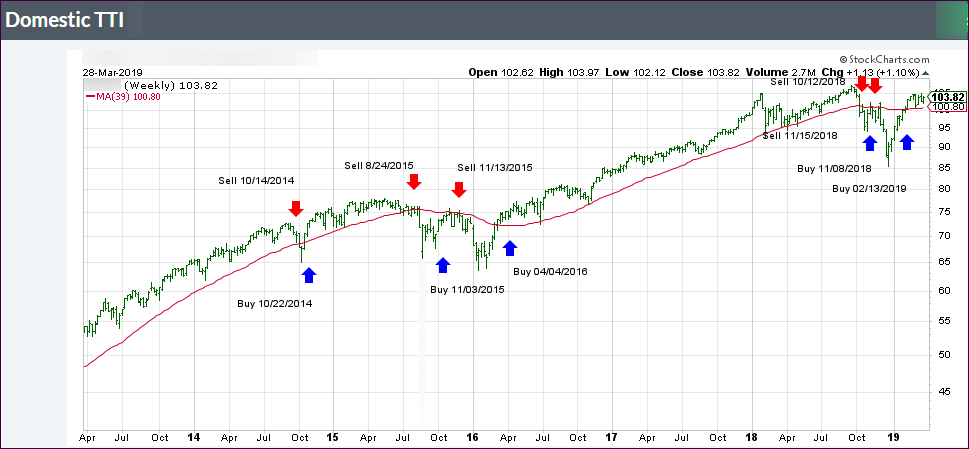

ETF Tracker StatSheet

https://theetfbully.com/2019/03/weekly-statsheet-for-the-etf-tracker-newsletter-updated-through-03-28-2019/

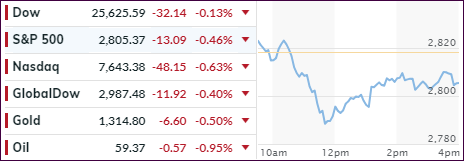

ENDING THE QUARTER ON A POSITIVE NOTE

[Chart courtesy of MarketWatch.com]

- Moving the markets

Continued optimism about more progress with the U.S.-China trade talks moved to front and center thereby pushing concerns over slowing global economies to the sidelines, at least for the time being.

Supporting the early rally was the market debut of Uber competitor LYFT, whose shares ended up trading at a market premium of 20% of what they were priced Thursday evening.

This bullish mood accelerated throughout the day with the major indexes picking up steam and closing at the highs of the day.

While the S&P 500 recorded its strongest quarter in a decade (+13.3%), let’s not forget that this comes after a devastating Q4 2018 performance of -13.5%, during which the Fed suddenly changed course by softening their interest rate policy thereby bailing out the Buy-and-Hold crowd and likely saving investors’ portfolios from far more serious destruction.

Ironically, all this occurred in the face of plunging bond yields and a surge in global money supply, while fundamental data, as represented by the Macro Surprise Index, simply tumbled.

But today, we also heard some positive econ reports during which we learned that consumer confidence rebounded and improved for the second straight month. At the same time, the pummeled real estate sector showed signs of life, as new home sales surged thanks to tumbling mortgage rates.

Earnings season will be on deck starting next week and will likely give us a better view not only if bullish forces are alive and well, but also if the markets have enough starch to weather out disappointments, which are sure to be part of the story line.

Read More

{kind=link}

{kind=link}

{kind=link}