- Moving the markets

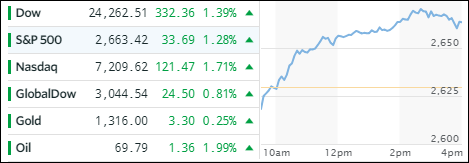

Muted inflation fears were one part of the puzzle that helped the markets score another win with the major indexes gaining across the board.

First, today’s reading on April consumer prices came in at +0.1%, which was a tad below estimates. Second, the 10-year bond yield pulled back and did not close above the much feared 3% level. Third, to make sure the markets were going to close in the green, the VIX was clubbed again and tumbled to 12 from yesterday’s 13 level.

This triple combination was enough to control any bearish thoughts and let the bulls have another chest pounding session. Even news headlines that 2 of the biggest hedge fund managers opined that “This is not a time to be rewarded for long market exposure…” while announcing their increased short holdings, did nothing to reduce the bullish fever—at least not yet.

Despite market anxieties appearing to have taken a step back, the jury is still out as to whether this will be a resumption of the prior bull market or, as some fund managers believe, simply a sign of a blow off top.

While gold and oil edged higher as well, the US Dollar (UUP) got spanked and lost -0.47%, its biggest drop in 2 months. However, due to its recent rebound, UUP is still positioned on the positive side of its 50- and 200-day M/As.