Below, please find the latest High-Volume ETF Cutline report, which shows how far above or below their respective long-term trend lines (39-week SMA) my currently tracked ETFs are positioned.

This report covers the HV ETF Master List from Thursday’s StatSheet and includes 312 High Volume ETFs, defined as those with an average daily volume of more than $5 million, of which currently 253 (last week 264) are hovering in bullish territory. The yellow line separates those ETFs that are positioned above their trend line (%M/A) from those that have dropped below it.

In case you are not familiar with some of the terminology used in the reports, please read the Glossary of Terms. If you missed the original post about the Cutline approach, you can read it here.

The fact that the Fed’s announcement of higher rates possibly in 2023, some 2 years from now, caused such a disturbance in the financial markets, goes to clearly confirm the one thing I have been pounding on for years. Namely, that without artificially low interest rates and reckless bond buying by the Fed at the tune of $120 billion per month, stocks would be at a much lower level and are only hovering in bubble territory because of the Fed’s largesse, aka manipulation.

After all, how else can you explain this current fallout based only on the possibility of higher rates two years from now?

Be that as it may, today’s quadruple options expiration session greatly contributed to increased volatility with all major indexes hitting the skids, but it could have been far worse than the S&P 500’s 3.5% drop for the week.

To some investors, this pullback appears to be a big deal, but only because we have not seen these kinds of fluctuations since January, as market instability has been “well managed” over the past few months.

Not helping the sour mood on Wall Street was the Fed’s mouthpiece Jim Bullard, who told CNBC:

It was natural for the Fed to tilt a little “hawkish” this week and that the first rate increase from the central bank would likely come in 2022.

That was a change from the original forecast of two hikes in 2023, but who knows how much the narrative will change as time goes on. For right now, the Fed threw down the gauntlet, and the markets reacted.

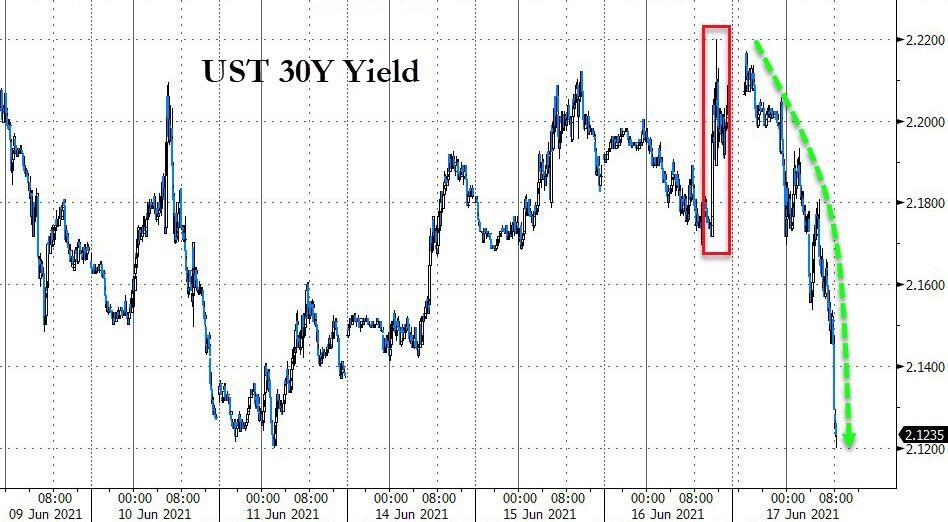

There was no escape as even energy, industrials, financials, and materials took a licking. The yield curve drastically flattened, which means that shorter term Treasuries, like the 2-year note, rose, while longer-term durations, like the 10-year bond, declined.

Elaborated CNBC:

The retreat in long-dated bond yields reflects less optimism toward economic growth, while the jump in short-end yields shows the expectations of the Fed raising rates.

