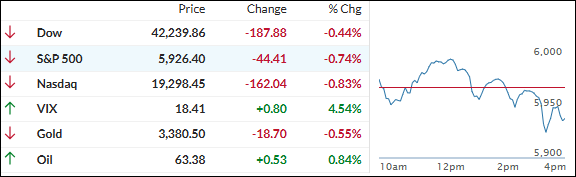

The day started off on shaky ground, with markets slipping early as fresh trade headlines put a lid on any bullish momentum.

China’s Foreign Ministry said Presidents Trump and Xi had a phone call—initiated by Trump—but details were scarce. Trump called it a “very positive conclusion,” but investors weren’t exactly buying it.

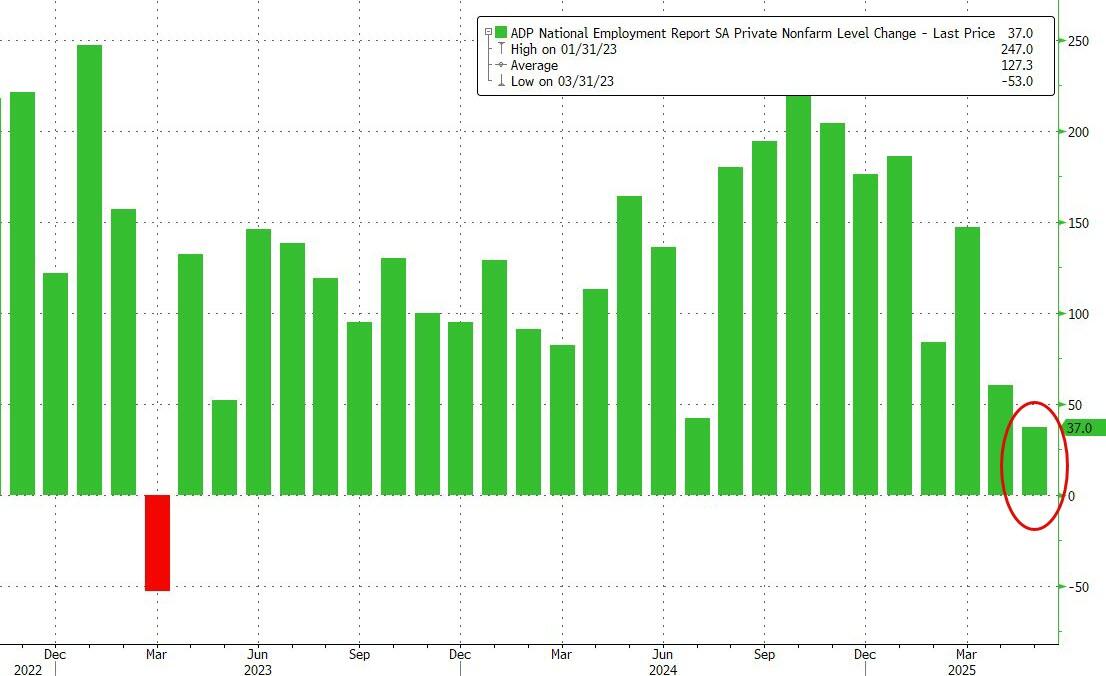

On the economic front, jobless claims ticked up to 247,000 last week—8,000 more than the previous week and above the expected 236,000. Combined with weaker-than-expected ADP private payroll data, all eyes are now on tomorrow’s official jobs report, where the forecast is for a 125,000 gain.

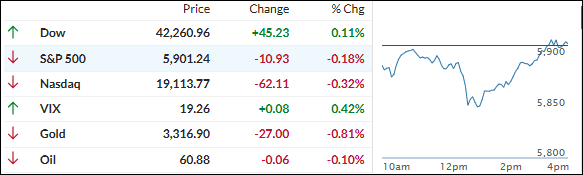

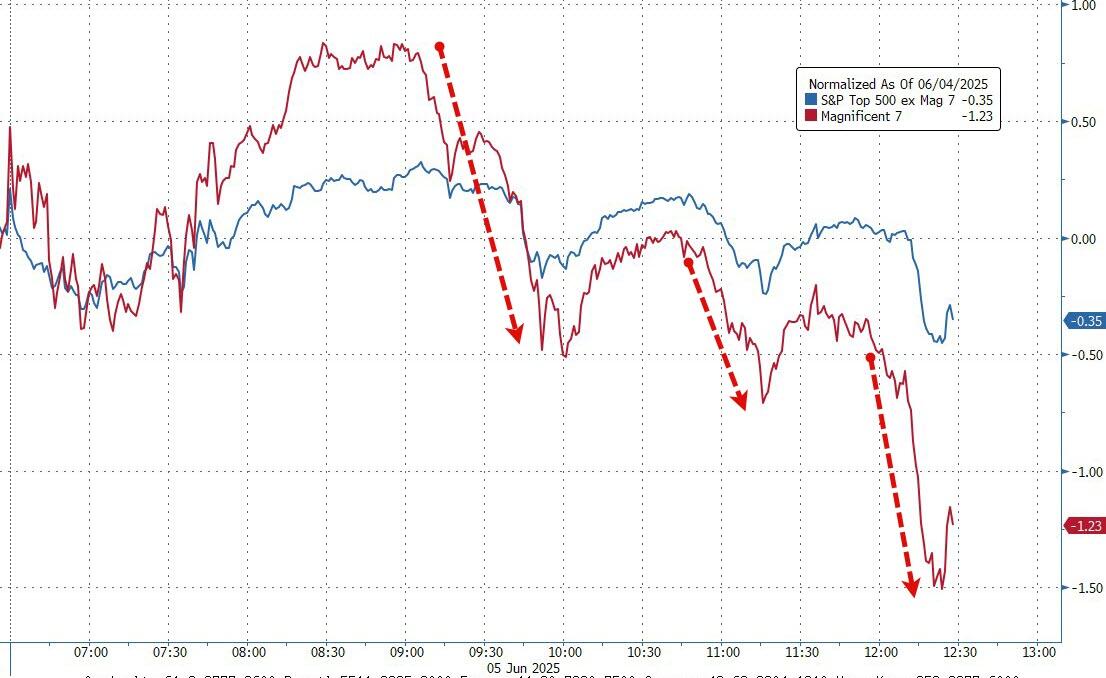

Then things really unraveled. The ongoing slugfest between Trump and Musk escalated dramatically, sending Tesla shares tumbling over 17%. Retail investors, many of whom had been buying the recent dips, got caught in the crossfire. The MAG 7 stocks underperformed the rest of the S&P 500, as the tweet storm reached a fever pitch.

