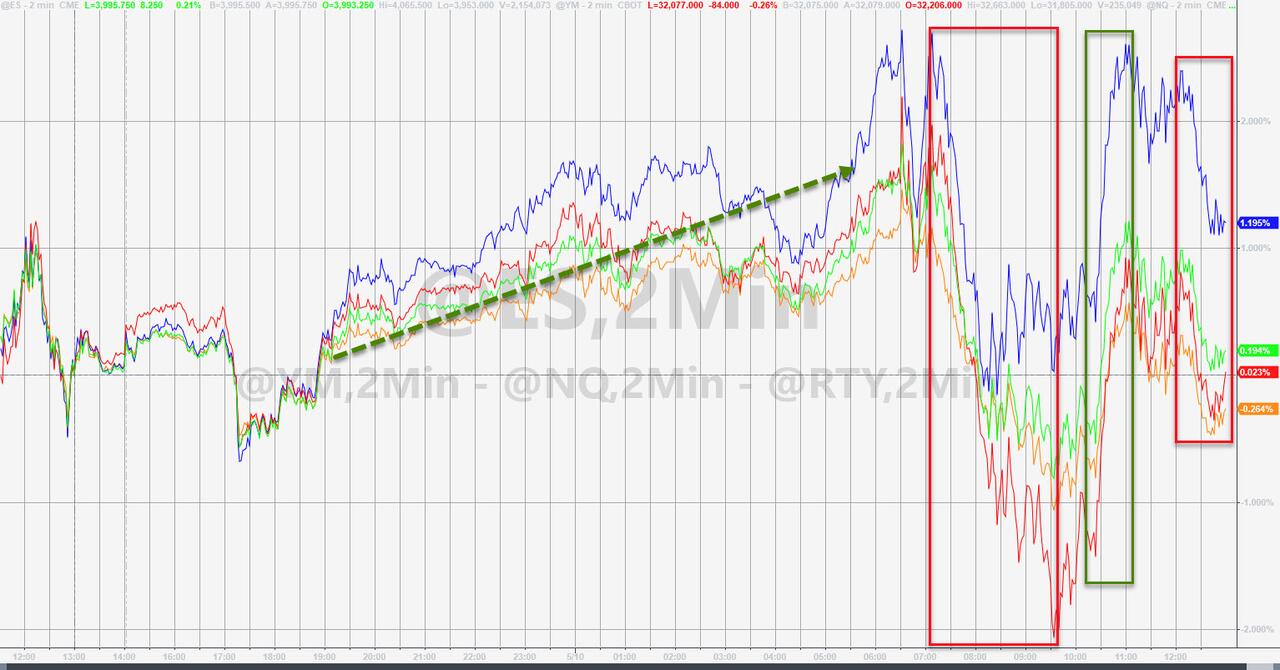

The pattern, that early ramps get wiped out during the session, has been occurring with such regularity, that we could conclude that they are merely dead-cat-bounces, i.e., hopeful leaps with no connection to reality.

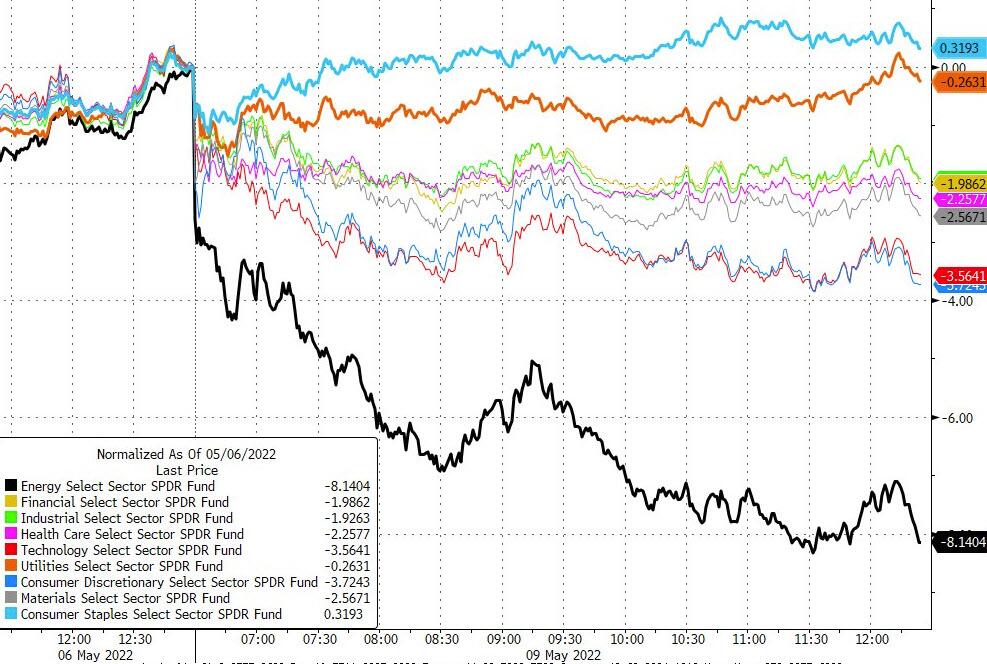

Today was no exception. The chart above clearly demonstrates that occurrence and here again, the major indexes got spanked, despite a late day rebound above the unchanged line.

