[Chart courtesy of MarketWatch.com]

- Moving the market

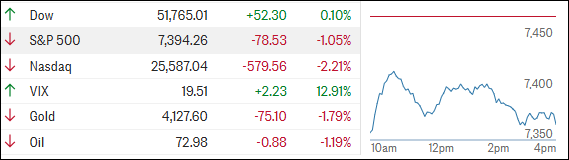

Stocks came under pressure right out of the gate as a tech sell-off from the previous session gained momentum overnight. Weakness in Asia set the tone, with memory chip stocks getting hit hard and dragging global markets lower.

The Nasdaq took the biggest hit, falling 1.3% on Monday, weighed down largely by Alphabet. Selling pressure then spread across the globe, with South Korea’s Kospi leading the decline as chip-related names got routed.

{kind=link}

That weakness carried into U.S. trading. Micron dropped 10%, Sandisk slid 12%, and Seagate lost more than 7%. Intel was off 3%, while AMD and Qualcomm fell 5% and 9%, respectively. Alphabet continued to struggle after Monday’s 5% drop, as concerns linger about key AI talent leaving the company.

By the close, what started as a regional tech sell-off turned into a broader hit to U.S. big tech, with the Nasdaq leading losses while the Dow managed to finish roughly flat.

On the macro side, the data didn’t do the market any favors. Philly Fed Services and manufacturing/business conditions came in weak, though the U.S. PMI surprised to the upside, hitting a five-month high thanks to stronger manufacturing and some easing in price pressures.

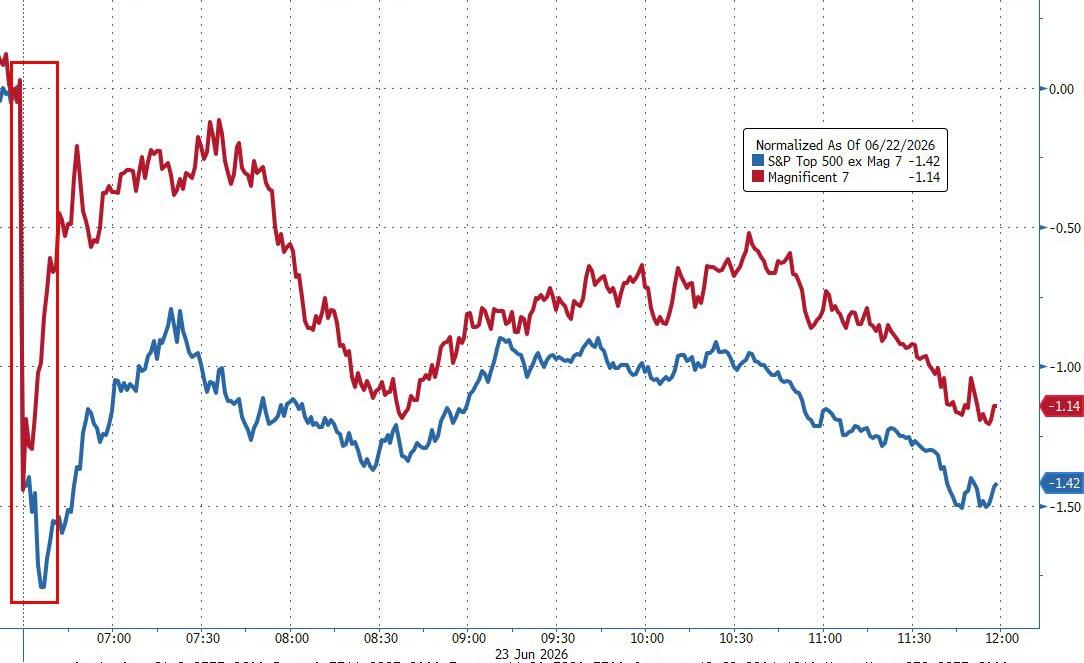

Elsewhere, slightly lower oil prices added to the cautious mood, and interestingly, the “S&P 493” actually underperformed the Mag 7—a reversal of the usual trend.

