Softness in the markets prevailed for the third day, as a

bunch trade news volleys made their way back and forth and kept the major indexes

in limbo. An early drop shifted into rebound mode, an occurrence we’ve seen

regularly in the recent past, but it fell short of conquering the unchanged

lines.

Even though we closed slightly in the red, the continued resilience

of the market, to shake off bad news and remain at ridiculously elevated levels,

is remarkable. The see-saw moves over the past few days continued with utter abundance,

with the market moving headlines being clearly recognizable in this

chart.

With a record “trade deal on/trade off” reversals being the

new norm, it now included “unnamed sources” saying that “the US would be

willing to delay the December 15 tariffs, even if there is no trade deal,” but

that the pro-Hong Kong human rights bill passed by Congress could be a major

obstacle to any agreements.

Despite equity weakness, bond yields rose, which hurt

bond prices and low volatility ETFs the most. The odds

of a US-China trade deal plunged, which means, if those don’t reverse, a new

driver will be needed to keep stocks on their northerly path.

The markets started the session by meandering slightly below

their respective unchanged lines when a sudden dive took the starch out of any

existing support. As I posted yesterday, a new headline about how close the latest

trade deal might be was sure to be on deck.

Well, we got trade headlines, but they revealed exactly the

opposite of what was expected, namely that phase one of this much jawboned about

event may not be completed this year. To stoke the fire of discontent even

more, China condemned a US Senate resolution supporting human rights in Hong

Kong.

Then it was the US’s turn to emphasize that “rolling back

tariffs for a deal that fails to address core intellectual property and

technology transfer issues will not be seen as good deal for the US.” That

was the final nail in the coffin to seal the downward

trend of equities.

But the mocking continued, as the editor of China’s Global

Times, after his earlier threat that “China wants a deal but is prepared for

the worst-case scenario, a prolonged trade war,” proceeded to taunt the US farmers with “wait

for a trade deal before getting bigger tractors.” You just can’t make this

up, and it makes me wonder how long this soap opera will go on.

Despite all this negativity, a late day rebound lifted the

indexes off their lows but fell short of moving them into the green. Nevertheless,

the markets are showing tremendous resilience, especially when you consider

that the Dow has been down 2 days in a row for its biggest drop in 6 weeks, and

this very drop amounted to less than 1%.

The S&P 500 has not had 1% correction in 28 days and,

as ZH points out, it went 36 days in June/July without one. Of course, as I have

pointed out on many occasion, the main driver that controls market direction is

global liquidity, which this

chart (Source: Bloomberg) clearly demonstrates.

Today we experienced a market condition, which we have

not seen in a while, namely not just an intra-day sell off, but also a red

close of more than the occasional shocking -0.01%, at least for the Dow. Of

course, I am being facetious here, but the usual end of the day ramp saved the

S&P 500 and Nasdaq.

However, given the relentless march higher, today’s partial

retreat was more than overdue. A slightly positive opening gave way to a gentle

slide into the red zone, but the bullish theme remained strong enough to assist

in the recovery.

Not helping matters were disappointing earnings results

and the good old standby excuse that a US-China deal has become questionable.

Home Depot’s shares took

a hit with the company not just posting a miss in Q3 sales,

but more importantly, they slashed their full-year sales guidance as well. Ouch!

However, offsetting that poor report was a rise in US home building and permits

for future construction.

Clearly, the economy, despite being hyped up, is mixed

bag at best. Even the Fed’s John Williams seems to agree as he posted things

like “the economy is clearly facing several challenges, primarily from

overseas, but the three rate cuts since July should help sustain growth,” on

which he elaborated further with the US “facing headwinds from slower global

growth.”

In the end, nothing much was gained or lost, except the

Nasdaq remained on the plus side all day and added +0.24%. At least the tech arena

showed signs of life in the face of a sinking retail

sector, where the stocks of Home Depot and Kohls were sent reeling.

With no obvious driver to help the markets today, I imagine

that we will see a new rollout of “the trade deal is close” headlines

latest by tomorrow, in order to pump stocks further into record territory.

When the Fed announced a few weeks ago that it would be

buying up Treasury debt to the tune of $60 billion a month, it sure sounded to

everyone on Wall Street that another round of QE (Quantitative Easing) had

started. However, Fed chief Powell insisted that this is “in no sense is QE.”

Yeah right.

Author Charles

Hugh Smith wasn’t in agreement either and quoted in a recent post a

riddle that Abraham Lincoln was known to have told: “If I should call a

sheep’s tail a leg, how many legs would it have? — Five! — “No, only four; for

my calling the tail a leg would not make it so.”

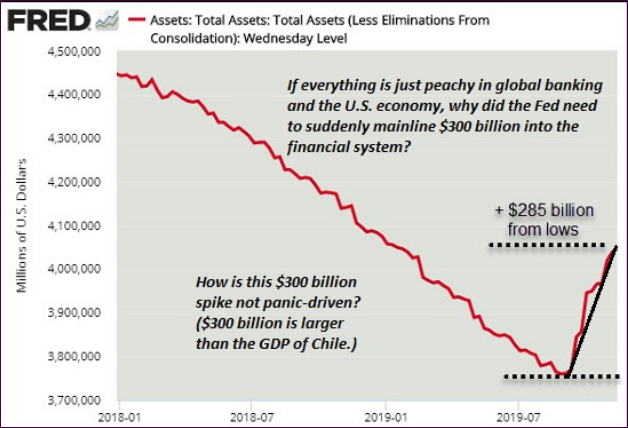

That is a great analogy to the Fed’s QE implantation

which, despite all denials, is a bailout of some sort, most likely of the repo

market, about which I have commented on from time to time. And, as this

chart depicts, it may have been a panic reaction, and I am certain

that this will not be the last we’ve heard about repo issues.