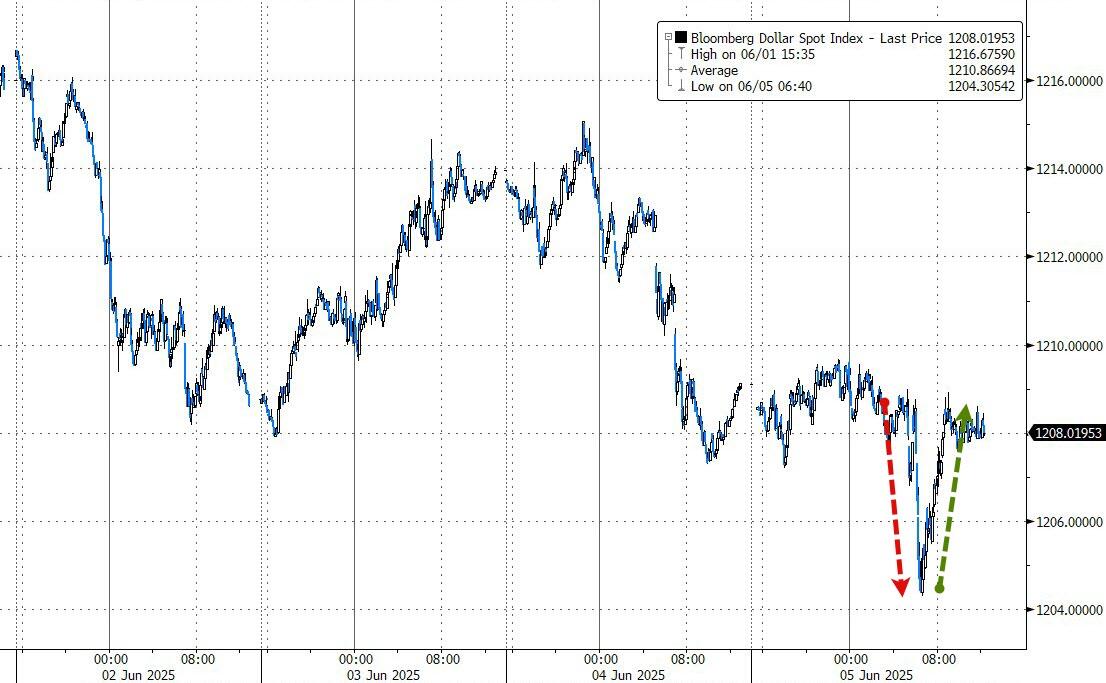

Bond yields reversed course and climbed into the close. Gold started strong but faded, ending lower. The dollar took a wild ride—first dropping, then surging. Bitcoin lost its footing and fell to a three-week low.

The one bright spot? Silver, which spiked 3.5% and stood out in an otherwise gloomy session.

With all this turbulence, the big question now is: Will tomorrow’s jobs report calm the markets—or add more fuel to the fire?

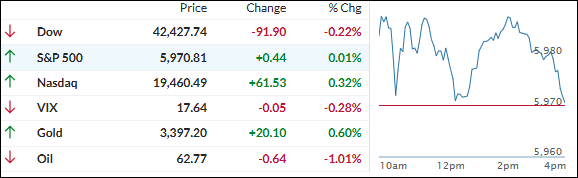

Despite a weak jobs report, stocks opened higher. ADP reported that private sector hiring added just 37,000 jobs in May—way below the already-lowered April figure of 60,000 and far short of the 110,000 economists were expecting. That’s raising eyebrows ahead of Friday’s big non-farm payroll report, which is forecast to show a gain of 125,000.

The disappointing data put a dent in the “strong labor market” narrative. In fact, the surprise index dropped to levels we haven’t seen since before the 2024 election. That prompted a fiery tweetstorm from Trump, pressuring Fed Chair Powell to cut rates.

Tech stocks tried to keep the mood upbeat. Nvidia and Broadcom led the charge again, helping the Nasdaq close in the green. But the Dow and S&P 500 couldn’t keep up and ended the day mixed.

