Below, please find the latest High-Volume ETF Cutline

report, which shows how far above or below their respective long-term trend

lines (39-week SMA) my currently tracked ETFs are positioned.

This report covers the HV ETF Master List from Thursday’s

StatSheet and includes 322 High Volume ETFs, defined as those with an average

daily volume of more than $5 million, of which currently 31 (last week 91) are

hovering in bullish territory. The yellow line separates those ETFs that are

positioned above their trend line (%M/A) from those that have dropped below it.

In case you are not familiar

with some of the terminology used in the reports, please read the Glossary of Terms.

If you missed the original

post about the Cutline approach, you can read it here.

The

markets finally managed to keep a rebound

rally going after yesterday’s collapse. As I posted, during bear markets, you can

witness violent upswings, but they don’t mean the bearish trend is over.

Today,

we started in the green, as news from Europe that the German FinMin unleashed

their version of a financial bazooka and presented their “whatever it takes moment:”

SCHOLZ SAYS POSSIBLE

GERMANY WILL NEED TO TAKE ON ADDED DEBT;

GERMANY WILL HAVE NO

LIMIT ON CREDIT PROGRAM FOR COMPANIES;

SCHOLZ SAYS GERMANY

WILL SPEND BILLIONS TO CUSHION ECONOMY;

GERMANY PLANS TO SET

UP SAFETY NET FOR VIRUS-HIT COMPANIES;

ALTMAIER: RESOURCES

FOR GERMANY’S STATE BANK TO RISE TO 500BN

That

set the bullish tone for the day, and up we went. Adding hope for a quick response

domestically were reports that House Speaker Pelosi and the Trump

Administration were nearing an agreement on an aid package, to include sick pay

free virus testing and other resources.

Then

it was the Fed’s turn to announce their “whatever it takes moment,” by attempting

to restore some liquidity in the broken overnight lending market by concluding three

of six emergency POMOs (Permanent Open Market Operations) and soaking up billions

of Treasuries of varying maturities.

Towards

session end, it was Trump’s stimulus/testing plan that spiked equities to their

biggest gain since October 2008, thereby somewhat offsetting the market’s worst

week since 2008, during which the S&P 500 dropped -8.8%.

Even

diversification did not help, as this week was the worst weekly loss for a

diversified portfolio of stocks and bonds since 2008 with -14.69%, as Bloomberg

points out in this

chart.

Next

week, the Fed will meet, and the markets are “demanding” a full 1% interest rate

cut with Bloomberg providing the graphic representation.

You can be pretty much assured that the Fed will cave and comply, otherwise the

current debacle will continue in an accelerated fashion.

1. From the universe of over 1,800 ETFs, I have selected only those with a

trading volume of over $5 million per day (HV ETFs), so that liquidity and a

small bid/ask spread are assured.

2. Trend Tracking Indexes (TTIs)

Buy or Sell decisions for Domestic and International ETFs (section 1 and

2), are made based on the respective TTI and its position either above or below

its long-term M/A (Moving Average). A crossing of the trend line from below

accompanied by some staying power above constitutes a “Buy” signal. Conversely,

a clear break below the line constitutes a “Sell” signal. Additionally, I use a

7.5% trailing stop loss on all positions in these categories to control

downside risk.

3. All other investment arenas do not have a TTI and should be traded

based on the position of the individual

ETF relative to its own respective trend line (%M/A). That’s why those signals

are referred to as a “Selective Buy.” In other words, if an ETF crosses its own

trendline to the upside, a “Buy” signal is generated. Since these areas tend to

be more volatile, I recommend a wider trailing sell stop of 7.5% -10% depending

on your risk tolerance.

If you are unfamiliar with some of the terminology, please see Glossary of Termsand new subscriber information in section 9.

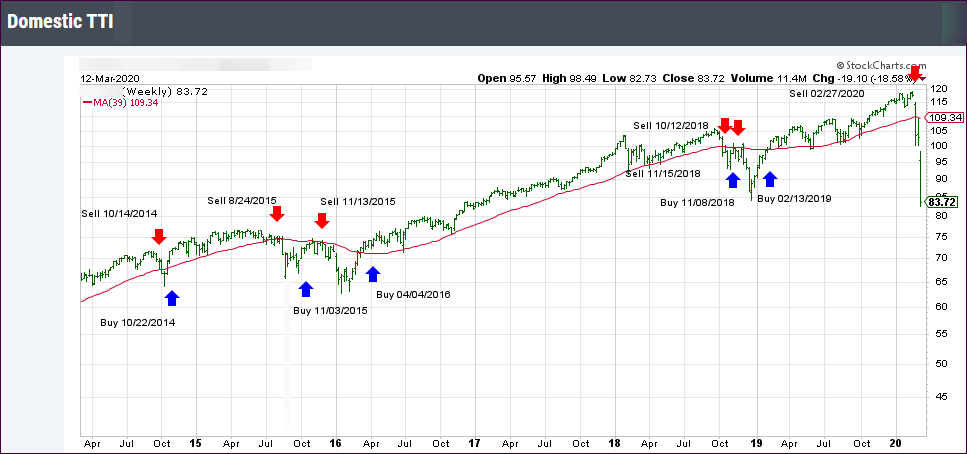

1. DOMESTIC EQUITY ETFs: SELL

— since 02/27/2020

Click on chart to enlarge

Our main directional indicator, the Domestic Trend Tracking Index (TTI-green line in the above chart) is now positioned below its long-term trend line (red) by -23.80% after having generated a new Domestic “Sell” signal effective 2/27/20 as posted.

