ETF Tracker StatSheet

You can view the latest version here.

RISING BOND YIELDS = SLIDING TECH SECTOR

- Moving the markets

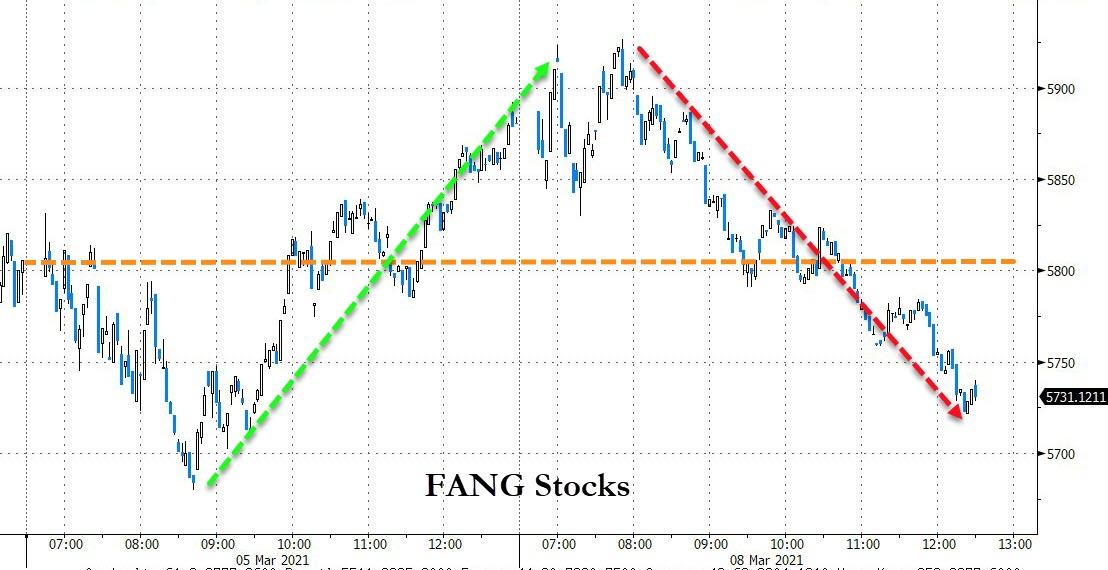

Again, it was the Nasdaq futures, falling as much as 2%, that predicted a sloppy opening of the regular session. That’s exactly what happened because bond yields spiked again, thereby taking the starch out of any investment with the word “growth” attached to it.

The 10-year bond yield dashed and topped its March 5th highs with the 30-year following suit keeping the major indexes in check. The exception was the Dow, which never dropped below its unchanged line and gained +0.90% for the day, in the process setting another record.

The S&P 500 climbed out of hole and managed to barely crawl back into the green. The Nasdaq’s attempt to do the same failed but early losses were greatly reduced.

The US Dollar inched higher by a modest amount, but today’s environment clearly belonged to the value sector with RPS and IJS, which we own, adding +1.58% and +1.46% for the session. Higher yields also benefitted the financial sector with XLF gaining +1.05%.

There is no question in my mind that higher yields, if allowed to continue to elevate, will be the biggest danger to all risk assets (equities), especially if Fed policies become less dovish at some point in the future.

Ned Davis Research seems to agree:

He estimates that the Nasdaq 100, the tech heavy index which tracks the 100 largest non-financial companies in the Nasdaq Composite, would drop another 20% if the 10-year yield hits 2%.