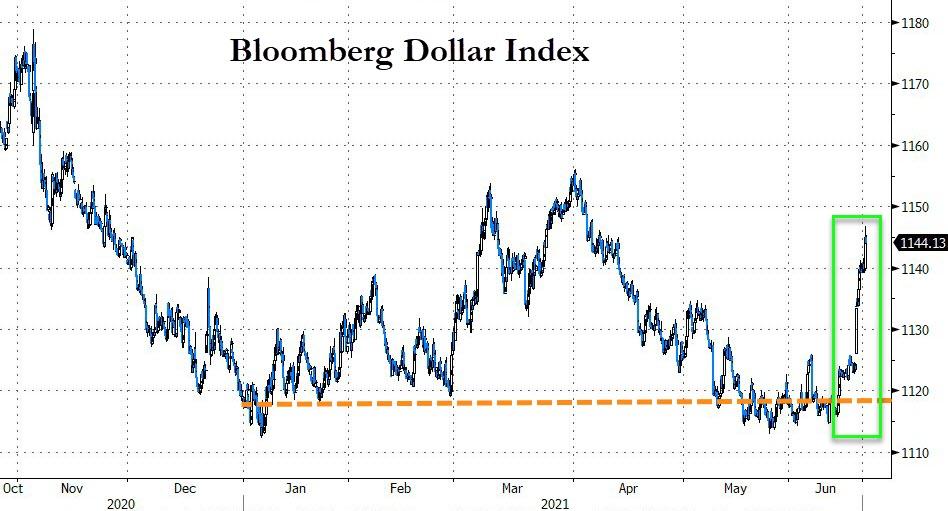

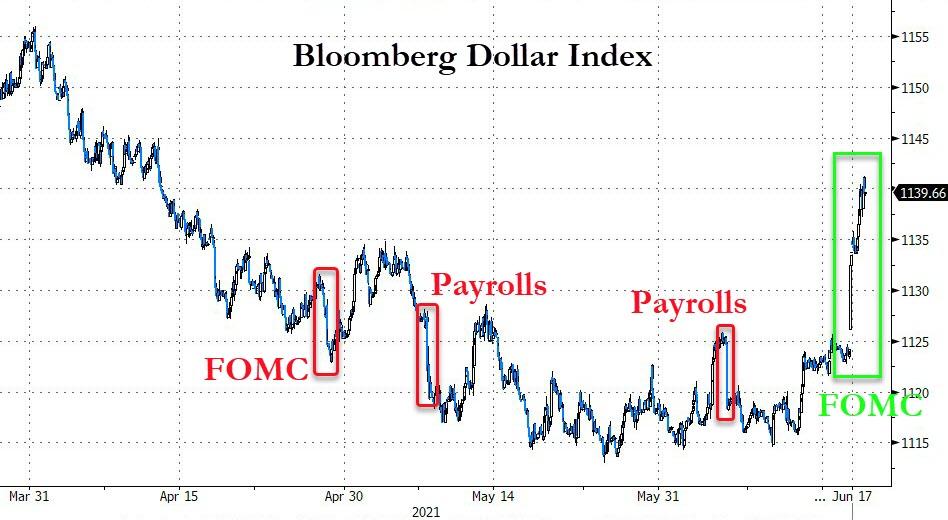

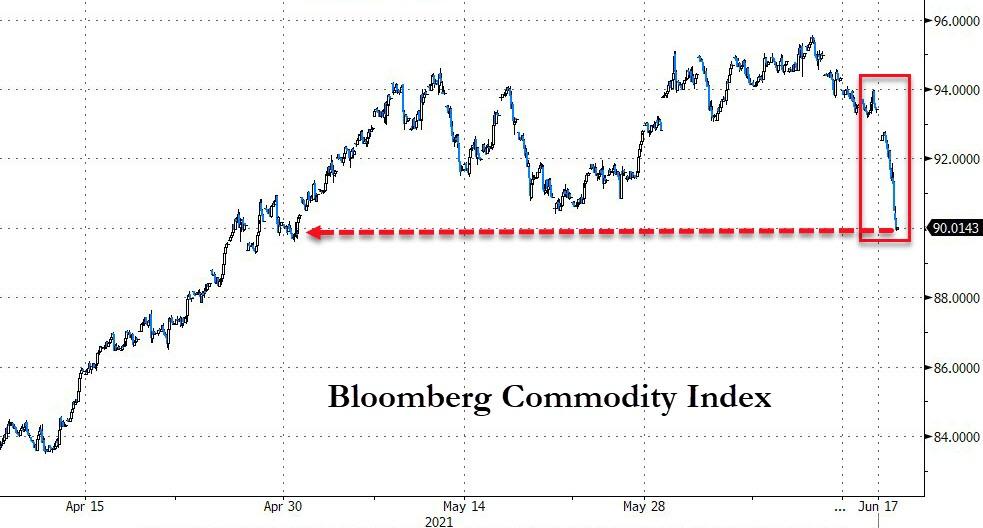

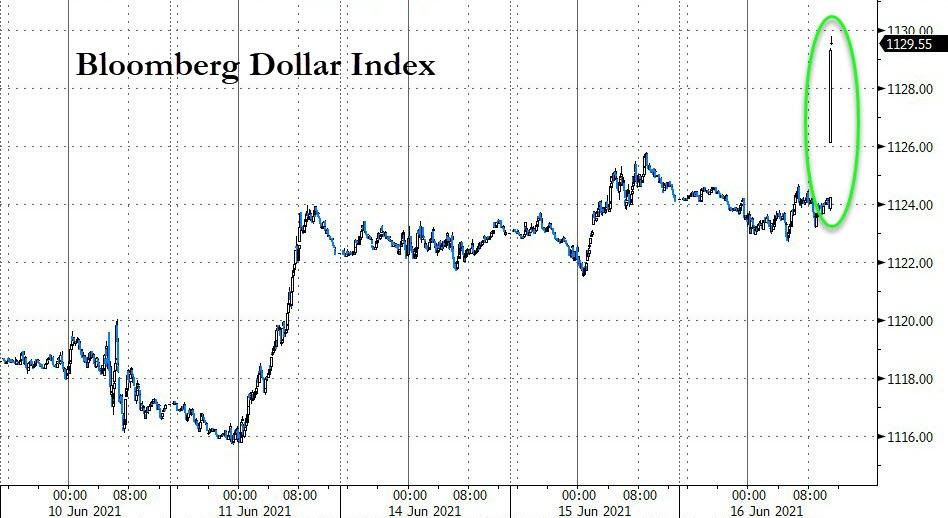

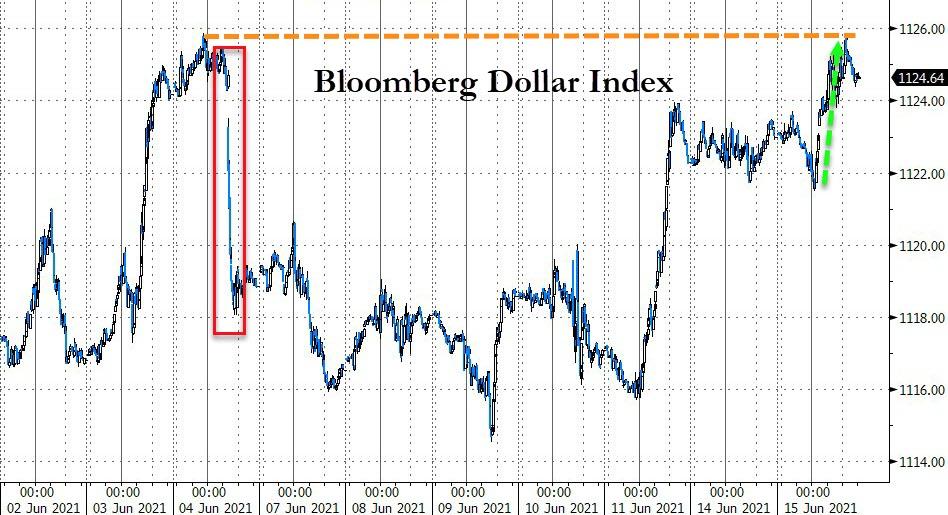

Despite getting hammered recently, commodities managed a bounce-back today, the US Dollar Index spiked sharply and is approaching March highs, which was enough to send gold into the basement, with the precious metal now having to climb out of a deep hole to get back to last week’s prices.

At least the always unpredictable quadruple witching hour has passed, and we will have to wait and see if traders will find market optimism over the weekend to pull the indexes out of their doldrums.

Or could it be that a bear market is in the making?

1. From the universe of over 1,800 ETFs, I have selected only those with a trading volume of over $5 million per day (HV ETFs), so that liquidity and a small bid/ask spread are assured.

2. Trend Tracking Indexes (TTIs)

Buy or Sell decisions for Domestic and International ETFs (section 1 and 2), are made based on the respective TTI and its position either above or below its long-term M/A (Moving Average). A crossing of the trend line from below accompanied by some staying power above constitutes a “Buy” signal. Conversely, a clear break below the line constitutes a “Sell” signal. Additionally, I use an 8% trailing stop loss on all positions in these categories to control downside risk.

3. All other investment arenas do not have a TTI and should be traded based on the position of the individual ETF relative to its own respective trend line (%M/A). That’s why those signals are referred to as a “Selective Buy.” In other words, if an ETF crosses its own trendline to the upside, a “Buy” signal is generated. Since these areas tend to be more volatile, I recommend a wider trailing sell stop of 8%-10% depending on your risk tolerance.

If you are unfamiliar with some of the terminology, please see Glossary of Termsand new subscriber information in section 9.