{kind=link}

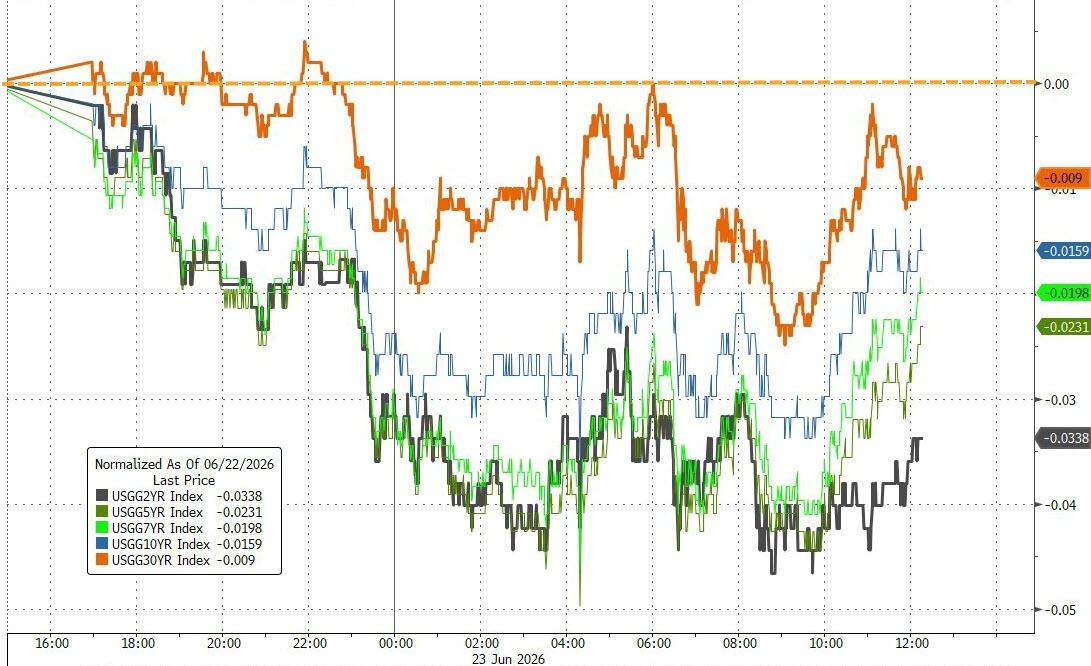

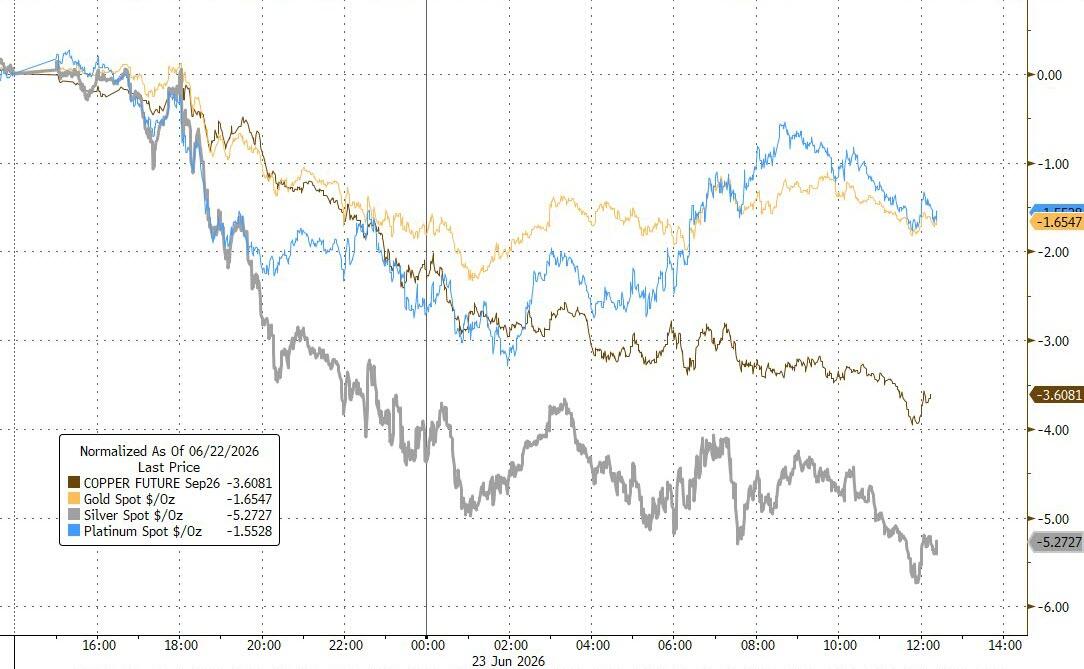

Bond yields edged lower, the dollar continued to climb, and that combination weighed on precious metals, with silver taking the biggest hit. Gold managed to hold near $4,100, while Bitcoin hung onto the $62K level—for now.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

At the end of the day, there really wasn’t much of a safe haven, leaving traders on edge and wondering how equities might react if the Fed follows through with potential rate hikes in September and December, especially with inflation still showing signs of stickiness.

So, the question is: are we just seeing a temporary shakeout in tech, or is this the start of a bigger reset for the market?

2. Current domestic “Buy” Cycle (effective 5/20/2025); International “Buy” Cycle (effective 5/8/25)

Our domestic bullish cycle that began on November 21, 2023, concluded on April 3, 2025, following a market downturn triggered by President Trump’s tariff policy announcement.

This development caused significant declines across major indexes and broader market indices. However, markets subsequently rebounded, culminating in a new domestic “Buy” signal taking effect May 20, 2025.

Concurrently, our International Trend Tracking Index (TTI) experienced parallel volatility. On April 4, 2025, it breached critical thresholds, prompting a “Sell” recommendation. This position reversed as global markets recovered, with the International TTI regaining sufficient momentum to issue a new “Buy” signal effective May 8, 2025.

3. Trend Tracking Indexes (TTIs)

Markets opened on a weak note, and the bulls never really showed up. The overnight sell-off in Asia set the tone, and the bears stayed firmly in control throughout the session.

Most markets took a beating, with the Dow being the lone exception that managed to avoid the worst of the damage.

The metals complex didn’t fare much better, and both of our TTIs finished the day in the red.

That said, it’s worth highlighting that the domestic TTI held up relatively well, especially when compared to its international counterpart.

This is how we closed 06/23/2026:

Domestic TTI: +6.57% above its M/A (prior close +6.93%)—Buy signal effective 5/20/25.

International TTI: +6.78% above its M/A (prior close +8.01%)—Buy signal effective 5/8/25.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

———————————————————-

WOULD YOU LIKE TO HAVE YOUR INVESTMENTS PROFESSIONALLY MANAGED?

Do you have the time to follow our investment plans yourself? If you are a busy professional who would like to have his portfolio managed using our methodology, please contact me directly to get more details.

Contact Ulli