- Moving the market

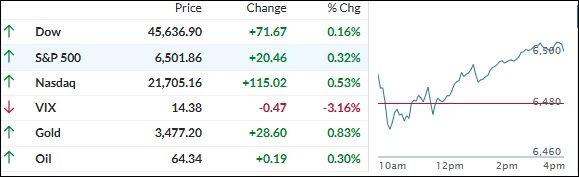

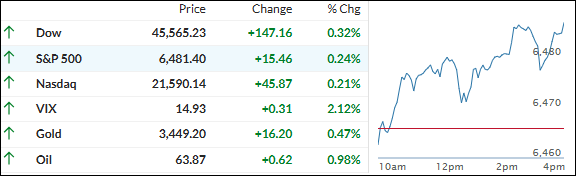

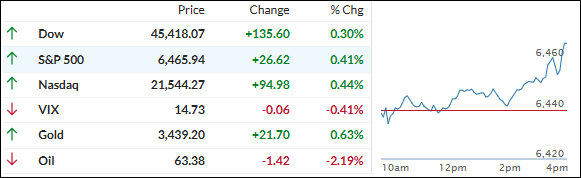

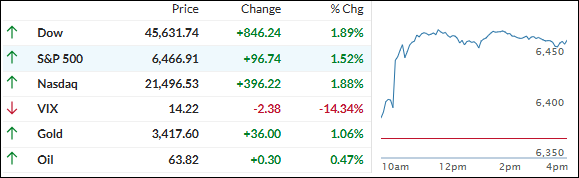

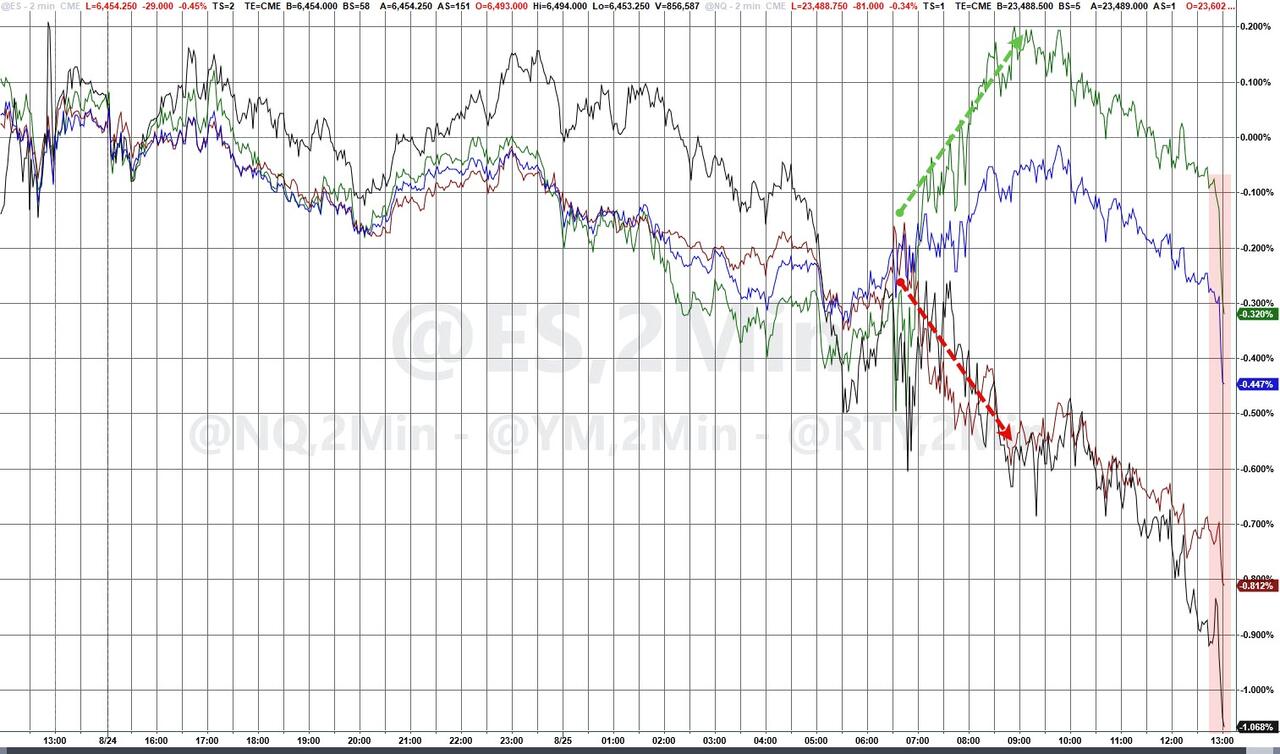

Today’s session reflected a blend of cautious optimism and earnings digestion. The Dow, S&P 500, and Nasdaq all closed at new record highs for the first time in 2025.