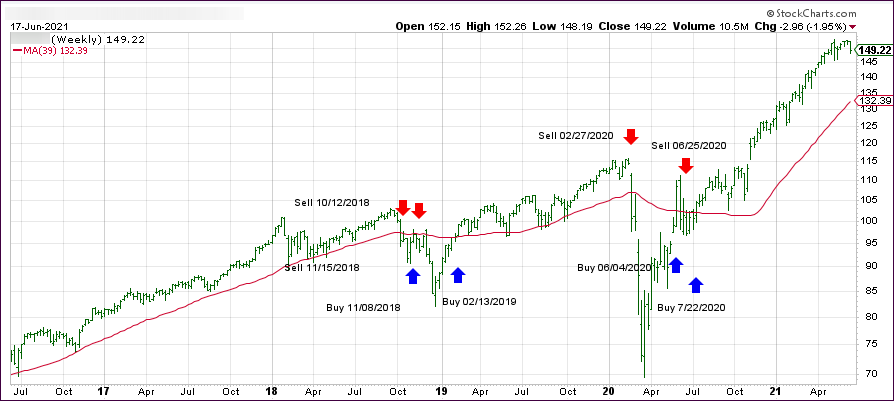

1. DOMESTIC EQUITY ETFs: BUY— since 07/22/2020

Click on chart to enlarge

Our main directional indicator, the Domestic Trend Tracking Index (TTI-green line in the above chart) has now rallied above its long-term trend line (red) by +13.59% and remains in “BUY” mode as posted.

The morning, after the Fed’s announcement that it envisions two rate hikes in 2023, thereby subtly admitting that inflation may not be transitory, traders were shocked to see today’s market reaction, as this chart demonstrates.

ZeroHege described it this way:

Traders are watching in stunned amazement at what is going on in the market where contrary to everything the Fed has said, we are seeing a stampede into tech, growth, and duration-sensitive names…and a flight out of reflation and value sectors…

Bonds were in a world of their own when, after yesterday’s yield spike, which represented a normal reaction to potentially higher rates, opposite day arrived and slammed yields lower back down to the June 11 level. The 30-year yield crashed down to a price last seen on November 20.

Huh? Even seasoned traders watched this unreal development open-mouthed and were not able to come up with a reasonable explanation. Bank stocks got hit hard, which pushed the Financial Sector ETF down -2.90%. The US Dollar surged for the 5th straight day, as ZeroHege pointed out, thereby clubbing Gold like a baby seal, which slumped -4.68% and dropped below its $1,800 level. Ouch!

It was a day where nothing made sense and even the inflation-sensitive commodity sector got annihilated and suffered its biggest drop since March 2020. In other words, things that should not have happened did happen.

In the end, it may not have been the Fed causing havoc in some market sectors, but what is about to take place tomorrow. That is massive options expirations in SPX and QQQ with a total value of some $2 trillion!

What we saw today may have been just a front run of tomorrow’s main feature.

Despite the Fed leaving interest rates unchanged for the time being, it was the outlook that disturbed the bulls today. Inflation expectations were raised to 3.4% for 2021, which is 1% higher than the March projection.

The time frame as to when rate hikes might occur was moved to 2023, during which two increases are now projected. That came as a surprise after March’s announcement that such action may not be on deck until at least 2024.

The broad market dumped, including all 11 S&P sectors showing red numbers at one point, and there was no escape to safety. Apparently, beliefs were that the Fed would sit on its hands, so today’s hint that rates will need to rise sooner and faster, came as a surprise.

Regarding the Fed’s monthly $120 billion bond buying program, designed to keep bond yields low and make debt service feasible, no changes were announced.

The fallout was instant, as the US Dollar surged and bond yields rose, which caused stocks to tumble and Gold to dive.

The big question is this one: “Can the markets absorb this news without much damage, or will sentiment favor the bears from hereon forward?”

As I posted yesterday, more of the same was indeed how this session turned out. Traders stayed away from making new commitments and, due to lack of buying enthusiasm, the markets drifted aimlessly ahead of tomorrow’s Fed announcement.

Although the major indexes wandered into the red, keep in mind that they are still within striking distance of new all-time highs, so this two-day slippage is meaningless.

Looking at the big picture, the tech sector surrendered yesterday’s gains, as “value” was favored over “growth” today, with RPV managing a +0.35% gain while Small Caps hit the skids by given back -0.98%.

On the economic front, retail sales for May fell 1.3%, worse than an expected 0.7%, and the Producer Price Index rose 0.8% vs. an anticipated 0.6%. While these numbers had a negative market effect, this was mitigated somewhat by the upcoming Fed meeting results due out on Wednesday.

Bond yields pretty much trod water, but the US Dollar broke out of its short-term sideways pattern and touched its June 4th highs. As is the case when dollar rallies, Gold lost its luster for this session and gave back -0.30%.

Concluded ZeroHedge:

Finally, the dismal disappointment in retail sales today, combined with Empire Manufacturing’s miss, a worse than anticipated drop in homebuilder confidence, and a bigger than expected drop in business inventories, the US macro surprise index fell to its lowest since May 2020…

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}