In a few decades, historians will look back at the past 10

years and shake their heads in disbelieve at the insane Fed monetary policies

that have kept markets artificially propped up, while “disallowing” any downside

moves beyond a certain “acceptable” percentage.

Though many erroneously attribute the current market

disaster to the coronavirus, that is incorrect. The virus was merely the pin

that pricked the ever-growing bubbles, which would have burst anyway, but we

might have pushed the can down the road a little longer.

ZH and others posted these relevant commentaries:

This bull market will go down in history as the one that nobody believed would last this long. A lot of people have been hurt because their retirement money disappeared…. What brought us to where we are in 2020 is too much hope, sky-high valuations.

Did I see it coming this far? No. Throughout the past 11 years, the market has had a lot of dips, and always the Federal Reserve came to the rescue…. Right now, the Fed is not enough, central bank action is not enough. There is a pyramid of uncertainty right now.

Does the Fed really want to have a put every time the market gets nervous? …Coming off all-time highs, does it make sense for The Fed to bail the markets out every single time… creating a trap?

The Fed has created this dependency and there’s an entire generation of money-managers who … have only seen a one-way street… of course they’re nervous.

The question is – do you want to feed that hunger? Keep applying that opioid of cheap and abundant money?

The market is dependent on Fed largesse… and we made it that way…

At this moment, the crash fest goes on with utter abandon causing one analyst to ask:

“Is the market now like an “Oriental Rug Factory” where “Everything Must Go?”

It certainly

feels that way now, as many leveraged traders are forced to unwind and sell everything,

including safe-haven assets like precious metals, in order to meet margin

calls.

Of course,

in bear markets we can witness and sharp rebounds of great magnitude, but that

does not mean a new bull market is imminent. Case in point was today, when the

Fed fired a bazooka

by unleashing a $1.5 trillion Rep bailout, which means up to $3 trillion in cumulative

repos by the end of the month.

The effect was immediate, as the above chart shows, with the

Dow regaining some 1,500 points within minutes. Unfortunately, this was merely

a dead cat bounce, and the markets resumed their downward trajectory with utter

abandon leaving me pondering as to whether the Fed has finally run out of

ammunition.

However, I expect them to drop rates to zero, or below, and

directly intervene in the markets, just like the Japanese Central Bank does, by

openly buying stocks, bonds and ETFs. We will find out soon.

Yes, the thing that may have been unthinkable 3 weeks ago

is upon us. The bear market has arrived with full force and may be hanging around

for a while.

Being out of the market and on the sidelines never felt

so right.

With the benefit of hindsight, yesterday’s hope-based

snap-back rally has now assumed the smell of a dead-cat bounce, with the major indexes

getting hammered, as the Dow touched the commonly recognized bear market territory,

which is a 20% drop from recent highs.

A few headlines combined to eradicate any remaining bullish

sentiment:

Core CPI jumps the highest in 12 years with

services costs soaring

The WHO finally declares the coronavirus a Pandemic

Mnuchin says that broad economic response will

have to wait

Globally, the urge to “do something” accelerated with the

Bank of England delivering an emergency 0.25% interest rate cut while pledging

more fiscal stimulus. Germany’s Merkel promised to do “whatever is necessary,”

while at the same time the ECB President warned of an economic shock like the

2008 financial crisis.

Sure, markets are pricing in an easing of Central Banks,

but the question remains how much firepower is really left, after having been

in easing mode for the past 10 years.

In the meantime, the non-reported crisis in the overnight

repo lending market continues unabated with the Fed having to increase the liquidity

bailout to a stunning $175

billion per day, and the market still keeps collapsing (hat tip to ZH/Bloomberg

for this data). Something is seriously broken, which the Financial

Conditions Index clearly shows.

