[Chart courtesy of MarketWatch.com]

- Moving the markets

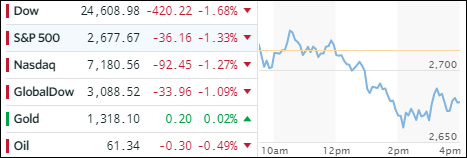

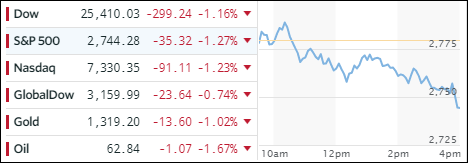

Today, it was economic data points that caused increased market volatility and sent the major indexes into a tailspin closing at the lows of the day. We started the session on a positive note, then bounced around the unchanged line for a while and finally accelerated to the downside with the S&P and Dow registering its worst month in two years.

Today, as well as for most of the month, there was no place to hide, with MarketWatch summing it up best:

Equities have struggled throughout February, with the Dow and the S&P 500 dropping into correction territory earlier this month, defined as a 10% drop from a recent high. The monthly losses were broad, with all 11 primary S&P 500 industry groups closing in negative territory.

With comments from new Fed chief Powell having sparked yesterday’s sell-off, today the culprit appeared to be poor economic data. First, GDP growth was reduced to 2.5% from 2.6% in the fourth quarter. This was followed by the Chicago PMI, which slipped to a six-month low in February, and Pending home sales, which plunged the most since 2010 (-4.7% in January vs. an expected +0.5%).

Surprisingly, bad news like these, are suddenly perceived as actually being bad news, while similar poor economic readings were simply overlooked during the past year as the bull market raged on. Maybe we have now reached a point where a sense of reality not only has set in but needs to be dealt with.

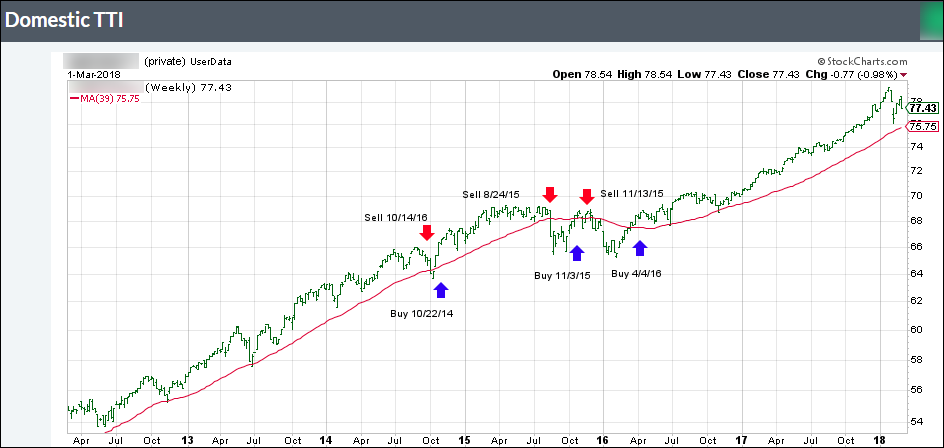

In terms of overall market direction, we are still bullish but have to be aware that this situation could change and that the bounce-back of the past 3 weeks really has legs and is not a just continuation of the short-term downtrend started early in February. After all, in the early phase potential bear markets start slowly and demonstrate violent rebound abilities.

Read More