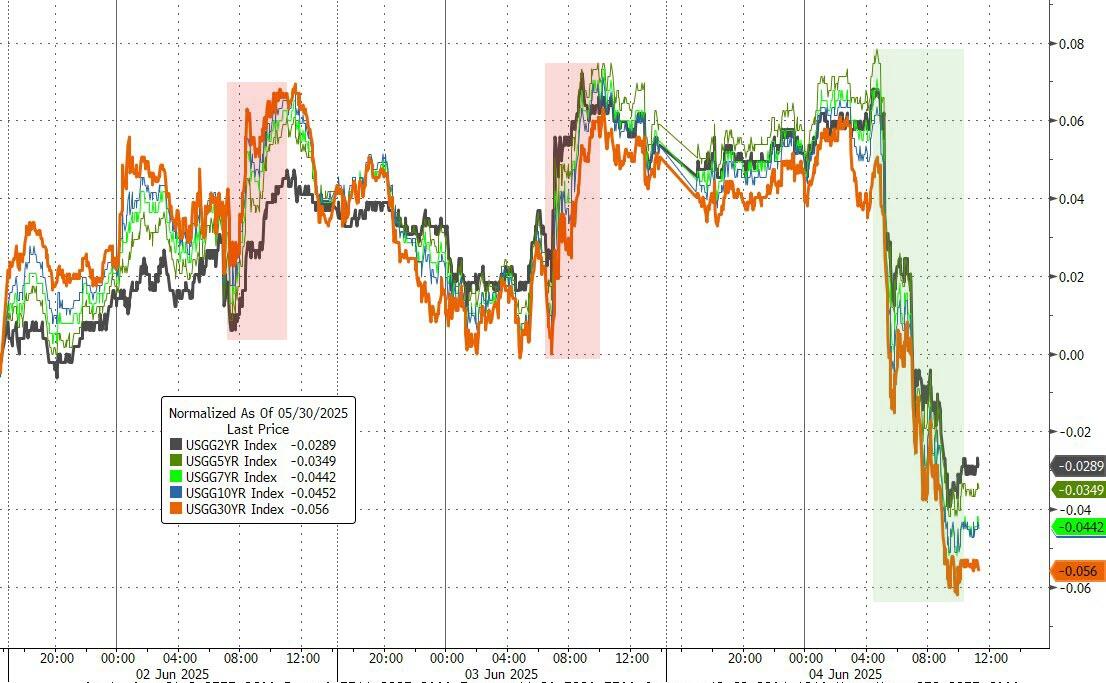

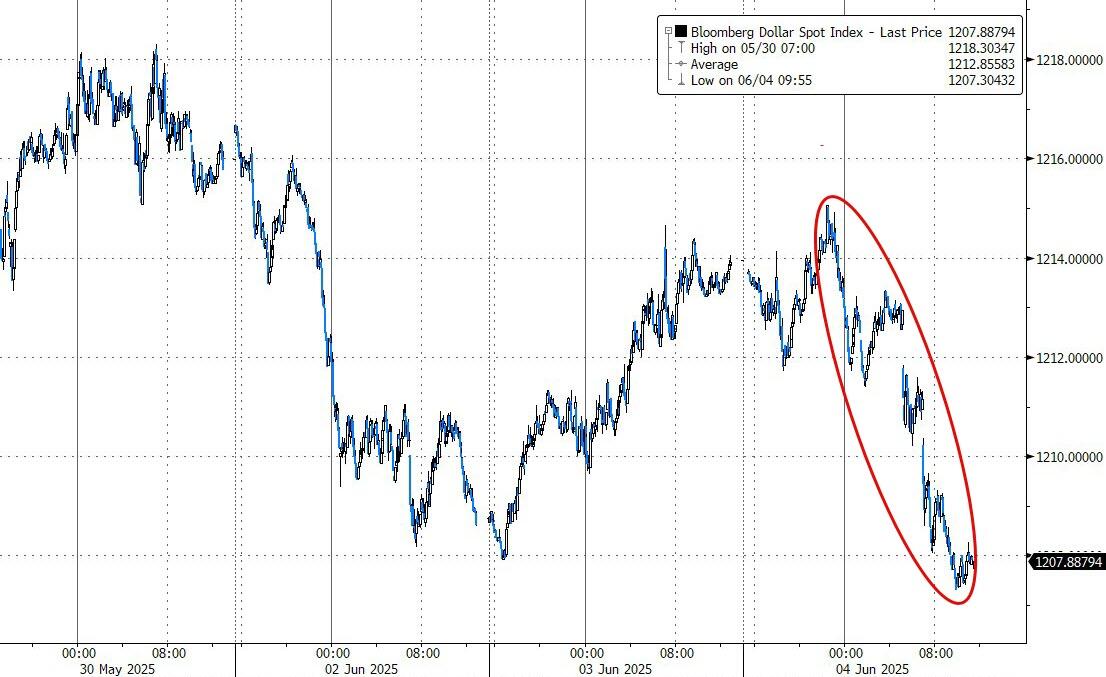

Meanwhile, bond yields plunged—especially the 30-year, which saw one of its biggest one-day drops in a year and a half. The dollar followed suit, hitting new lows not seen since July 2023.

That weakness gave gold a boost, sending it soaring past $3,400 intraday. Bitcoin dipped slightly but found support around $105K.

Now, all eyes are on Friday’s payroll report. Will it confirm a slowdown—or surprise us all?

Continue reading…

2. Current domestic “Buy” Cycle (effective 5/20/2025); International “Buy”Cycle (effective 5/8/25)

Our domestic bullish cycle that began on November 21, 2023, concluded on April 3, 2025, following a market downturn triggered by President Trump’s tariff policy announcement.

This development caused significant declines across major indexes and broader market indices. However, markets subsequently rebounded, culminating in a new domestic “Buy” signal taking effect May 20, 2025.

Concurrently, our International Trend Tracking Index (TTI) experienced parallel volatility. On April 4, 2025, it breached critical thresholds, prompting a “Sell” recommendation. This position reversed as global markets recovered, with the International TTI regaining sufficient momentum to issue a new “Buy” signal effective May 8, 2025.

3. Trend Tracking Indexes (TTIs)

The Dow and S&P 500 lost steam after a promising open and ended the day pretty much flat. The Nasdaq, however, managed to stay in the green, showing a bit of bullish energy.

As for our TTIs, they went in different directions—the international markets showed some improvement, while the domestic side pulled back a bit.

This is how we closed 06/04/2025:

Domestic TTI: +1.10% above its M/A (prior close +1.33%)—Buy signal effective 5/20/25.

International TTI: +6.66% above its M/A (prior close +6.34%)—Buy signal effective 5/8/25.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

———————————————————-

WOULD YOU LIKE TO HAVE YOUR INVESTMENTS PROFESSIONALLY MANAGED?

Do you have the time to follow our investment plans yourself? If you are a busy professional who would like to have his portfolio managed using our methodology, please contact me directly to get more details.