As ZeroHedge pointed out, today is the biggest 5-day drop for stocks since 3/20/20, with the S&P 500 now clearly having lost its 4k level:

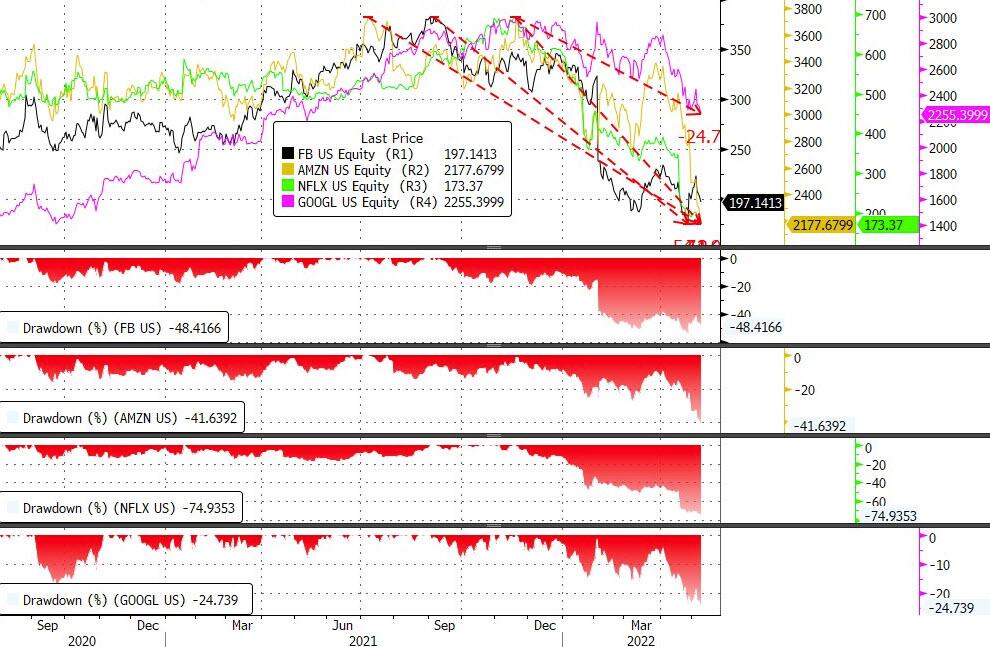

- Nasdaq is now down over 29% from its highs, Dow down over 17%, and the S&P almost 14%.

Today’s April CPI report of 8.3% YoY, while an improvement from March’s 8.5%, was higher than the expected 8.1%. Hope that inflation may have peaked, was nothing but wishful thinking, and that reality set in later and pulled the major indexes into the red.

As I have repeatedly said, the Fed is way behind in its attempts to curb inflation, and a far more aggressive approach is needed to not only conquer the price increases we are experiencing now—but also to get a handle on potential hyperinflation and a cost-of-living crisis. A puny 0.5% hike in the Federal Funds rate will not do it.