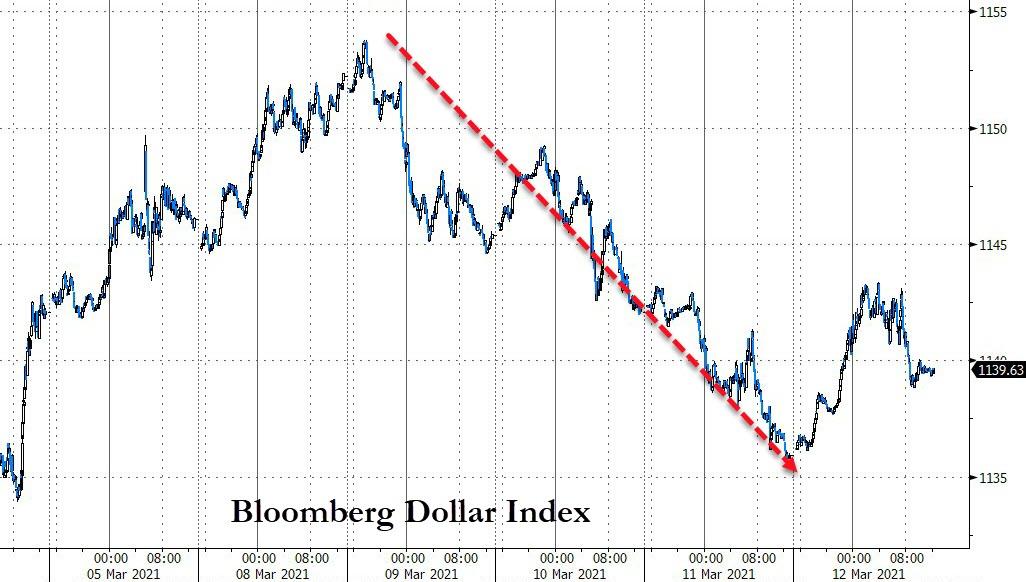

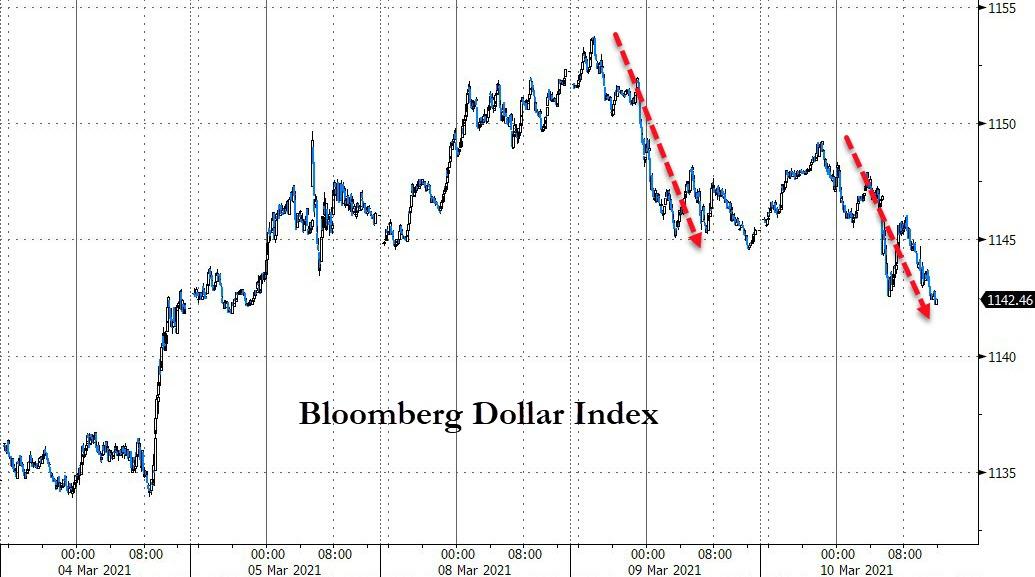

All bond yields have now reached pre-covid level, as Bloomberg shows in this chart. Once the inflationary forces are truly recognized, yields will continue to ramp higher.

However, keep in mind that during the initial phase of inflation, equities will rally, but once a certain, yet unknown point is breached, it will be all over for the bull market.

That’s the moment in time where the value of an exit strategy will become priceless.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}