- Moving the market

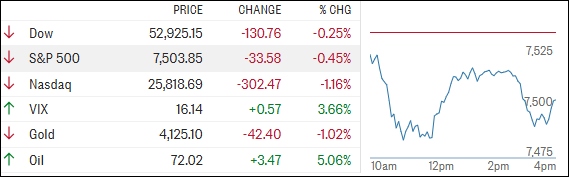

The Dow pulled back from record highs early on as traders once again rotated out of AI-related stocks and grappled with rising oil prices and higher bond yields.

{kind=link}

The selling pressure was especially noticeable in the semiconductor space. Micron dropped 7%, while KLA, Marvell Technology, Broadcom, and AMD also moved lower. The VanEck Semiconductor ETF (SMH) lost more than 5%, highlighting the broad weakness across the chip sector.

Investor sentiment took another hit after reports that Iran attacked a Qatari liquefied natural gas tanker near the Strait of Hormuz. The escalation pushed energy prices higher, with Brent crude climbing more than 2% to trade above $73 a barrel.

The weakness in AI-related stocks actually started overseas. South Korea’s Kospi index tumbled nearly 5%, led by a sharp decline in Samsung Electronics. Despite reporting a strong jump in second-quarter profit, concerns about future spending and demand overshadowed the positive earnings news.

Adding to the uncertainty, reports surfaced that DeepSeek is developing its own AI chip. If successful, that move could reduce its reliance on suppliers such as Nvidia and Samsung, raising fresh concerns about future demand for some of the industry’s biggest chipmakers. Nvidia shares also finished lower on the day.

By the closing bell, markets were struggling to absorb a combination of rising oil prices, higher bond yields, and growing inflation expectations. The dollar spent much of the session drifting sideways before surging into the close.

{kind=link}

{kind=link}

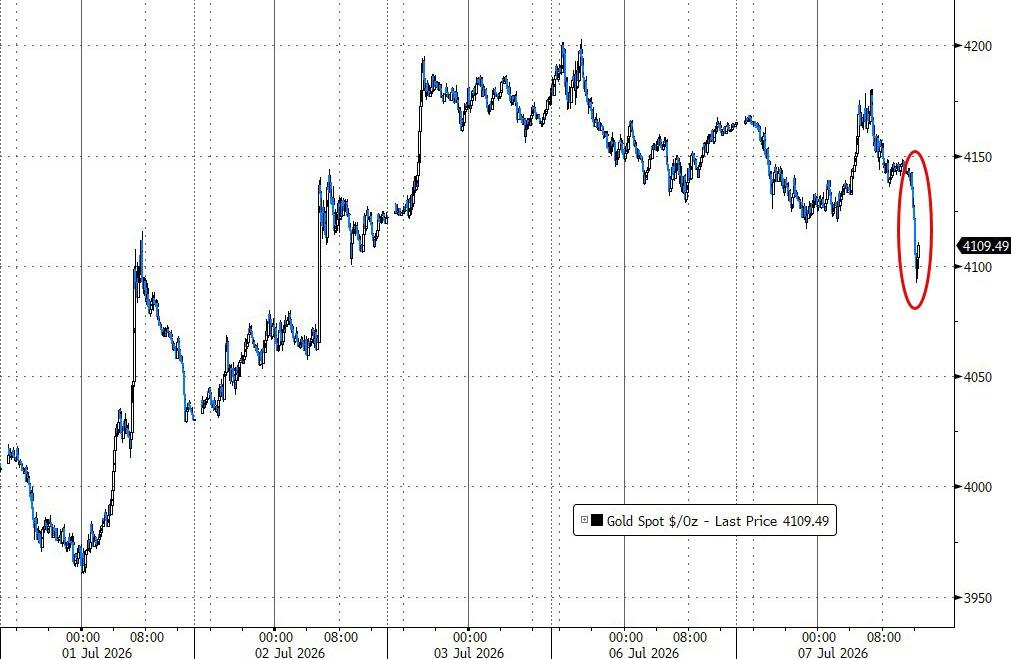

That late-day dollar strength took much of the momentum out of an early gold rally, sending the precious metal back toward the $4,100 level.

