ETF Tracker StatSheet

You can view the latest version here.

MARKETS RALLY ON HORRIFIC ECONOMIC DATA

- Moving the markets

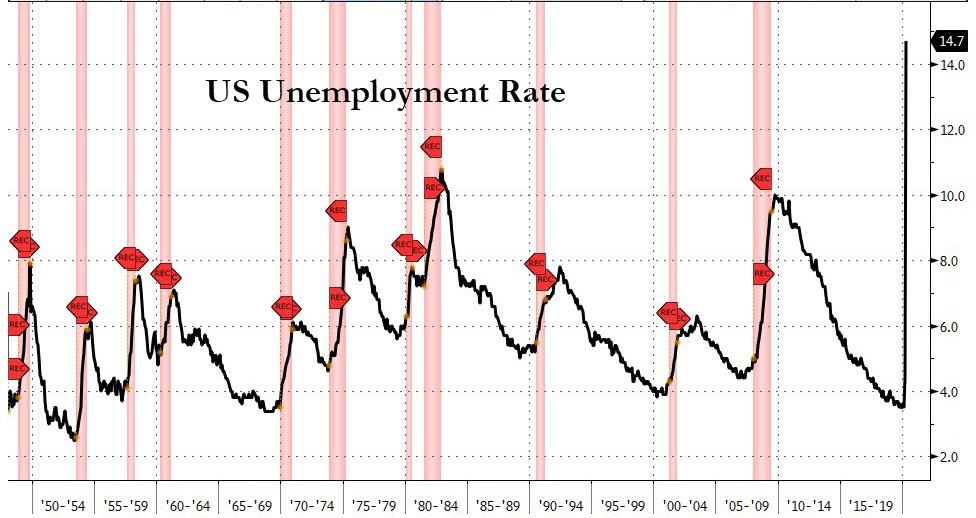

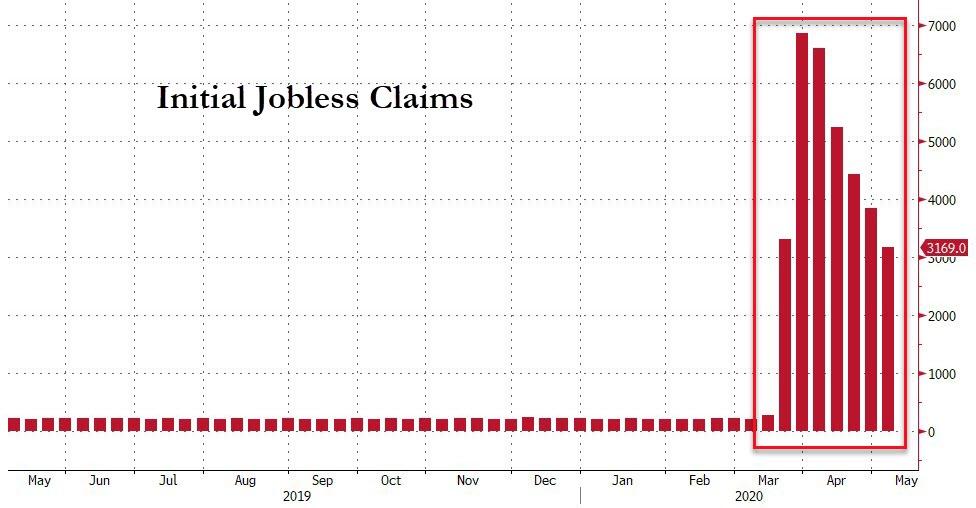

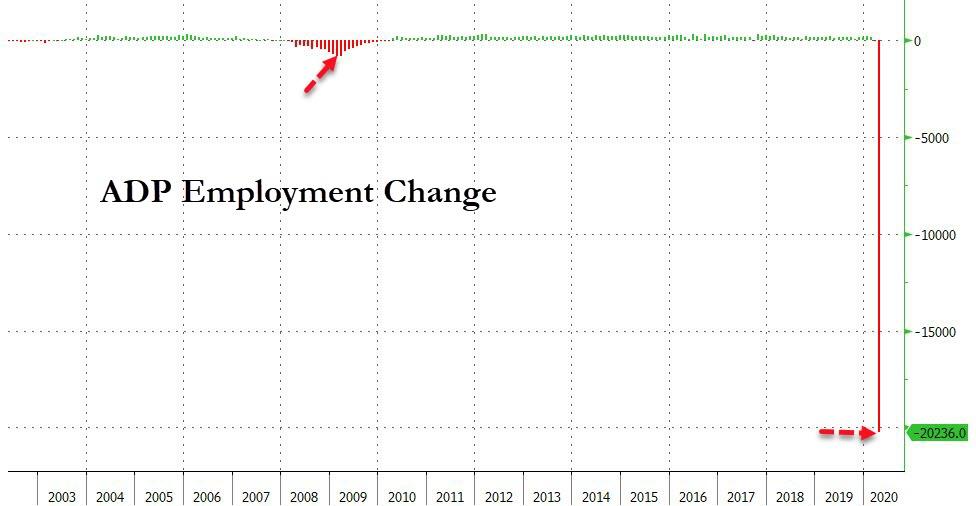

See if this makes sense to you. Today’s data released by the U.S. Labor Department (BLS) showed that we now have the worst unemployment rate since the Great Depression with 14.7%, while 20.5 million are out of work.

As a result, the markets rallied, presumably because the headline number was “less worse” than some estimates for 22 million unemployed. The fact that a broader measure of unemployment, that includes discouraged job seekers and other people on the fringes of the labor market, skyrocketed to a record 22.8%, was conveniently ignored. Wow, I am not making this up.

