ETF Tracker StatSheet

You can view the latest version here.

CRASHING INTO THE WEEKEND

- Moving the markets

Despite an early bounce along the green side of the unchanged line, reality set in, supported by the always unpredictable quad options expirations day, sending the markets reeling—again.

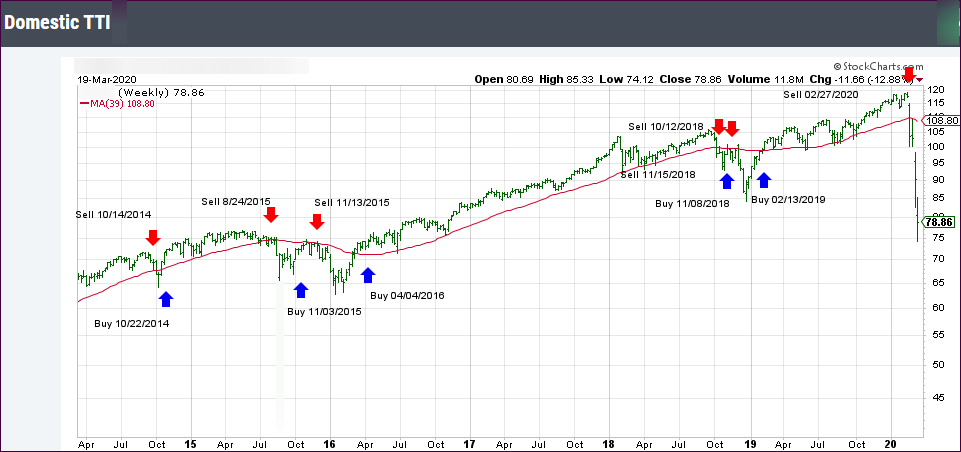

The major indexes were hammered, with the S&P 500 getting skunked by -15%—for the week! Not helping matters late in the day was the fact that a death-cross in the Dow had occurred, meaning its 50-day moving average had dropped below its 200-day M/A, which can be a sign of more weakness ahead.

Of course, some clueless analysts were quick to point out that the last death cross appeared three days before the Christmas Eve 2018 bottom. So, what difference does that make? All the gains from that point forward have now been given back and then some, which is a clear representation of the buy-and-hold idiocy.

ZH points to the fact that today was a historic one. The Fed bought a record $107 billion in securities today alone, as its balance sheet exploded some 50% in the last six months. It becomes clearer by the day that the Fed’s scramble to stabilize the Treasury market is not working.

As I said before, there is some big player (to be named later), like a bank or Hedge fund, that got caught on the wrong side of a severely leveraged trade and needs to be bailed out. Hence the monetization of various securities, including now the Muni bond market. Something appears to be broken beyond repair, and I am sure we will find out soon what it is.

ZH added more color:

This was the worst week since Lehman (and worst 4 weeks since Nov 1929) for The Dow Jones Industrial Average…(Dow was down 18% during the Lehman week and 17.35% this week), despite The Fed gushing a stunning $307 billion into the markets – almost double its previous biggest liquidity injection (in March 2009)…

And here’s Bloomberg’s updated chart showing where we might be going, and that is towards the 1,700 level on the S&P 500. And longer term, we may even see history repeat itself.

In the meantime, enjoy the popcorn while watching this movie from the sidelines.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}