[Chart courtesy of MarketWatch.com]

- Moving the market

The major indexes started the morning on the upswing, helped by falling oil prices and some cautious optimism ahead of Micron’s earnings after the close.

Energy stocks, however, didn’t share in the upbeat start. Big names like Exxon, Chevron, and ConocoPhillips each dropped more than 2%, while SLB fell over 3%. The broader energy ETF (XLE) was down nearly 2%, reflecting the pressure across the sector.

In tech, Micron slipped about 1% heading into its report, with peer Sandisk also edging lower. Both stocks are still recovering from a brutal 13% drop in the prior session.

This follows Tuesday’s tech-led selloff that dragged down both the S&P 500 and Nasdaq. Many traders are viewing this pullback as a healthy reset after a strong run, especially with valuations stretched and earnings expectations running high.

With earnings season picking up again in July, the bar for tech companies may be tougher to clear than investors would like.

Just like yesterday, the Nasdaq led the downside move, while the Dow managed to squeeze out a modest gain. The Mag 7 once again lagged the broader market, adding to the pressure.

{kind=link}

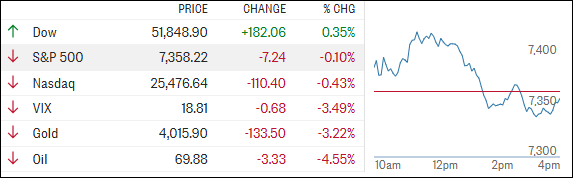

Elsewhere, oil continued to retreat, with WTI falling back toward the $70 level—its lowest since the U.S.-Iran conflict began—as supply conditions appear to be improving faster than expected.