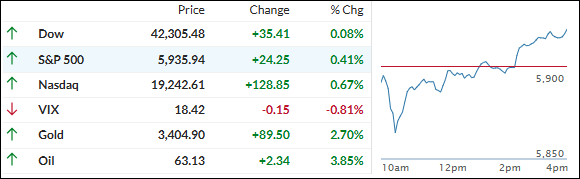

Markets picked up where they left off yesterday, building on modest gains despite a flat start as traders kept a close eye on potential developments in U.S.-China trade talks.**

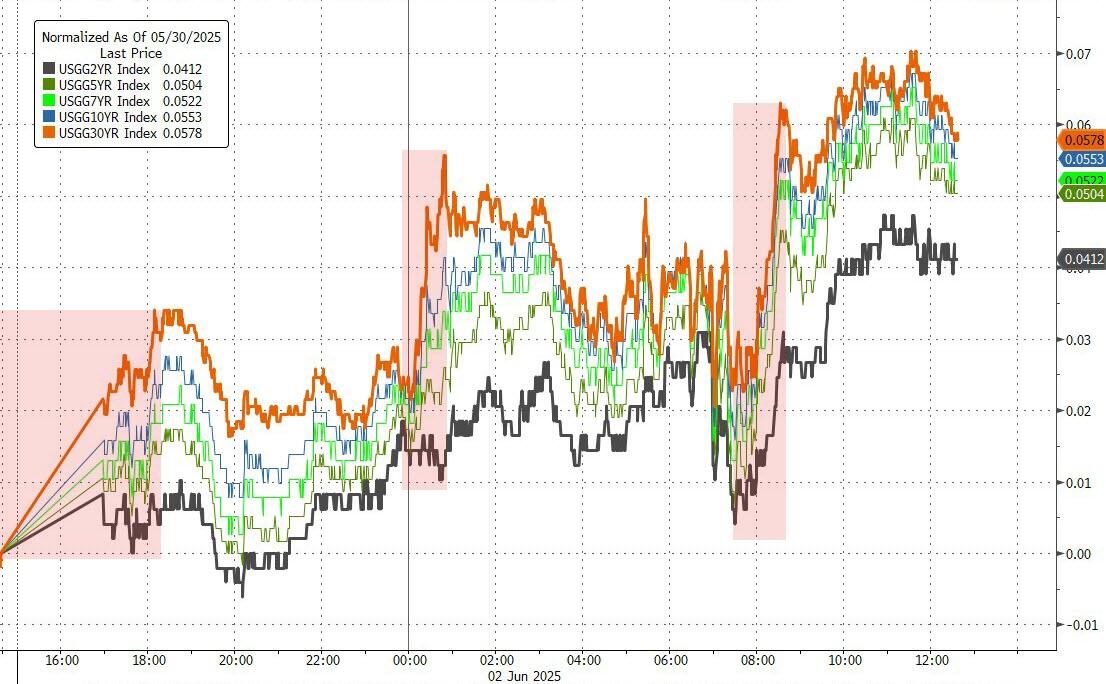

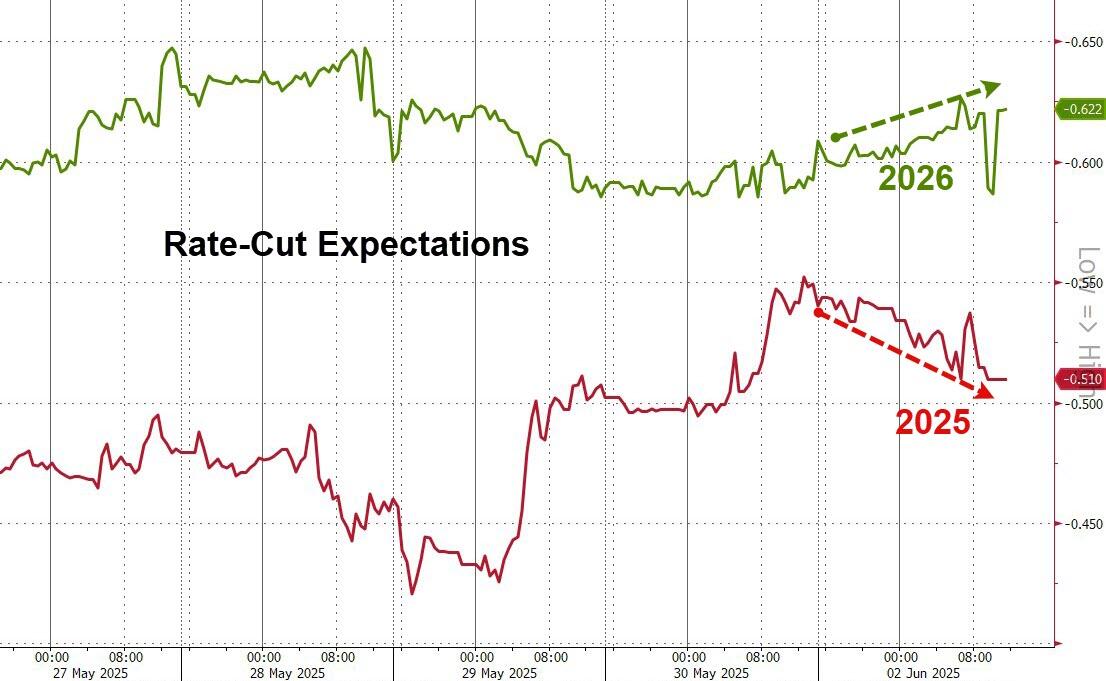

However, not everything was working in the bulls’ favor. The OECD trimmed its U.S. growth forecast to 1.6% from 2.2%, casting a bit of a shadow over the day’s optimism. That news initially pushed bond yields lower, but they later reversed sharply as hopes for rate cuts began to fade.

Trade tensions remained a key theme, with negotiations between the U.S. and China reportedly hitting more turbulence. Still, some analysts remain upbeat about the market’s short-term outlook, pointing to seasonal trends—historically, the next six weeks tend to be among the strongest stretches of the year, rivaling even the fourth quarter.