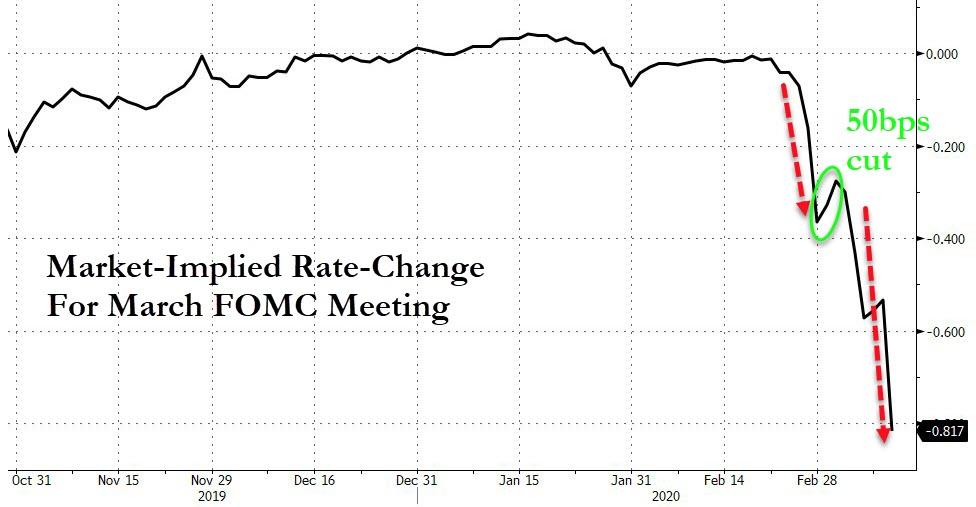

With the Fed summit next week, the implied rate-change

for the March FOMC meeting is about 82 basis point, as Bloomberg’s chart

demonstrates. That means interest rates are heading to the zero level.

And here’s something I have been commenting on over the years,

namely that during times of extreme market stress, such as we are witnessing

right now, the bond portion in a portfolio will not be able to “save” the equity

portion.

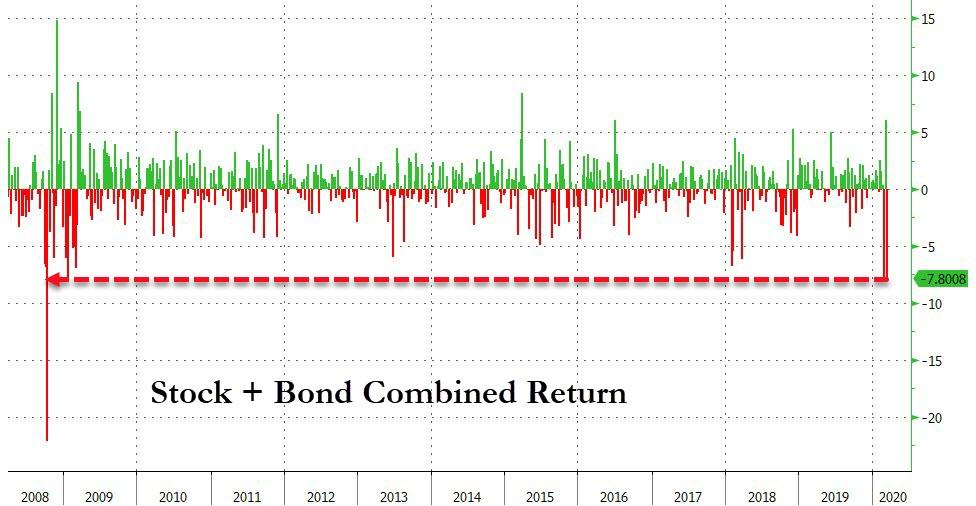

Bloomberg’s

chart shows that the weekly stock and bond combined return was the worst in

11 years (-7.80%), or more specifically since Leman went bankrupt. That supports

my belief that only 100% cash on the sidelines will prevent serious portfolio

damage.

Another wild roller-coaster day in the markets had the

Dow up 900 points early on, after which it tanked and dipped into negative territory

but then went on to rebound and reached new highs for the day, after a last

hour pump, as this

chart demonstrates.

Not that any current issues were resolved but hope for a

fiscal response to the coronavirus scare lifted overall spirits with an assist by

Trump’s proposal for a payroll tax cut.

Historically, today’s rebound is not unusual, as Bespoke Investment

Group strategists found that in the 10 previous times since 1952, that the

S&P 500 fell 5% or more on a Monday, the index has gained the following day

by an average of 4.2%.

While that is noteworthy, it does not imply that the bear

market is over, and all is well again. As officialdom scrambles to come up with

solutions, Trump’s overture to seek payroll tax relief and other measure to

help businesses deal with the virus problem, may be a step in the right direction

and had at least a momentary calming effect on the markets.

Right now, to me this is nothing more than a one-day

bounce, and we will need a lot more to see this move as sustainable and leading

to a new bull run. Technically speaking, the damage lingers with all major indexes

remaining below their 200-day averages.

Fundamentally speaking, the Dow has a long way to catch

down to earnings, as Bloomberg posted here.

While bond yields managed to surge back to the breakeven

point of last Friday’s close, with the 10-year gaining 22 basis points to close

at 0.792%, the untold story lies in the overnight lending market, where the financial

plumbing continues to break and the funding freeze is getting worse.

As I posted before, this is a very complex subject, so

suffice it to say that dealers demanded a record $216 billion in liquidity from

the Fed repo—for one day! ZH summed it up like this:

As we pointed out last week, this continuing

liquidity crunch is not only bizarre, but increasingly concerning, as it means

that not only did the rate cut not unlock additional funding, it actually made

the problem worse, and now banks and dealers are telegraphing that they need

not only more repo buffer but likely an expansion of QE… which will come soon

enough, once the Fed funds hits 0% in a few days and is forced to restart bond

buying to prevent the next crash.

If these issues are not resolved, the next disaster is

bound to start in the bond market, and if it does, it will certainly affect the

equity markets in a big way to the downside.

This is not the time to be a hero by engaging in the fine

art of bottom fishing.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}