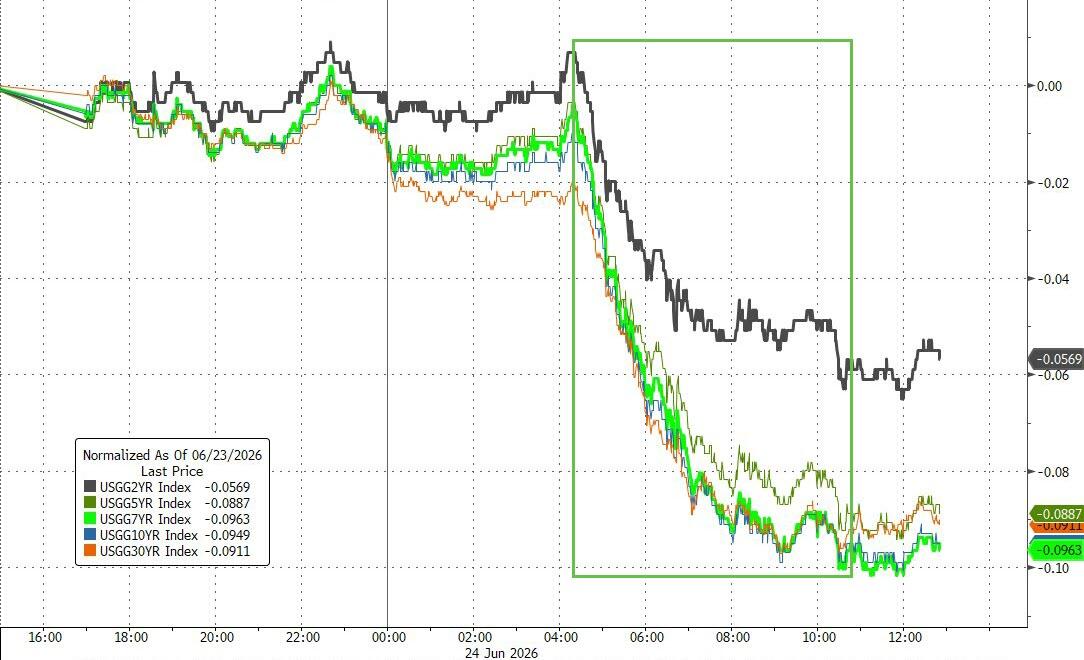

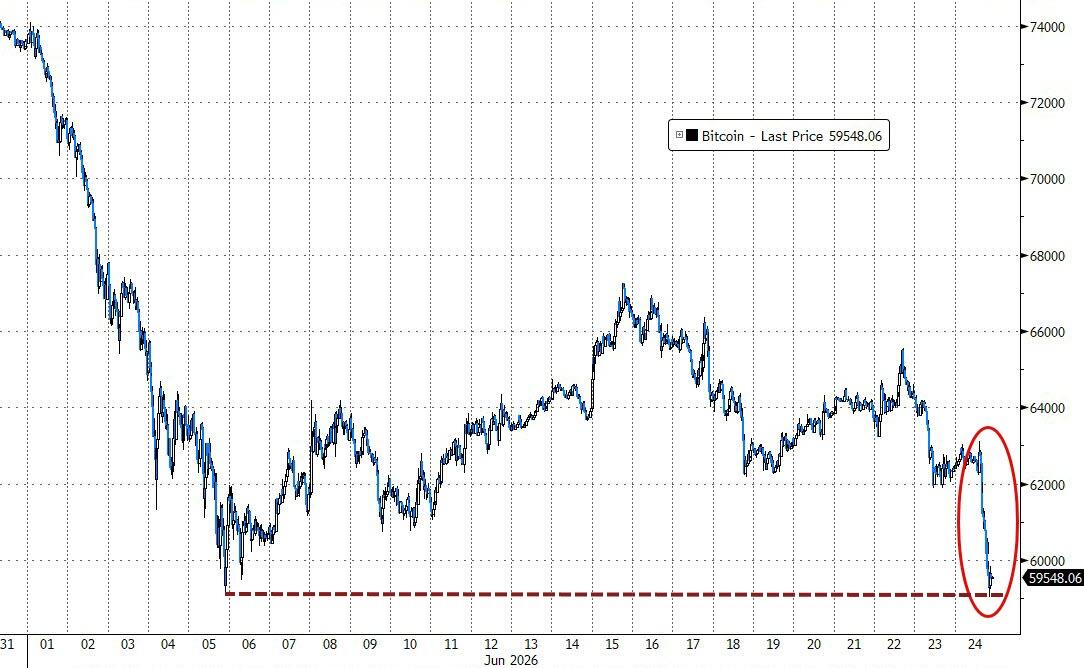

Bond yields eased, but the dollar kept climbing, hitting its highest level in 13 months. Gold dipped below $4,000 for the first time since November 2025 before closing just above that level, while Bitcoin took a hit as well, briefly dropping below $60K and testing support at its June lows.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Despite the ongoing correction in metals, one interesting development stands out: China imported 163 tons of gold in May—the highest level in over two years.

Which raises an intriguing question: Why is China buying aggressively while U.S. investors seem to be heading for the exits?

2. Current domestic “Buy” Cycle (effective 5/20/2025); International “Buy” Cycle (effective 5/8/25)

Our domestic bullish cycle that began on November 21, 2023, concluded on April 3, 2025, following a market downturn triggered by President Trump’s tariff policy announcement.

This development caused significant declines across major indexes and broader market indices. However, markets subsequently rebounded, culminating in a new domestic “Buy” signal taking effect May 20, 2025.

Concurrently, our International Trend Tracking Index (TTI) experienced parallel volatility. On April 4, 2025, it breached critical thresholds, prompting a “Sell” recommendation. This position reversed as global markets recovered, with the International TTI regaining sufficient momentum to issue a new “Buy” signal effective May 8, 2025.

3. Trend Tracking Indexes (TTIs)

The major indexes kicked things off on a positive note, but that optimism didn’t last long. By the close, most had slipped into the red, with only the Dow managing to hang on for a small gain.

Tech stocks took another hit—though not as hard as yesterday—while both metals and Bitcoin were under pressure and drifted lower.

Our TTIs told a mixed story again: the domestic index put in a solid gain, while the international one mostly just spun its wheels.

This is how we closed 06/24/2026:

Domestic TTI: +7.31% above its M/A (prior close +6.57%)—Buy signal effective 5/20/25.

International TTI: +6.60% above its M/A (prior close +6.78%)—Buy signal effective 5/8/25.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

———————————————————-

WOULD YOU LIKE TO HAVE YOUR INVESTMENTS PROFESSIONALLY MANAGED?

Do you have the time to follow our investment plans yourself? If you are a busy professional who would like to have his portfolio managed using our methodology, please contact me directly to get more details.

Contact Ulli