- Moving the markets

Subdued trading best describes today’s session during which the major indexes operated within a tight range. Despite a red close, the losses were minor, and the activity resembled a lack of motivation due to key inflation data and first quarter earnings awaiting on deck.

Market volatility continued to decline, as seen by the S&P 500 having now traded within a 1% range for the fifth session in a row. Reopening optimism was a major contributor with the VIX “fear” gauge trading below 18, a level last seen over a year ago.

The current focus is on tomorrow’s CPI release, which is considered the benchmark for measuring inflation, although the index is faulty in that it does not include day-to-day items that we all know have increased in price.

Fed chair Powell made an appearance on “60 Minutes” last night and had the following to say:

We want to see inflation move up to 2% — and we mean that on a sustainable basis, we don’t mean just tap the base once, but then we’d also like to see it on track to move moderately above 2% for some time.

And then what? I disagree with his statement, because it makes you think that inflation can be controlled or simply turned off, once it exceeds or reaches a desired number. Unfortunately, history is riddled with evidence showing that once the genie, aka inflation, is out of the bottle, you can’t put it back in.

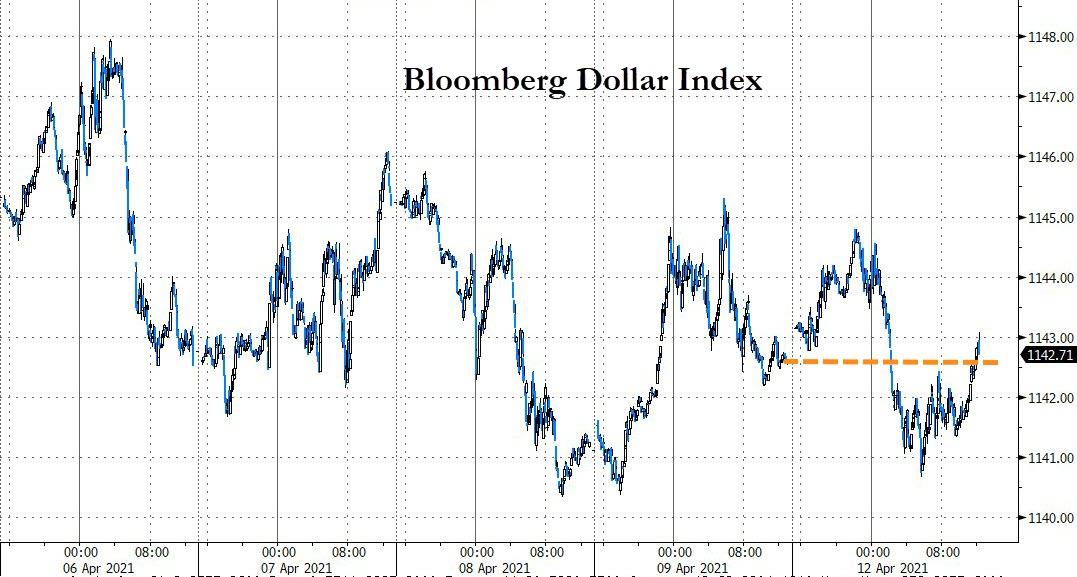

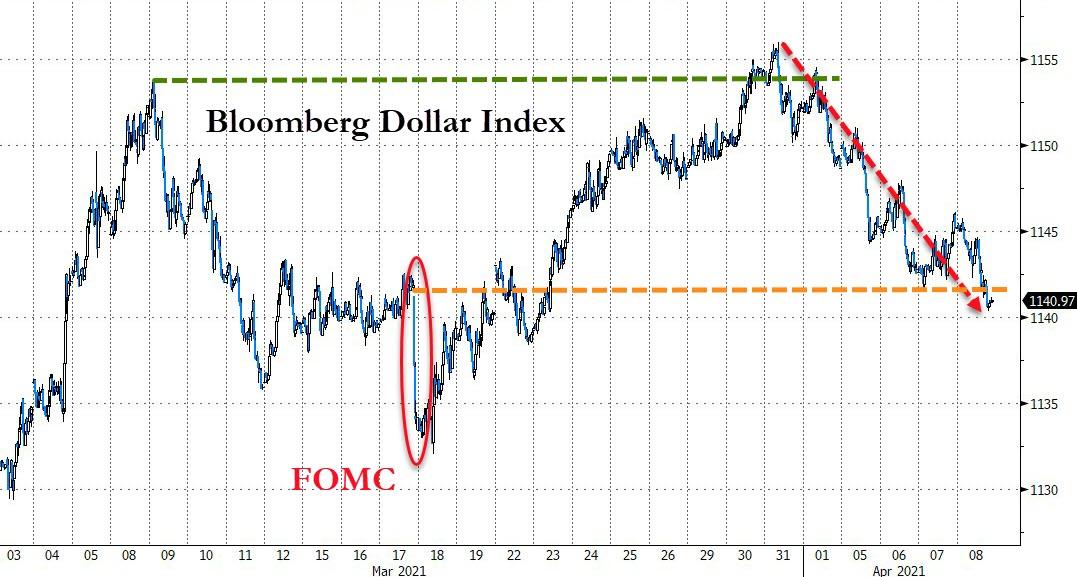

For the day, we saw 10-year bond yields treading water, the US Dollar meandering aimlessly, while gold slipped 0.72%.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}