- Moving the Markets

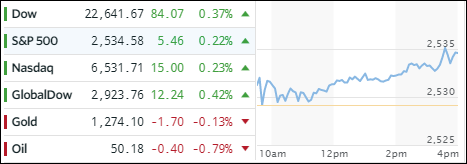

Even though today’s gains were modest, they were gains nonetheless. The major indexes continued their ascent into record territory despite a slow start right after the opening. However, in the end, the S&P 500 posted its sixth consecutive day of gains.

Private sector employment slowed from September with 150k jobs added. All eyes are now on Friday’s nonfarm payroll report, the outcome of which could drive markets higher. On the other hand, no matter what the number, the markets may rally anyway; it’s just the “new normal” type of environment we’re in.

The shocker of the day and the moment of truth came from SmallCaps, which actually ended the day lower with the Russell 2000 diving an incredible -0.25%, its worst drop in over a month… of course, I am being facetious…

In ETF land, the picture was mixed but the outcome of the session was overall positive. The Aerospace and Defense ETF (ITA) came in first place with a gain of +0.31%. Second place was a tie with Semiconductors (SMH) and Emerging Markets (SCHE) each adding +0.15%. Closing in the red was the Transportation Index (IYT) with -0.49% and US SmallCaps (SCHA) with -0.22%.

Interest rates changed immaterially, gold edged higher, oil slipped back below $50, and the US dollar (UUP) pulled back a tiny -0.12%.