{kind=link}

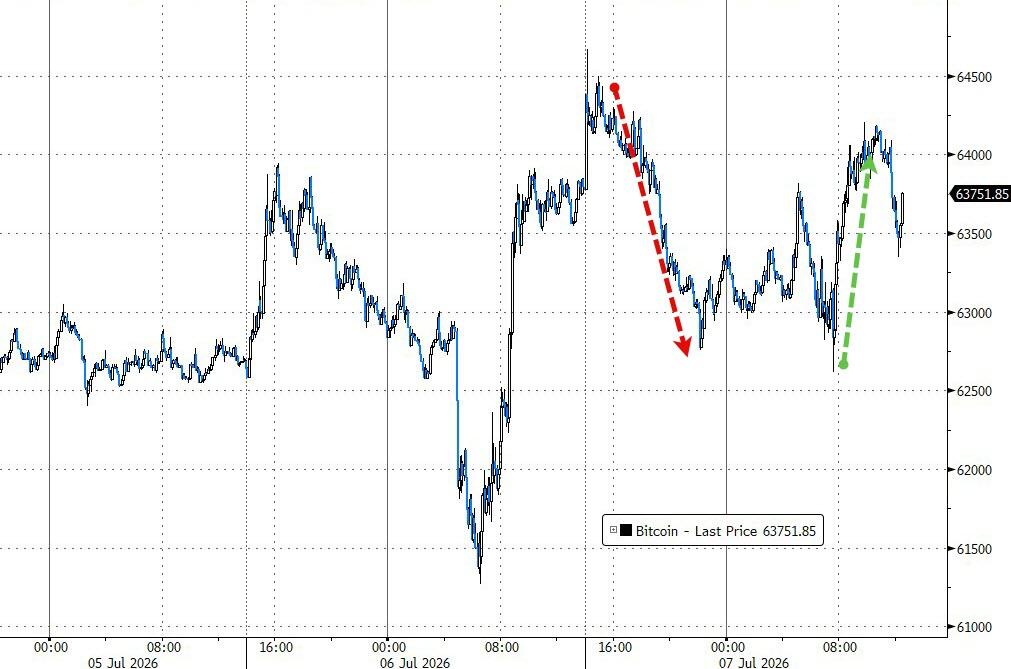

Bitcoin experienced its own rollercoaster session, swinging between $62,500 and $64,500 before finishing little changed.

{kind=link}

With geopolitical tensions in the Middle East heating up and traders facing a growing list of macroeconomic headwinds, the big question is whether the upcoming earnings season can provide enough fuel to keep the market’s longer-term uptrend intact.

2. Current domestic “Buy” Cycle (effective 5/20/2025); International “Buy” Cycle (effective 5/8/25)

Our domestic bullish cycle that began on November 21, 2023, concluded on April 3, 2025, following a market downturn triggered by President Trump’s tariff policy announcement.

This development caused significant declines across major indexes and broader market indices. However, markets subsequently rebounded, culminating in a new domestic “Buy” signal taking effect May 20, 2025.

Concurrently, our International Trend Tracking Index (TTI) experienced parallel volatility. On April 4, 2025, it breached critical thresholds, prompting a “Sell” recommendation. This position reversed as global markets recovered, with the International TTI regaining sufficient momentum to issue a new “Buy” signal effective May 8, 2025.

3. Trend Tracking Indexes (TTIs)

Bears were in control for most of the session, pressuring the major indexes from the opening bell and ultimately driving them to a lower close.

A stronger U.S. dollar and rising bond yields also weighed on the metals complex, leading to a modest pullback in our TTIs as well.

This is how we closed 07/07/2026:

Domestic TTI: +9.26% above its M/A (prior close +9.39%)—Buy signal effective 5/20/25.

International TTI: +7.45% above its M/A (prior close +7.94%)—Buy signal effective 5/8/25.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

———————————————————-

WOULD YOU LIKE TO HAVE YOUR INVESTMENTS PROFESSIONALLY MANAGED?

Do you have the time to follow our investment plans yourself? If you are a busy professional who would like to have his portfolio managed using our methodology, please contact me directly to get more details.

Contact Ulli