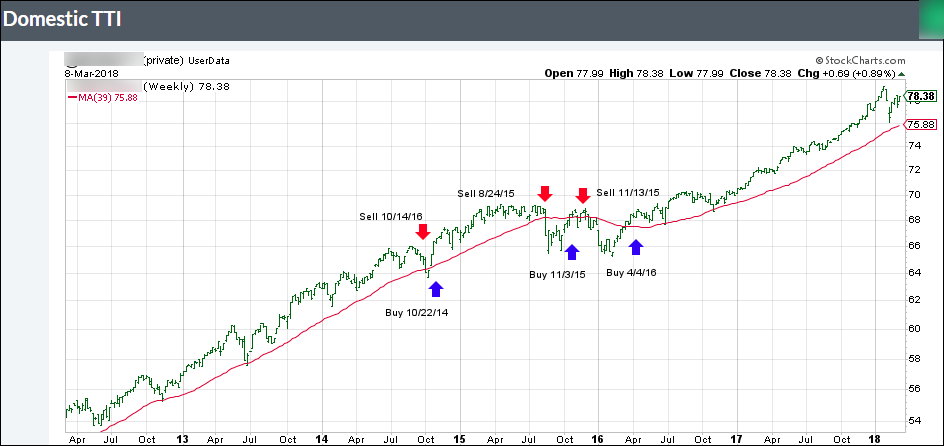

ETF Tracker StatSheet

https://theetfbully.com/2018/03/weekly-statsheet-etf-tracker-newsletter-updated-03-08-2018/

A ONE WAY STREET FOR THE BULLS

- Moving the markets

Forget the concerns of the past week. Things like tariffs, trade wars, rising bond yields and Gary Cohn’s exit from the White House appear to be in the rear view mirror, as the non-farm payroll report took front and center, which ZH summarized as follows:

While the headline payroll print of 313K was impressive, a look under the cover reveals even stronger data: first, the Household Survey showed that a whopping 785K jobs were added in February, while the number of unemployed Americans rose by only 22K, and with the labor force rising by 806K, this explains why the unemployment rate remained unchanged at 4.1%.

But what is even more notable is that when looking at the breakdown of job additions, one finds that in February, a near record 729K full-time jobs were added, the biggest monthly increase since last September’s 794K…

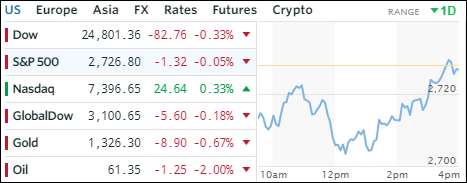

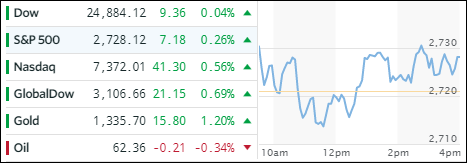

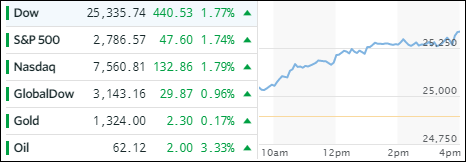

The bulls licked their chops and upward momentum went into overdrive despite the fly in the ointment being a total lack of wage growth, but hey, who cares about such trivia as the major indexes rallied without a pause with the Dow reclaiming its 25k level. The Wall Street mood was upbeat and remained that way despite the 10-year bond yield adding 4 basis points to end the week at 2.90%.

Notwithstanding the ups and downs all week, the US Dollar managed to close unchanged over the past 5 trading sessions. Looking towards next week, I am curious to see if this rally has legs and can lead us towards taking out the old highs.