While the major indexes see-sawed throughout the day, the

bullish bias remained intact with the Dow and Nasdaq eking out tiny gains, but the

S&P slipped a fraction. These small moves were actual significant in that the

usual driver, namely US-China trade news, was neutralized.

There were announcements about “progress” and “setbacks,”

cancelling each other out, which is what market direction reflected. Over the weekend,

we learned that top negotiators held “constructive” discussions, but other

reports suggested that without rolling back existing tariffs, the outlook for a

resolution looked questionable.

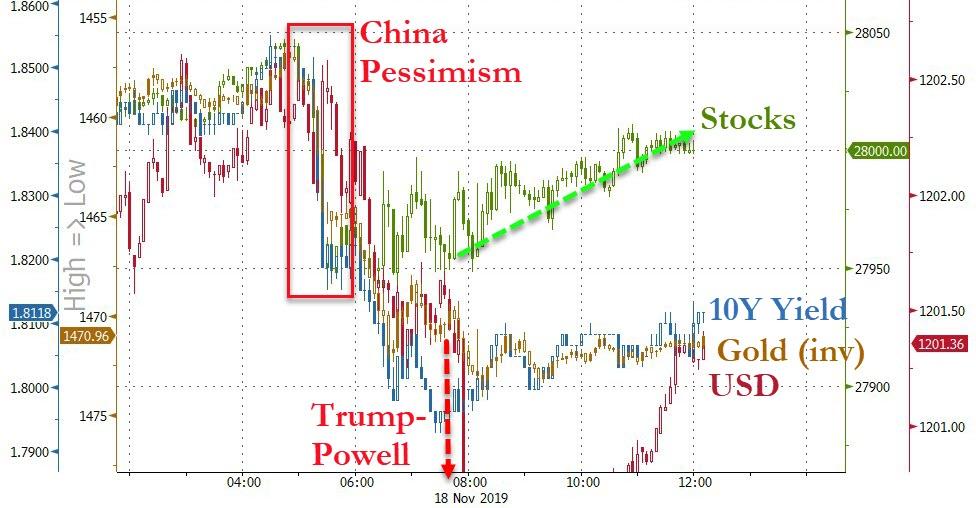

With trade news playing an immaterial role in the market today,

traders focused on a meeting between Trump

and Powell, with speculation running wild as to what these two discussed. Trump

released this statement:

Just finished a very good & cordial

meeting at the White House with Jay Powell of the Federal Reserve. Everything

was discussed including interest rates, negative interest, low inflation,

easing, Dollar strength & its effect on manufacturing, trade with China,

E.U. & others, etc.

I am sure that by tomorrow morning, the computer algos

may have found some more bullish meat on that bone, probably just enough to keep

the ramp going. If that doesn’t work, there is always another short

squeeze to be done, just like we saw today, which gave a big assist in pulling

the indexes off their lows. (Source: Bloomberg)

Below, please find the latest High-Volume ETF Cutline

report, which shows how far above or below their respective long-term trend

lines (39-week SMA) my currently tracked ETFs are positioned.

This report covers the HV ETF Master List from Thursday’s

StatSheet and includes 322 High Volume ETFs, defined as those with an average

daily volume of more than $5 million, of which currently 281 (last week 282)

are hovering in bullish territory. The yellow line separates those ETFs that

are positioned above their trend line (%M/A) from those that have dropped below

it.

In case you are not familiar

with some of the terminology used in the reports, please read the Glossary of Terms.

If you missed the original

post about the Cutline approach, you can read it here.

DRIVING

THE MARKETS: TRADE HOPE AND RETAIL HEADLINE

[Chart courtesy of MarketWatch.com]

Moving the markets

While

today’s headline retail number showed a rise of +0.3% MoM, which was better than

the expected +0.2%, the under the hood core number looked mixed at best by only

rising +0.1% MoM vs. an expected +0.3%. But headline news are what computer algos

read, so up we went.

The

initial boost came from alleged positive US-China trade war developments,

with the White House econ advisor Kudlow saying Thursday night that “negotiators

are getting close to an agreement,” however, Trump added that “he likes

what he sees, he’s not ready to make a commitment, we have no agreement just

yet.”

In

other words, there is no deal, only promises and possibilities, but that’s all

it takes these days to keep traders and algos happy, a condition which pushed the

major indexes into new all-time territory.

Even

poor economic news good not stem the march higher. US MoM Industrial Production

plunged

the most since March 2009, as October’s -0.8% collapse led to a YoY

decline of -1.13%. In addition, Manufacturing

output fell -0.6%, its weakest reading since December 2015 (Source: ZeroHedge).

I

am merely pointing this out to clarify that the stock market and the underlying

economy are in no way connected, and that a high level of stock prices does not

indicate a solid economic environment.

This

is further confirmed by the fact that the GDP for Q4 2019 has crashed with the US

economy growing at its slowest pace in 4 years, as the Fed’s tracking estimates

having tumbled by over 0.4% just the past week. The US GDP in Q4 2019 is now set

to print at around 0.35%, which is anemic and in no way justifies the current

level of stock indexes.

But

that is not what matters. What is critically important for the continuation of

the bullish ramp, as I pointed out before, is the liquidity in the market, which

has been created by an increase in the Fed’s balance

sheet. It grew by some $280 billion in the past two months alone and is directly

responsible for driving equities relentlessly higher.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}