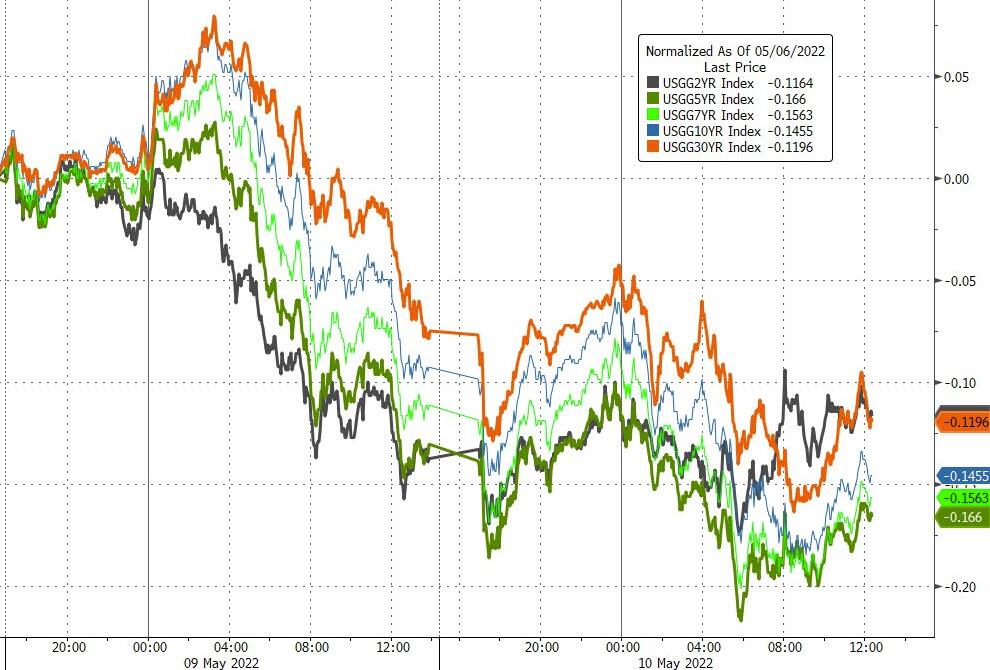

Bond yields spiked but pulled back late in the session, with the 10-year retreating from its 3.06% intra-day high to close down 7 bps at 2.93%.