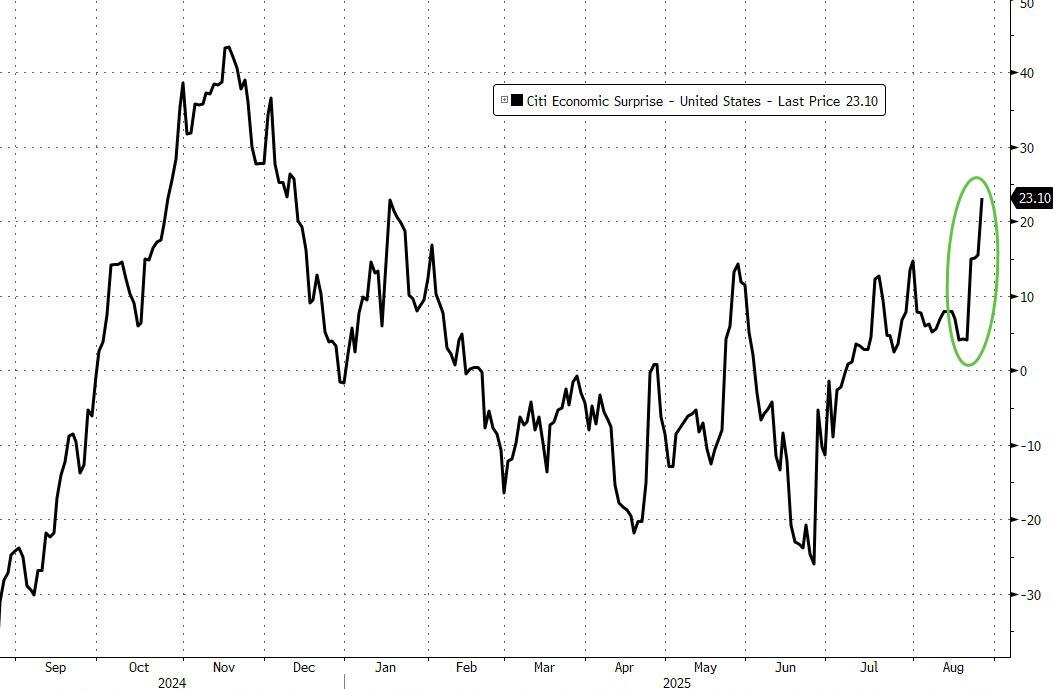

I believe traders spent the day weighing Nvidia’s latest “good but not mind-blowing” earnings and a surprise upward revision to US GDP. Surprisingly, the Russell 2000 outpaced the big indexes, notching a solid gain on renewed interest in small caps.

As for the Fed, odds of a September rate cut remain high—around 88%—and the market seems comfortable with the central bank’s slower, steadier approach. The way I see it, uncertainty about Fed independence is lingering thanks to recent headlines, but it hasn’t provoked much anxiety among stock investors.

