- Moving the markets

With the markets having surged into April, it was time for the pace to slow down, and that is what we saw today.

The S&P 500 broke a 3-day winning streak with the indexes coming off their record highs, although by only a small margin.

Bond yields continued to ease up with the 5-year dropping below 0.90%, the US Dollar stumbled further, and both helped GLD to rebound with a +0.82% gain.

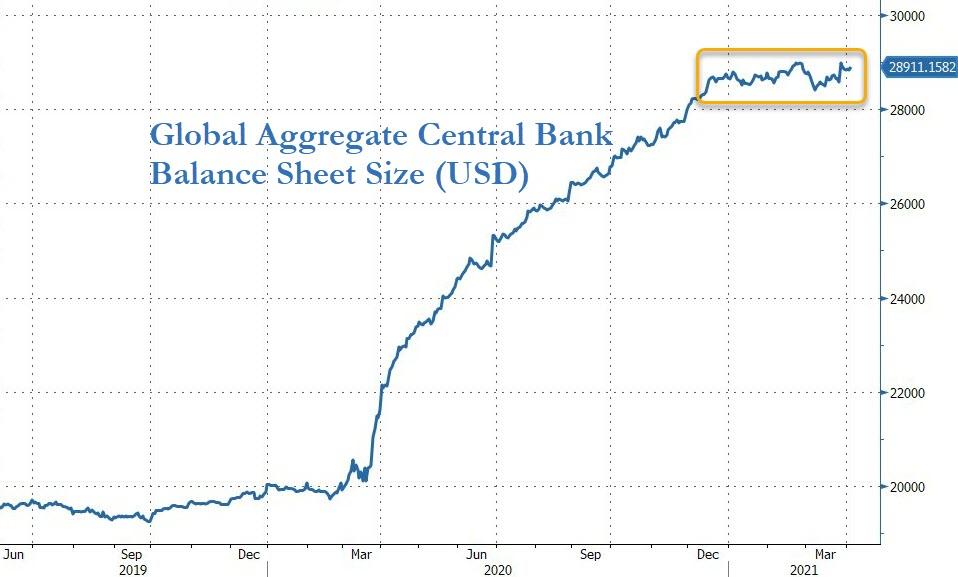

For sure, the historic stimulus efforts, despite their questionable long-term consequences, have helped equities to regain a solid footing after a wild ride in March. In addition, the vaccination rollout assisted in more businesses opening thereby paving the road for more optimism about the future direction of the markets.

The $2 trillion infrastructure proposal is still subject to much deliberation and pushback, while far from being a certainty in its present form. The size of the bill is still under discussion, as are some of the consequences, namely the impact of an increase in corporate taxes to 28%, along with other yet to be named tax hikes.

In the meantime, Q1 earnings season is on deck with the big banks kicking off the event next week.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}