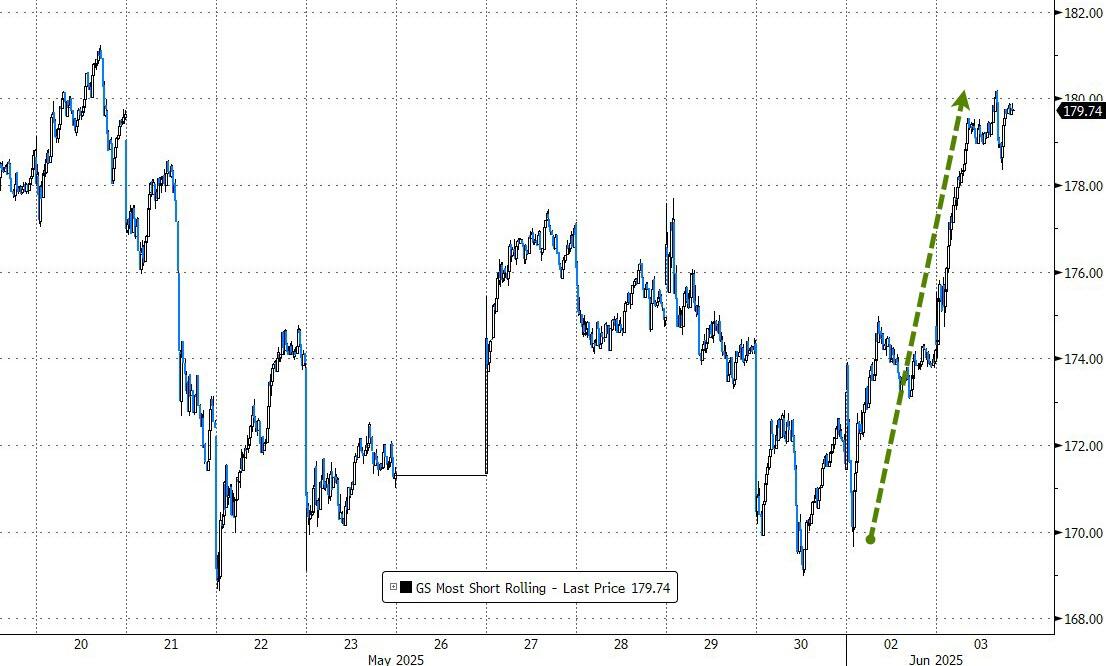

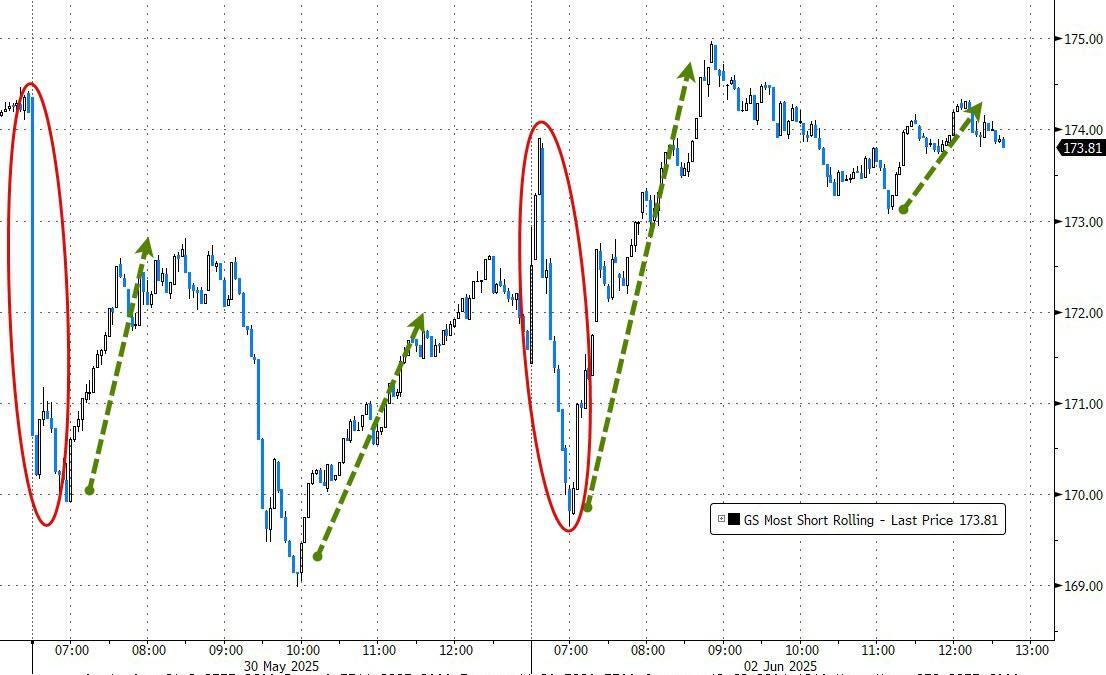

On the data front, the JOLTS report surprised to the upside, showing more job openings than expected. That, along with a boost in retail sentiment, helped fuel a midday rally and triggered a short squeeze that pushed markets even higher.