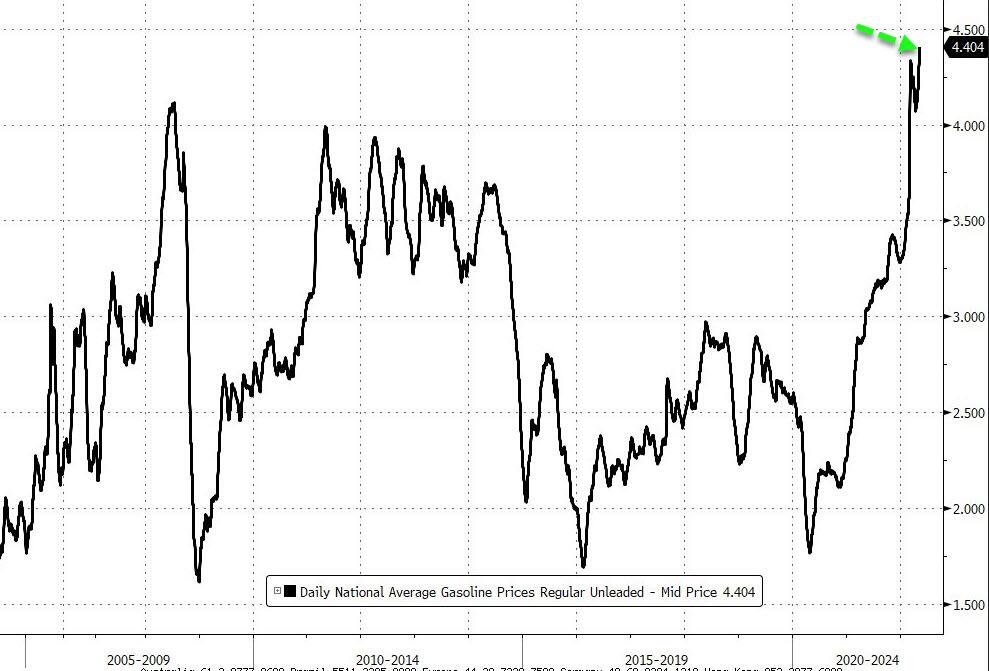

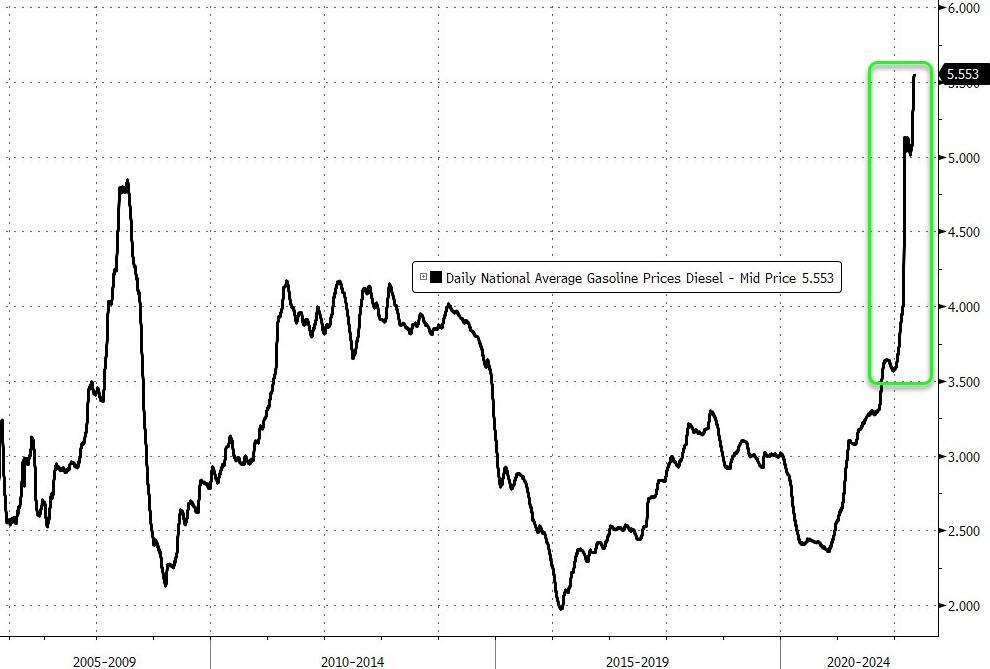

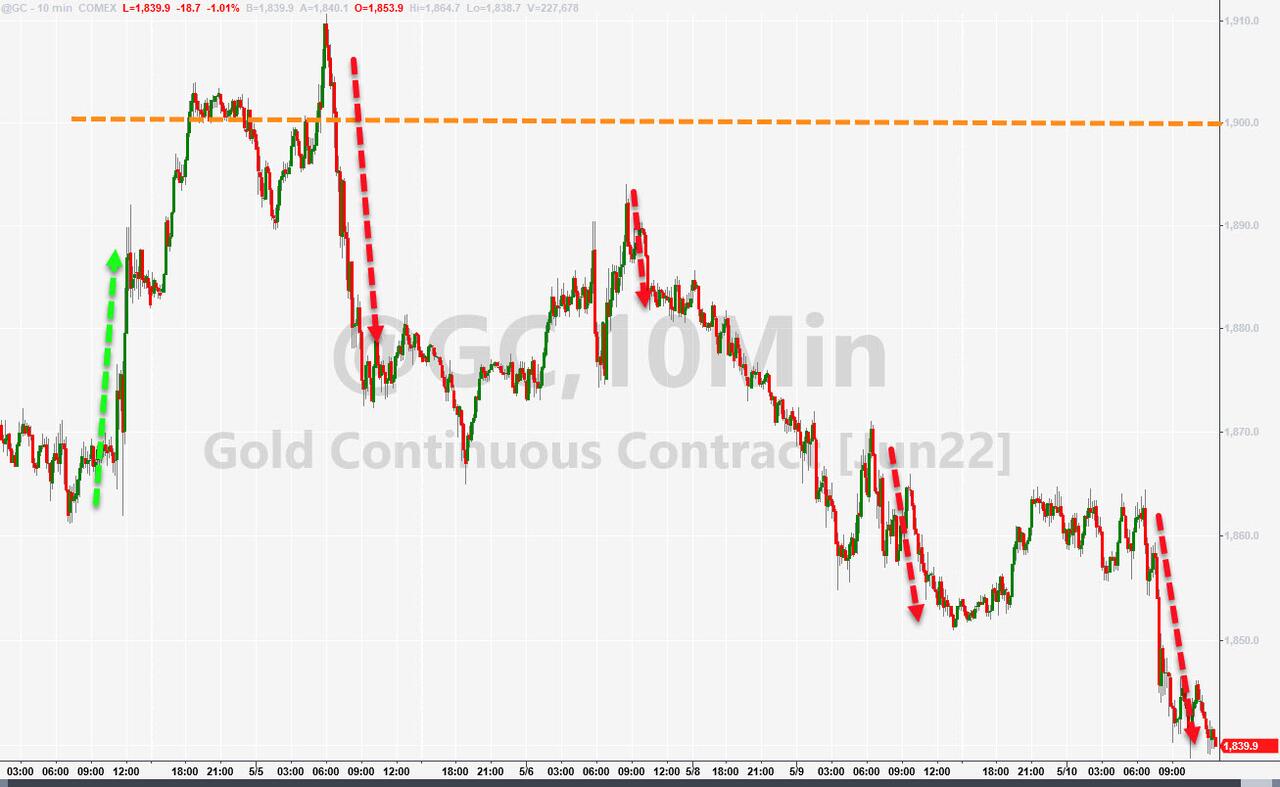

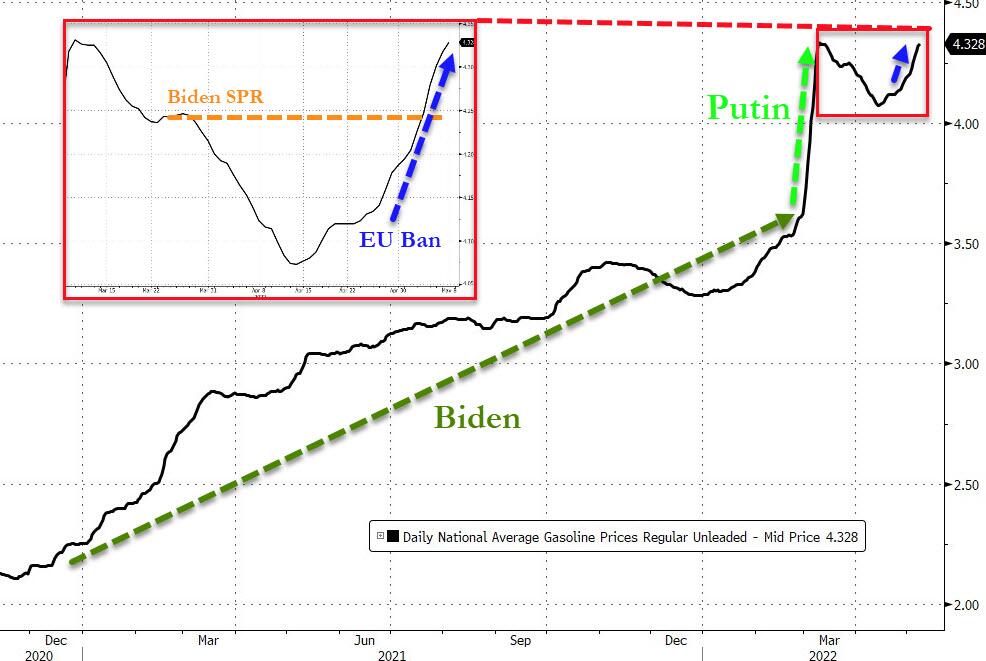

Crude Oil bounced back above $100, gold had a decent showing, but is still trying to climb back above its $1,900 level, and retail gasoline prices set a new record. More