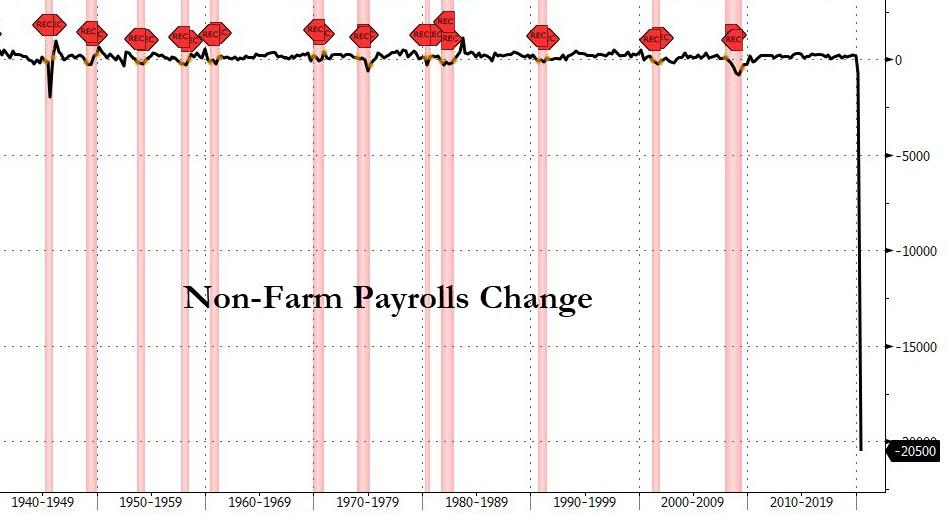

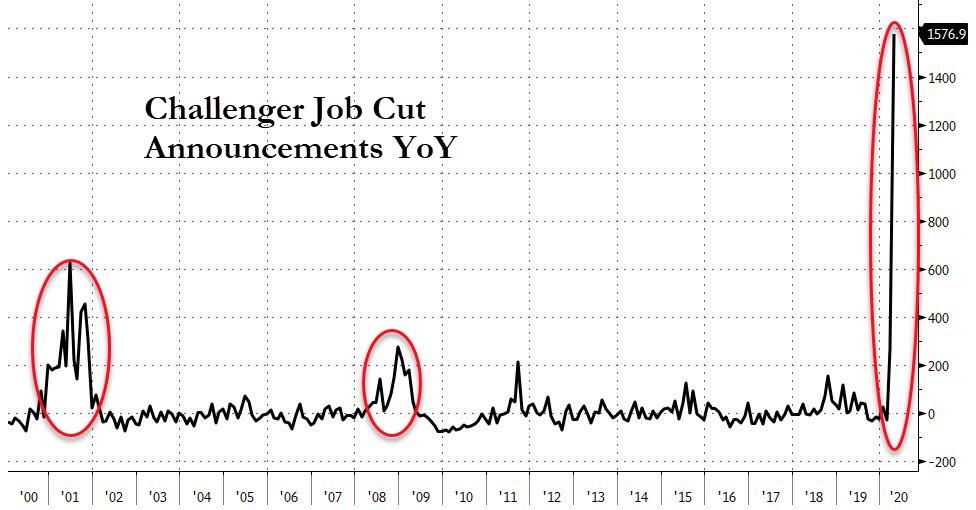

ZeroHedge added that this drop in unemployment is the biggest in history, and 10 times more than the 2 million jobs lost at the peak of the Great Depression.

Some clarification from the BLS:

Due to the impact of the COVID-19 pandemic, the relationship between the two was no longer stable in April. Therefore, the establishment survey made modifications to the birth-death model.

If the workers who were recorded as employed but absent from work due to “other reasons” (over and above the number absent for other reasons in a typical April) had been classified as unemployed on temporary layoff, the overall unemployment rate would have been almost 5 percentage points higher than reported (on a not seasonally adjusted basis).

In other words, the real unemployment rate is about 20%!

