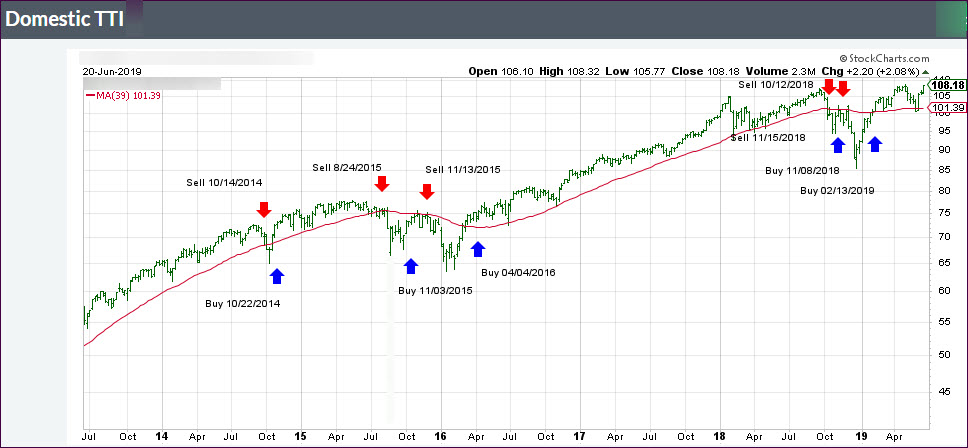

1. Moving the markets

As was to be expected, the major indexes wandered aimlessly slightly above and below their respective unchanged lines with only the Dow being able to eke out a green close.

With no news from the Fed expected, and the G-20 meeting on deck next weekend in Japan, we may seem some more bobbing and weaving and a lackluster view until a new driver appears and drives equities higher.

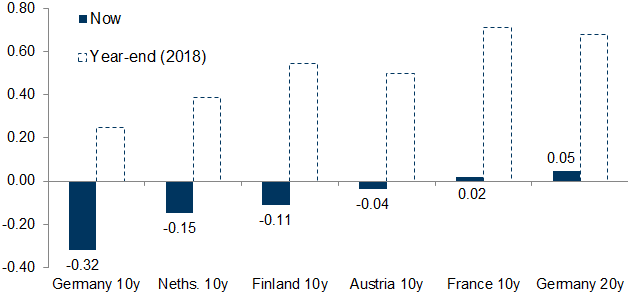

Trump and his Chinese counterpart Xi are set to meet on Friday and Saturday with traders worldwide looking for signs of a truce, as global markets are struggling with lack of growth prospects. These already have impacted various economies negatively, even those that are considered economic export powerhouses like Germany. Their forecasted GDP is down to an anemic 0.6%.

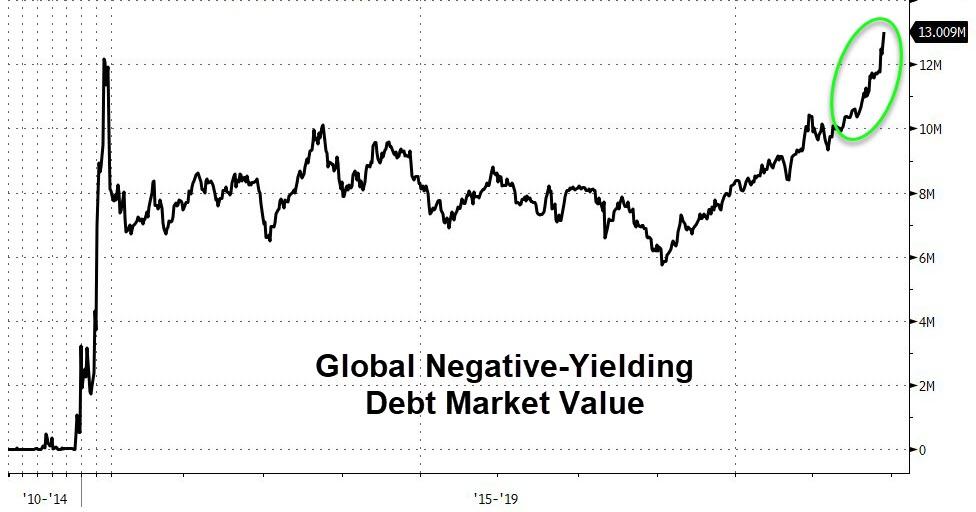

Even worldwide negative bond yields have not done much to stem the southerly tide in economic activity, while here in the US, the White House is trying to push the Fed to implement lower rates.

Why? The state of the current economy is so poor, that only continued stimulus will be able to keep things moving and assist in keeping equities at elevated levels. We saw what happened in 2018 when stimulus was dropped, and the markets crashed.

My view is confirmed by the latest data showing that the Dallas Fed Manufacturing survey collapsed from -5.3 to -12.1, while the Activity Outlook, aka ‘hope,’ has plunged into negative numbers.

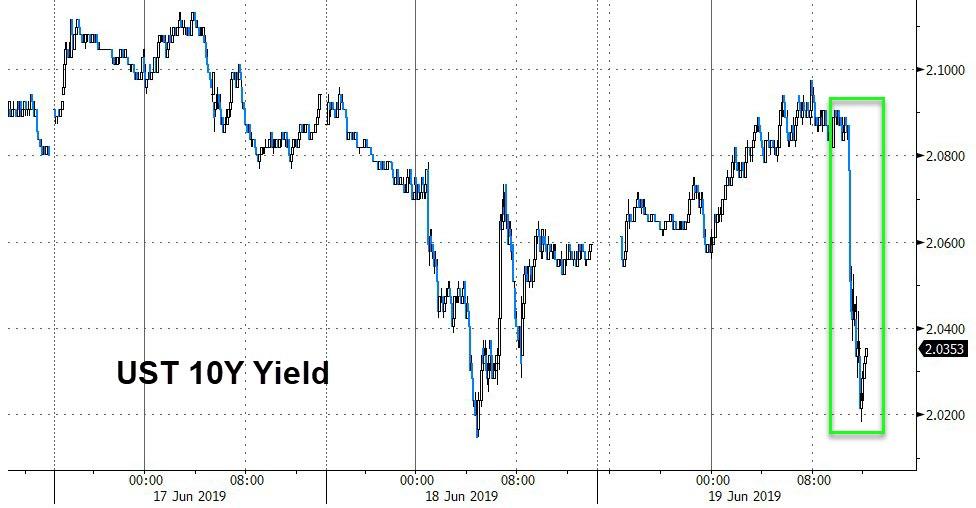

In other words, things are continuing to slow down, which makes me wonder what the justification for these elevated stock prices is. But, as I said before ‘bonds’ represent the smart money, and their crashing yields are indicative of what’s coming. Equities have simply not priced in any bad news on earnings and the economy.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}