astounding was the price of Diesel fuel, which absolutely exploded.

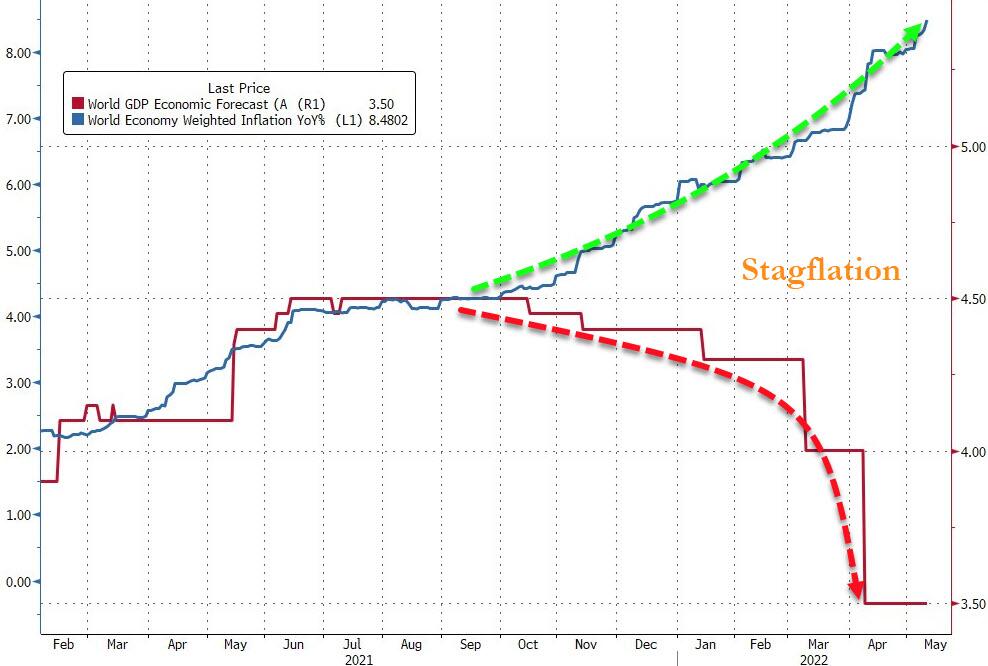

Having said all that, the dreaded “S” word, as in Stagflation (inflation + no growth), is making the rounds again, with Bloomberg producing this chart as evidence.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}