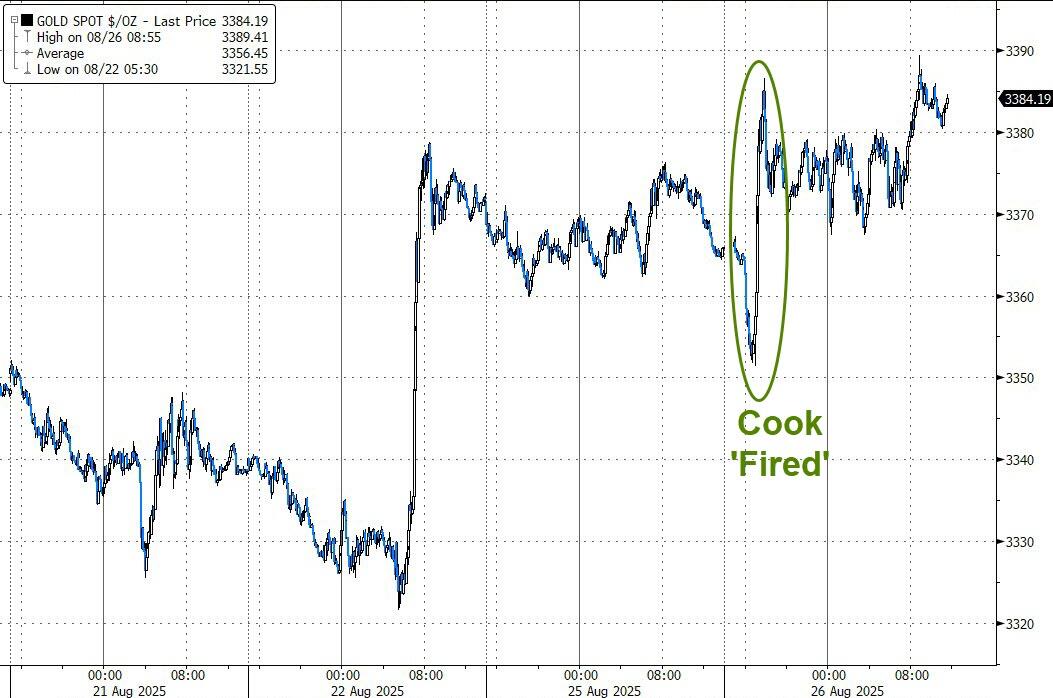

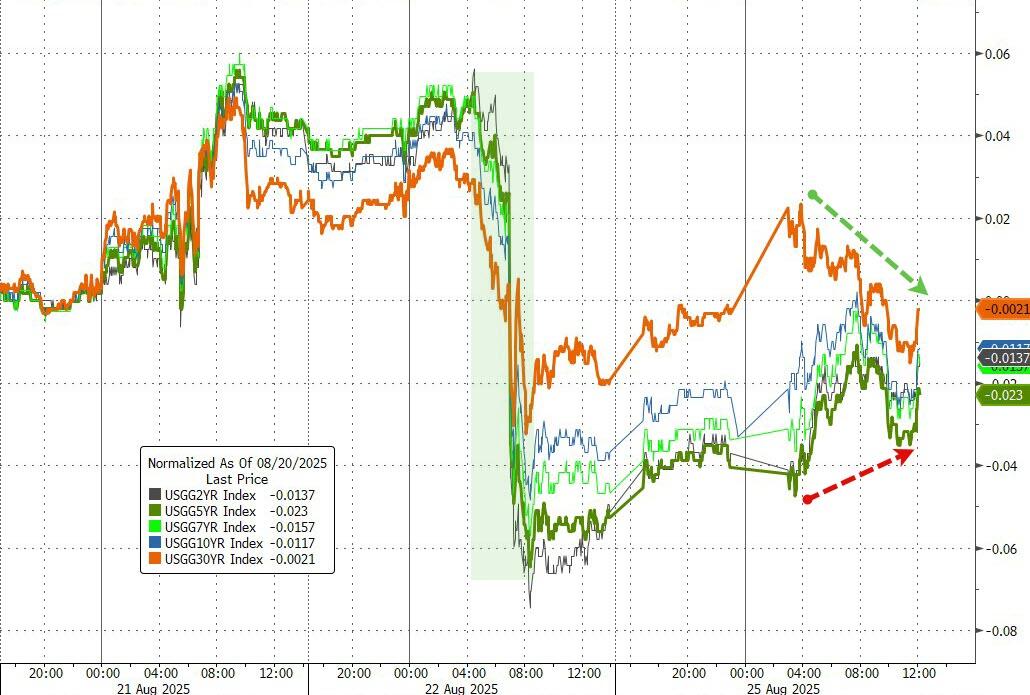

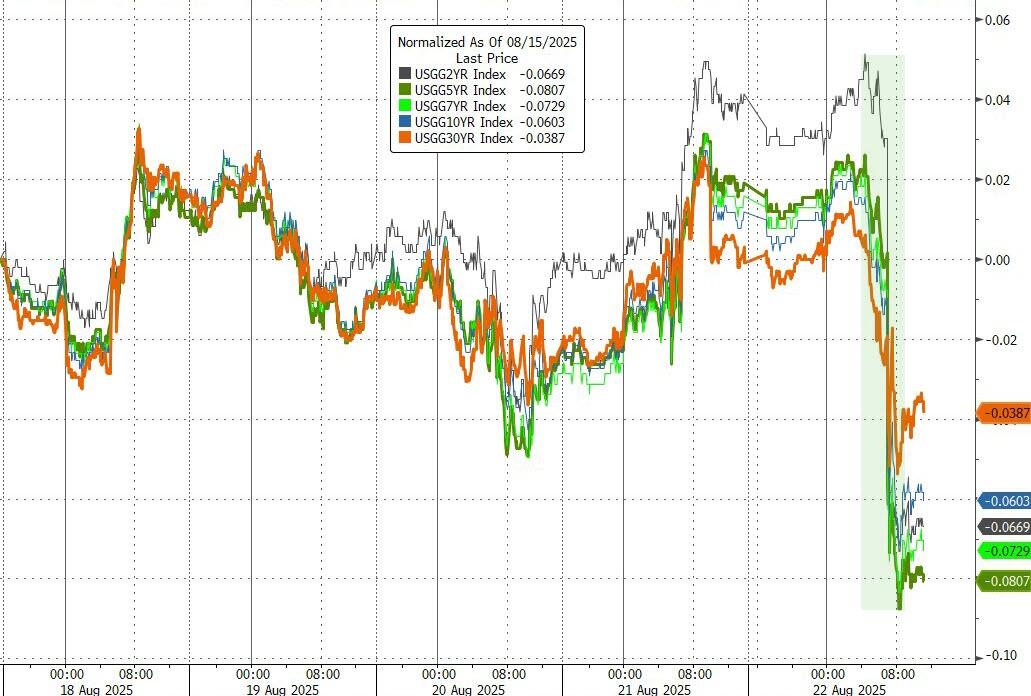

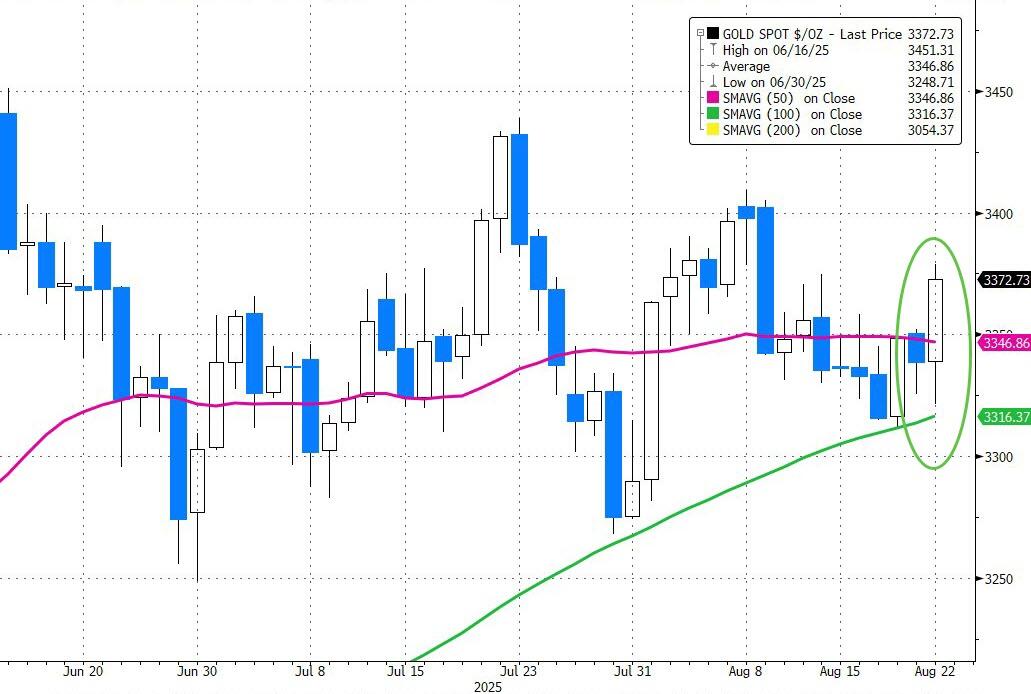

Bond yields barely moved, signaling no major change in rate expectations. The dollar fell, reflecting mild risk-on sentiment. Gold pushed towards its record highs, as some investors grabbed a bit more safety, given the recent political drama and steady Fed outlook.

Mag 7 stocks were mixed: Nvidia slid just a bit after earnings, while Broadcom popped over 1% and others like Microsoft, Apple, Alphabet, Amazon, and Tesla showed slight increases, with Meta bucking the trend and dropping. I think this split shows traders are still sorting winners and losers in the AI and tech trade—no clear leadership, but plenty of action.

On the digital side, bitcoin managed to snap back about 1% after recent weakness, suggesting traders are getting more comfortable with risk again.

With August winding down, I believe the market’s resilience is impressive—but with rates, tech, and politics all swirling, my question is: will this bullish streak hold up as we head into September, or is it just a summer fling?

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}