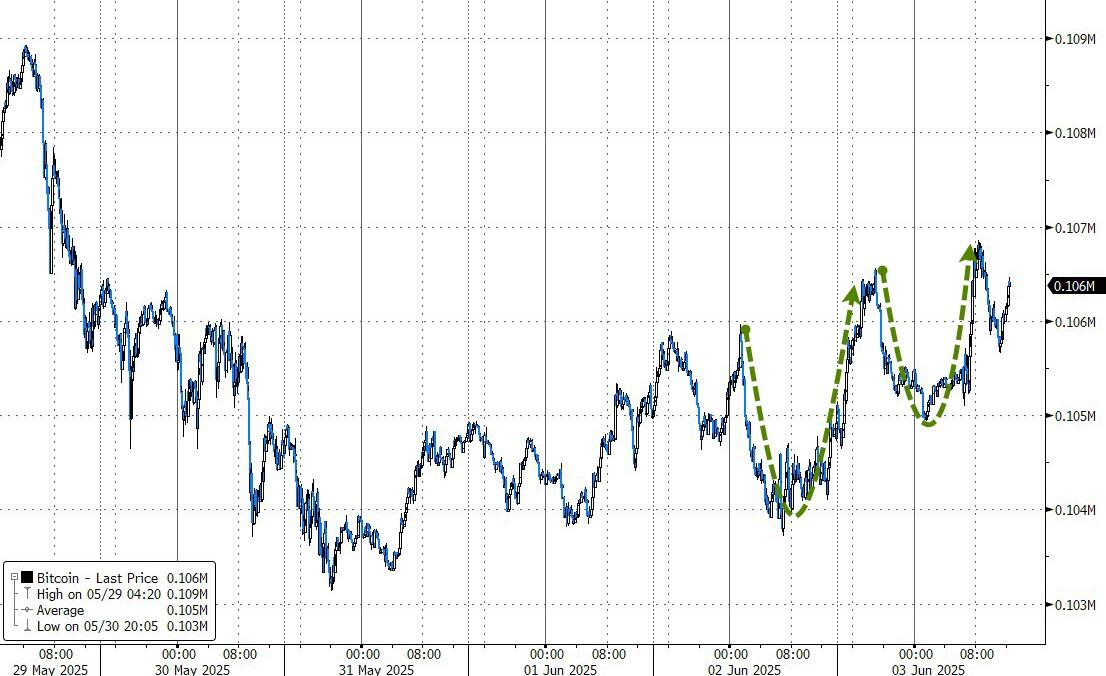

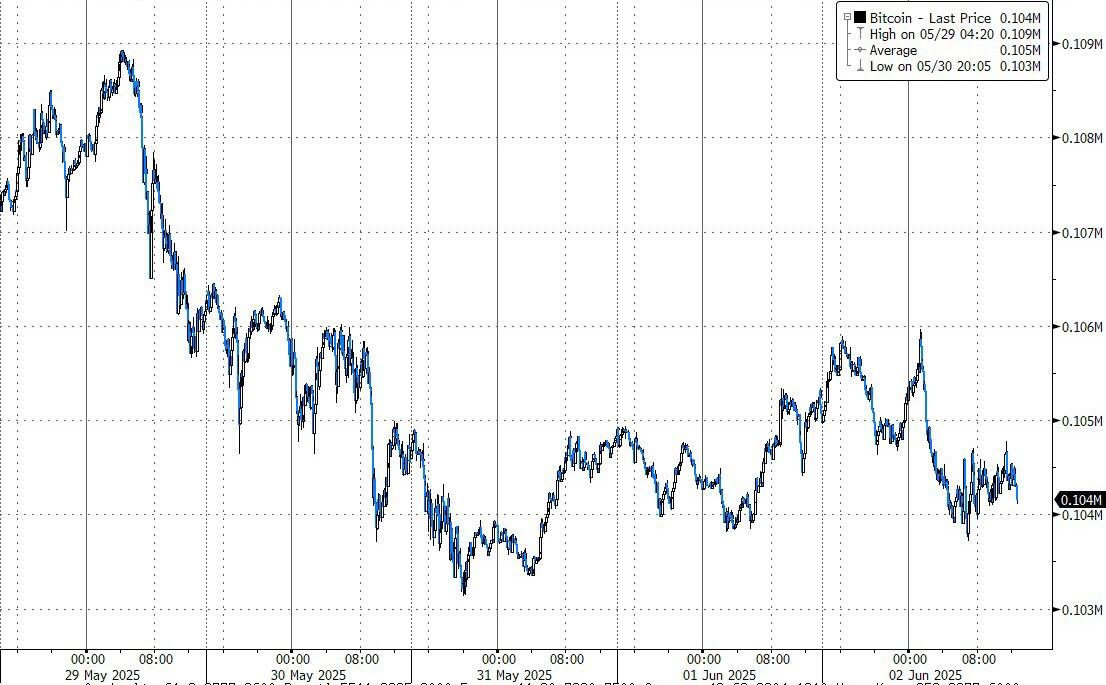

Elsewhere, the dollar rebounded from last week’s lows, putting pressure on gold, which gave back some recent gains. Bitcoin, true to form, continued its rollercoaster ride—up, down, and back up again.

All eyes are now on Friday’s jobs report. With job openings on the rise, the big question is: Will a strong payroll number be good news for stocks—or will it spook investors worried about fewer rate cuts?

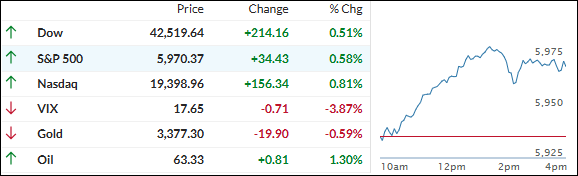

Global trade tensions had markets on edge early in the day, with major indexes slipping into the red right out of the gate.

The pressure came after China pushed back on U.S. claims that it had violated a temporary trade deal—blaming Washington for not holding up its end. The back-and-forth between the two powers made it clear that negotiations are heading in the wrong direction.

Meanwhile, tensions flared between the U.S. and the European Union after Trump announced a plan to double steel tariffs to 50%. The EU warned that this move could inject more uncertainty into the global economy and drive up consumer costs on both sides of the Atlantic.

Despite the rocky start, markets found their footing. A short squeeze kicked in early and helped lift the major indexes into the green by the close.

In the bond market, yields climbed as hopes for a 2025 rate cut faded. The dollar slipped to its lowest level since July 2023.

Gold had a standout day—jumping 2.73% and breaking out of its downtrend channel—while silver surged an impressive 5.3%. Bitcoin stayed rangebound but held support around the $104K mark.

ZeroHedge shared an updated global liquidity chart (with a 3-month lag), hinting that if history repeats, bitcoin could be on a path toward $200K.

So, with all this volatility and momentum, are we looking at the start of a summer breakout—or just another head fake?

Do you want to know which ETFs are hot and which ones are not? Then you need my High-Volume ETF Cutline report. It tells you how close or far each of the 311 ETFs I follow is from its long-term trend line (39-week SMA). These are the ETFs that trade more than $5 million a day, so they are not some obscure funds that nobody cares about.

The report is split into two parts: The winners that are above their trend line (%M/A), and the losers that are below it. The yellow line is the line of shame that separates them. You can see how many ETFs are in each group and how they have changed since the last report (159 vs. 181 current).

STOCKS REBOUND IN MAY, BUT TRADE TENSIONS AND FISCAL FEARS LINGER

[Chart courtesy of MarketWatch.com]

Moving the market

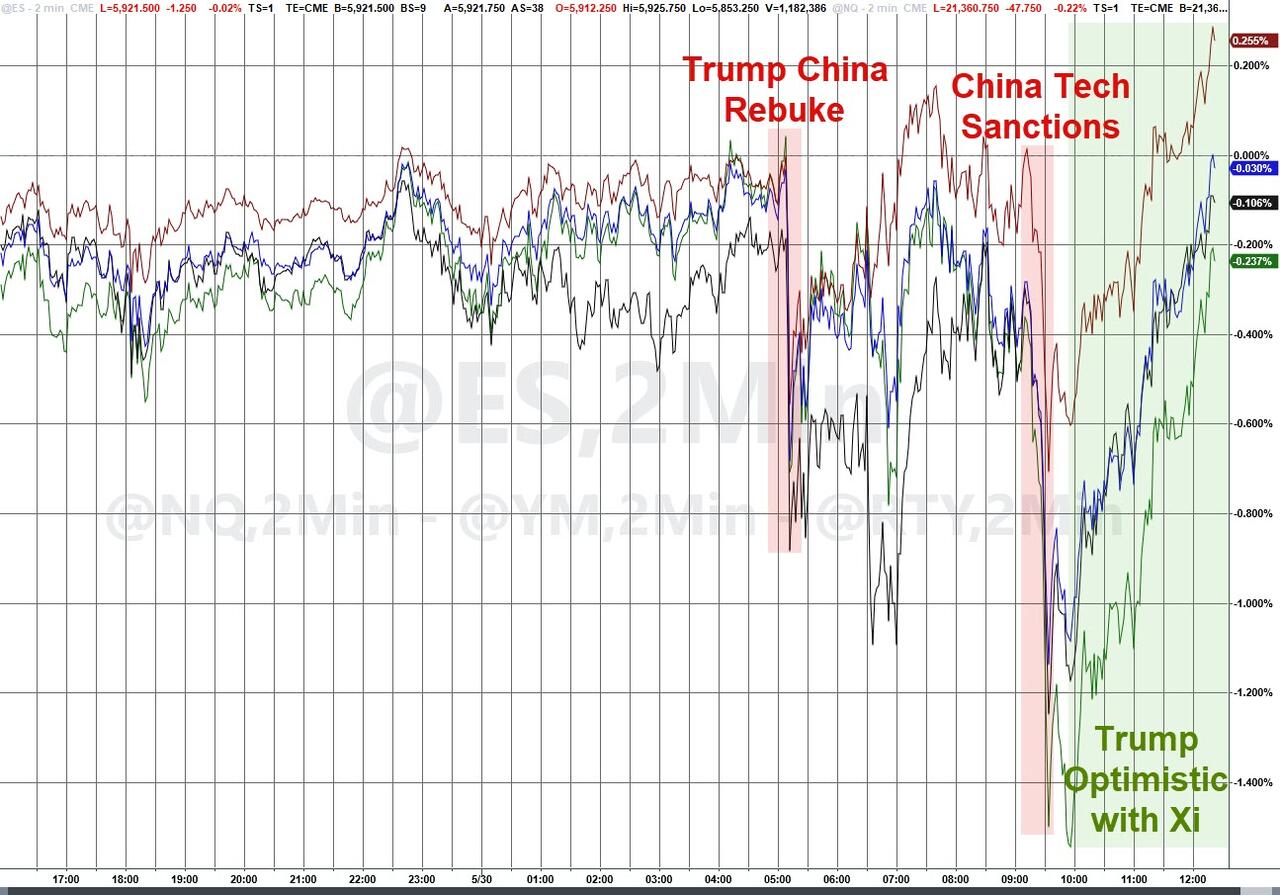

Stocks stumbled out of the gate today after President Trump accused China of breaking its initial trade deal—rekindling fears of a renewed trade war. That headline alone was enough to rattle traders early on.

Adding fuel to the fire was the legal uncertainty surrounding the administration’s aggressive tariff plans.

A court ruling on Wednesday night temporarily blocked most of the tariffs, only for an appeals court to step in Thursday afternoon and keep them alive—at least for now. The back-and-forth has made it tough to see how or when a lasting U.S.-China trade agreement might happen.

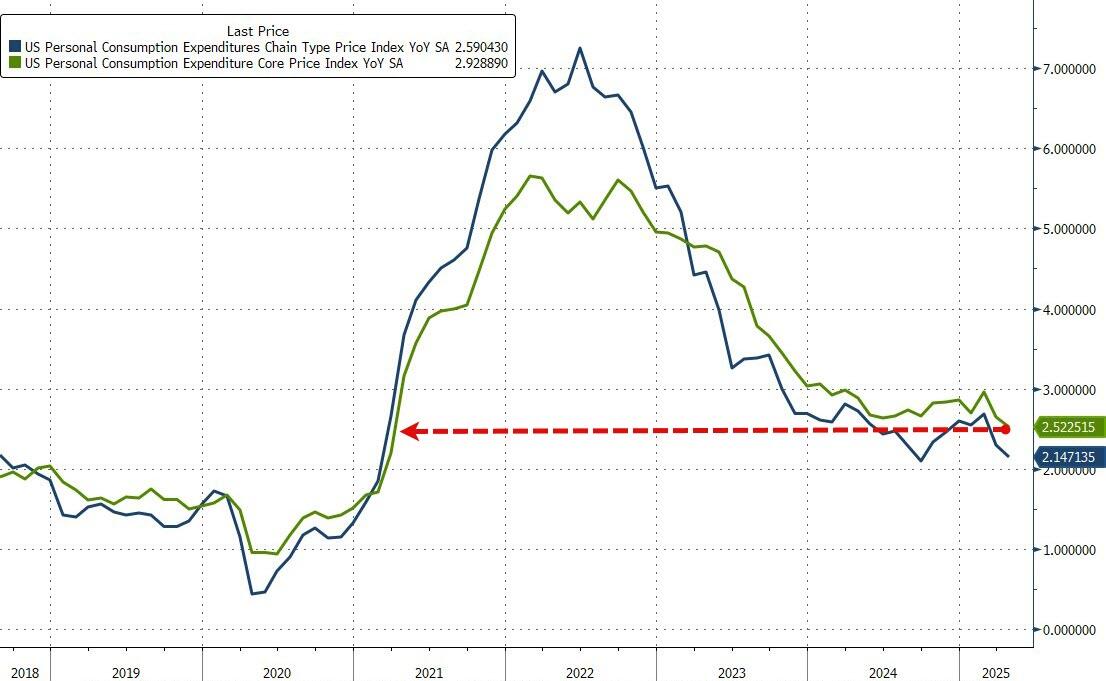

On the bright side, the Fed’s go-to inflation gauge—the PCE—dropped to a four-year low. That could make it harder for Fed Chair Powell to justify holding off on more rate cuts.

Despite today’s turbulence, May turned out to be a strong month for equities. The S&P 500 bounced back with a +6.2% gain, clawing its way into positive territory for the year—barely—at +0.80%. Still, that’s a far cry from gold’s impressive +25% YTD surge.

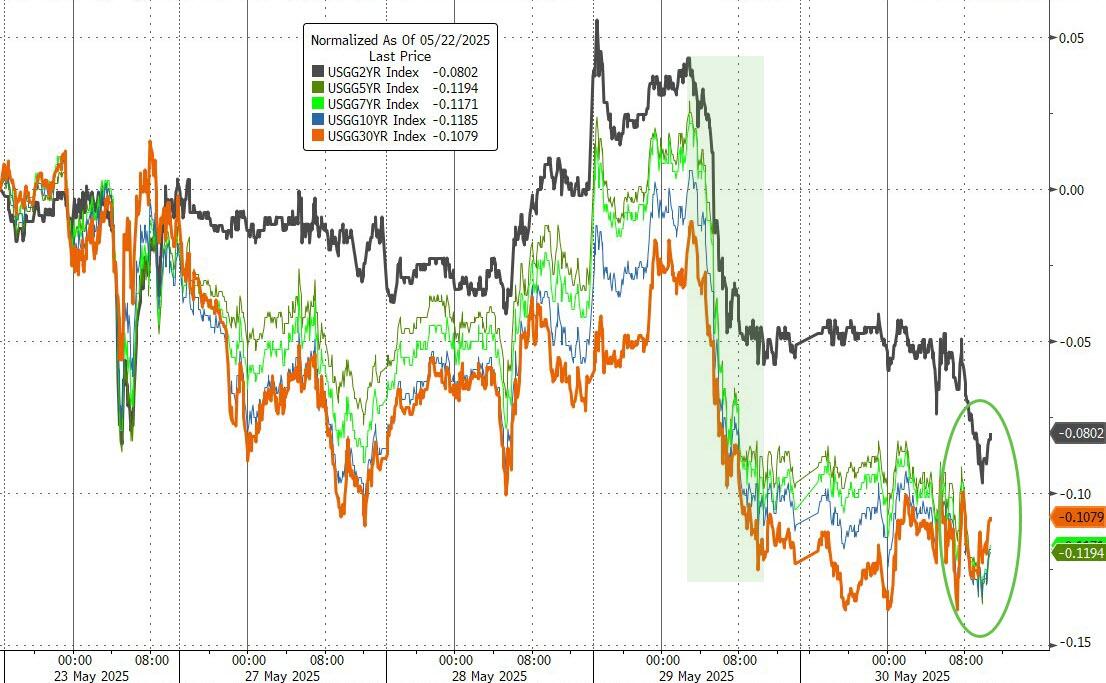

Elsewhere, bond yields dipped for the week but rose for the month. The dollar slid for the fifth month in a row, while gold notched a modest fourth straight monthly gain.

Bitcoin stole the spotlight again, jumping 11% in May and hitting a new all-time high, thanks in part to strong inflows into BTC ETFs.

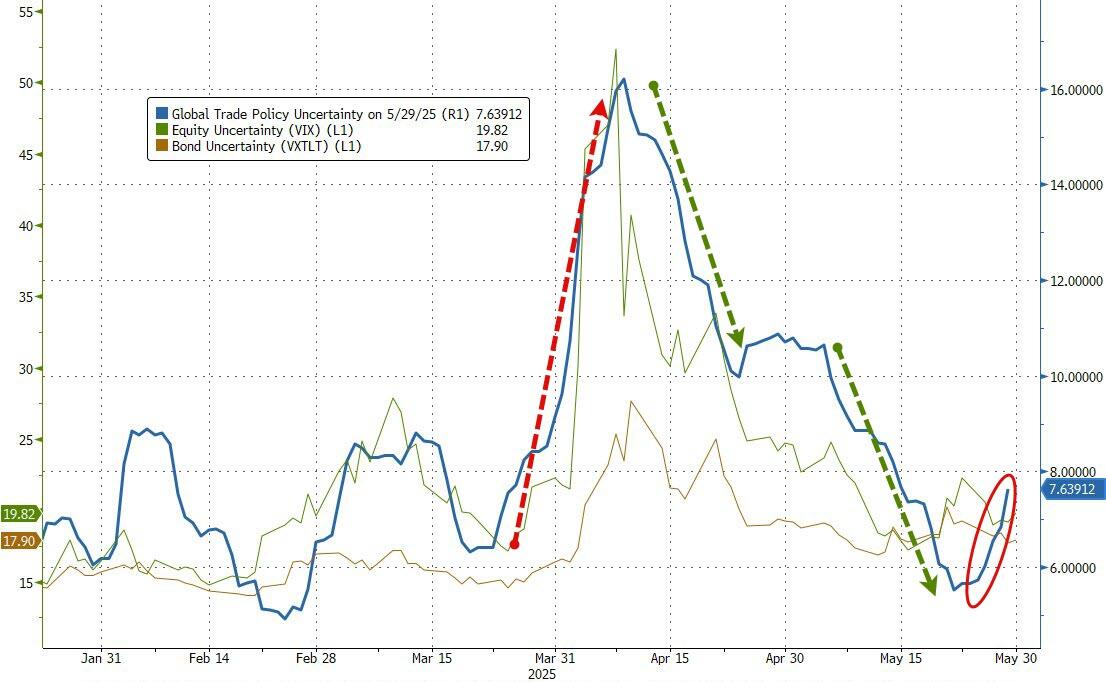

As ZeroHedge noted, even though trade policy uncertainty has eased a bit, concerns about U.S. fiscal stability and default risk are still hanging over the market.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}