Since most of the above was generally as expected, the headline-scanning computer algos simply discounted this surreal economic weakness in view of some progress made towards the reopening of seized-up economies not just here but abroad as well, despite an only gradual loosening of restrictions. As if we could flip a switch and all be back to normal…

Even Morgan Stanley’s base bull scenario adds another year to the recovery, while the bear case sees double-digit unemployment into 2022 an onward—and that is assuming there is no second round of closures in late 2020.

With 52% of small businesses expecting to be “out of business” within 6 months, there will be no quick recovery, let alone a V-shaped one. I doubt that this has been priced in the markets.

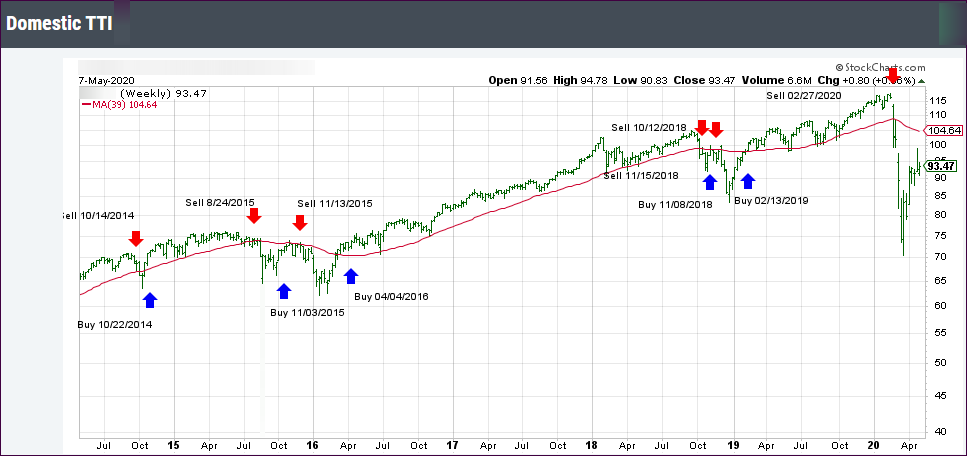

In the meantime, the bear market rebound rocks on, but it remains to be seen if it has enough momentum to push our Trend Tracking Indexes (TTIs) back into bullish territory.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}