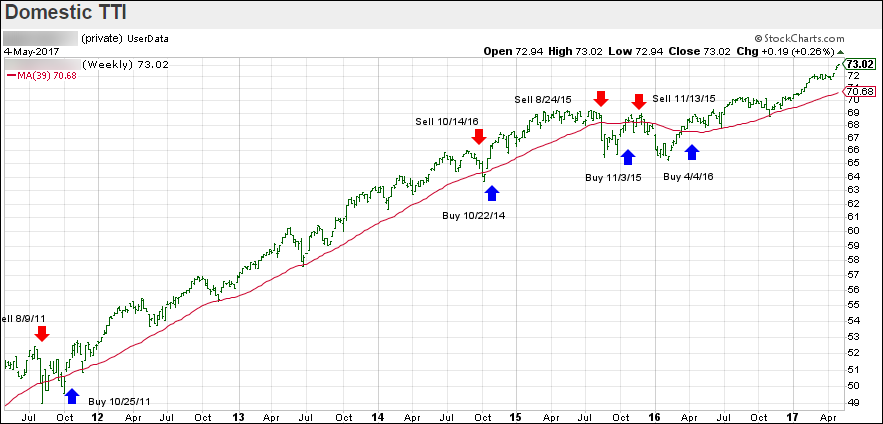

ETF Tracker StatSheet

https://theetfbully.com/2017/05/weekly-statsheet-etf-tracker-newsletter-updated-05042017/

TUG OF WAR: STRONG JOBS REPORT VS. FRENCH ELECTIONS

- Moving the Markets

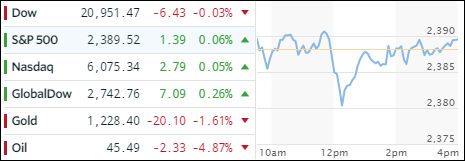

It was a tug of war as a strong jobs report battled for market direction against the uncertainty of the second and final round of the upcoming French elections. For the day, the on the surface positives of the jobs report were the winner as equities picked up some stream and closed higher with the S&P 500 knocking on the 2,400 milestone marker.

The jobs report showed that April payrolls jumped by 211,000 beating expectations and providing some relief after March’s disappointing revised 79,000 number. The disappointing part was that, despite strong jobs growth, hourly earnings were soft rising only 2.5% YoY vs. an expected 2.7%. So, why is it that in a labor market with alleged full employment wages simply can’t rise? The answer is clear and has to do with the quality of jobs, as most of them once again were in low or minimum-wage sectors aka waiters and bartenders.

ZH summed up today’s session as follows:

Massive liquidity issues in China wealth product liquidation, commodities crashing, oil plunging, US macro data disappointments, US earnings disappointments, and Buffett dumping Big Blue – only makes sense that The Dow just had its quietest 8 days since 1952!

US Macro data has negatively surprised for 7 straight weeks – dropping to its weakest since October…

Shown in a graph, it looks like this: