[Chart courtesy of MarketWatch.com]

- Moving the market

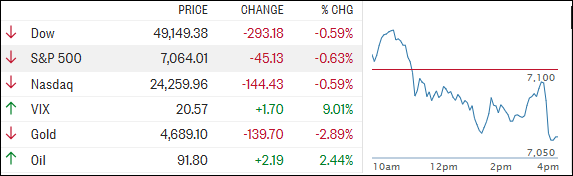

A positive start to the day fizzled out quickly, with the major indexes sliding into the red as traders waited for fresh developments out of the Middle East. With the current ceasefire set to expire on Wednesday, uncertainty once again took center stage.

President Trump told CNBC that he expects the U.S. and Iran to reach a “great deal,” but he also made it clear that the U.S. military is ready to act if no agreement is signed before the deadline — and that he has no intention of extending the ceasefire. That tougher tone followed an earlier Truth Social post in which Trump claimed Iran had “violated the ceasefire numerous times.”

Despite the headlines, Wall Street appears to be slowly looking past the immediate conflict.

What really matters to markets is the normalization of shipping through the Strait of Hormuz, and on that front, it feels like we’re getting closer. There was a brief pickup in commercial vessel traffic over the weekend, although that momentum stalled again after several reported attacks on ships.

By the close, the major indexes couldn’t recover and finished solidly in the red. Anxiety around the ceasefire deadline weighed on nearly every sector, with “value” stocks being the lone area showing some resilience. Even an early short squeeze failed to stick, leaving small caps as the day’s clear underperformers.

{kind=link}

Economic data offered some bright spots. Retail sales surprised to the upside, core sales came in strong, and pending home sales jumped sharply in March. Still, the macro news struggled to offset geopolitical concerns.

Bond yields moved higher, pushing the dollar up as well — a tough combination for gold, which slipped below the $4,800 level and tested the $4,700 area. Bitcoin faded too but held up better than the metals overall.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

With uncertainty in the Middle East still elevated — and the risk of no truce looming — the odds of another equity drawdown remain uncomfortably high, while hopes for a sustained rally continue to fade.

The question now is: what will it take to shift sentiment decisively back to the upside?

2. Current domestic “Buy” Cycle (effective 5/20/2025); International “Buy” Cycle (effective 5/8/25)

Our domestic bullish cycle that began on November 21, 2023, concluded on April 3, 2025, following a market downturn triggered by President Trump’s tariff policy announcement.

This development caused significant declines across major indexes and broader market indices. However, markets subsequently rebounded, culminating in a new domestic “Buy” signal taking effect May 20, 2025.

Concurrently, our International Trend Tracking Index (TTI) experienced parallel volatility. On April 4, 2025, it breached critical thresholds, prompting a “Sell” recommendation. This position reversed as global markets recovered, with the International TTI regaining sufficient momentum to issue a new “Buy” signal effective May 8, 2025.

3. Trend Tracking Indexes (TTIs)

Early bullish enthusiasm faded almost as quickly as it appeared, as the latest headlines offered little reason for equities to keep pushing higher.

That sour mood spilled over into the metals complex, and even Bitcoin wasn’t able to swim against the current.

Our TTIs pulled back as well, but importantly, they remain firmly on the bullish side of their respective trend lines — suggesting this looks more like a pause than a breakdown.

This is how we closed 04/21/2026:

Domestic TTI: +6.01% above its M/A (prior close +6.67%)—Buy signal effective 5/20/25.

International TTI: +7.75% above its M/A (prior close +8.51%)—Buy signal effective 5/8/25.

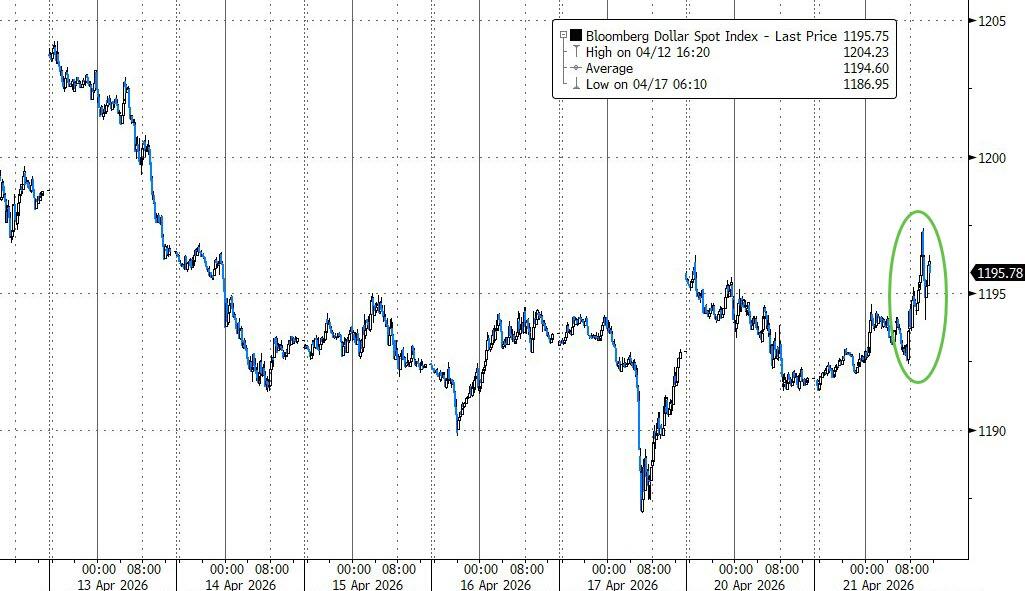

All linked charts above are courtesy of Bloomberg via ZeroHedge.

———————————————————-

WOULD YOU LIKE TO HAVE YOUR INVESTMENTS PROFESSIONALLY MANAGED?

Do you have the time to follow our investment plans yourself? If you are a busy professional who would like to have his portfolio managed using our methodology, please contact me directly to get more details.

Contact Ulli