ETF Tracker StatSheet

You can view the latest version here.

WHEN BAD NEWS IS GOOD NEWS

- Moving the markets

The much-anticipated jobs numbers turned into a huge disappointment and were downright shocking when the BLS revealed that only 266k jobs were added vs. expectations of 1 million.

Worse yet was the fact that, when looking under the hood, as ZH pointed out, it became clear that had it not been for some 187k workers added in food service and drinking places (waiters and bartenders), as well as 72k in gambling, amusement and recreation workers, the April print would have been virtually unchanged from last month. Ouch!

Not to worry, the markets in their infinite wisdom took this economic horror show and concluded that bad news is good news again, which CNBC explained like this:

Investors bet that the big jobs miss could keep the easy policies of the Federal Reserve in place, including record low interest rates and a massive bond-buying program. Tech stocks, which have been winning under the low-rates regime during the pandemic, outperformed after the data release.

To make sure, you understand that today’s bad numbers were good news, Treasury Secretary Yellen came out and said this:

I would note that the jobs report is a little bit stronger than the headline numbers might suggest on the hiring front.

Huh?

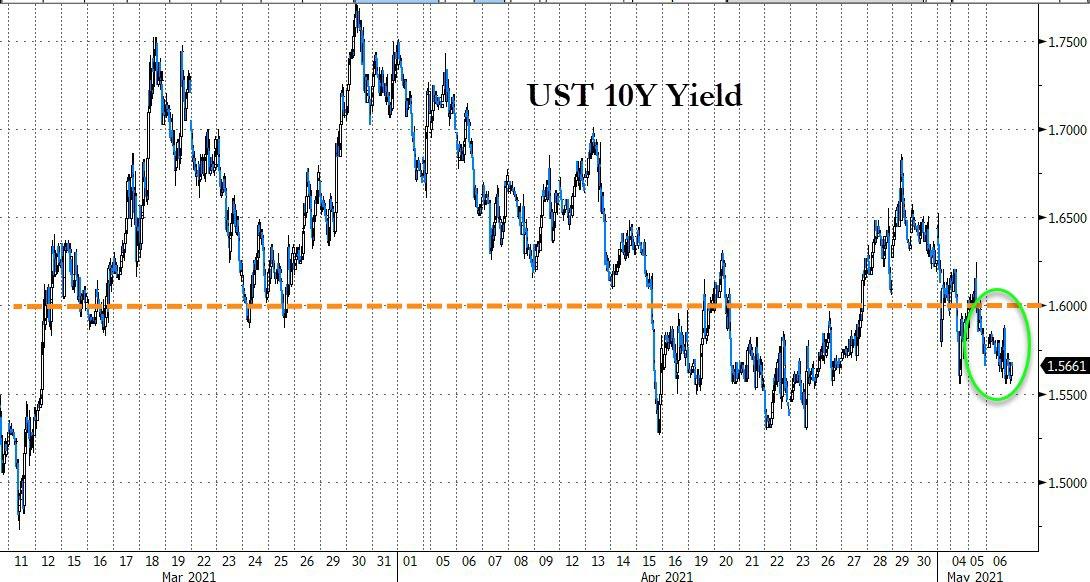

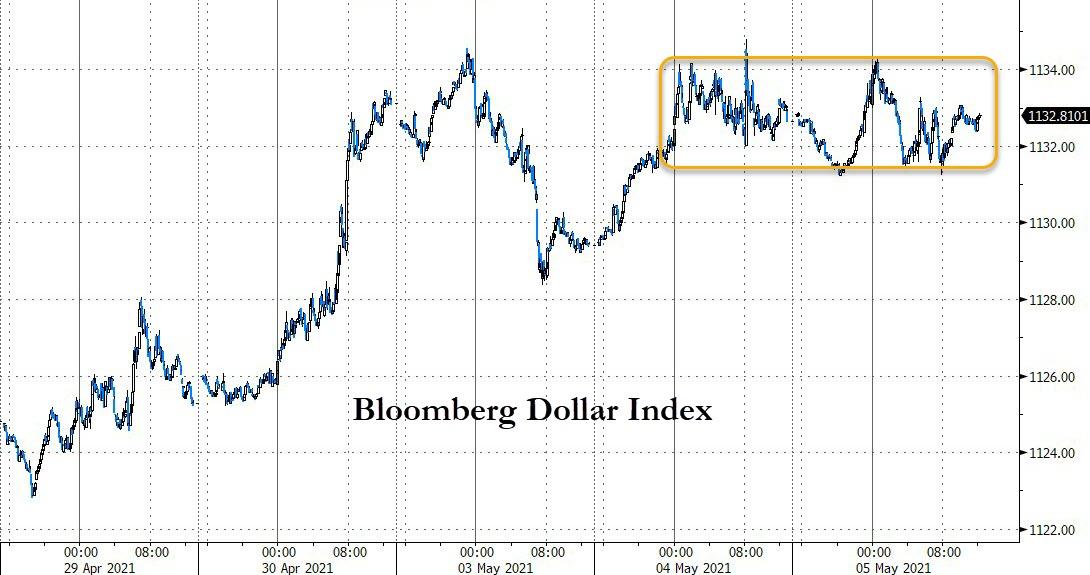

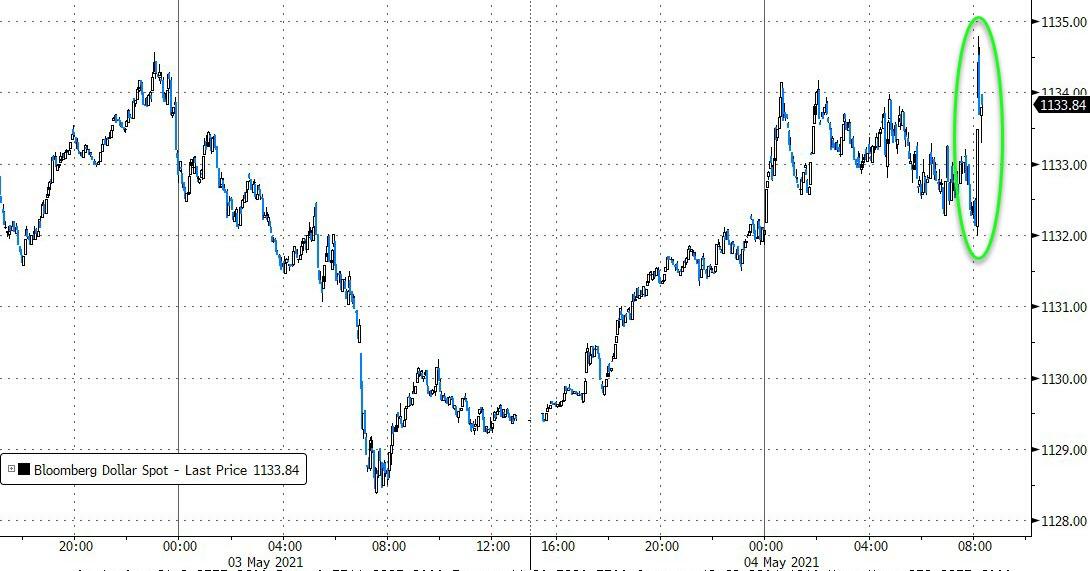

Be that as it may, the markets surged, with the Dow setting another record, and all 3 major indexes closed in the green, with the Nasdaq leading for a change. Bond yields dipped and ripped with the 10-year almost unchanged, while the US Dollar plunged again.

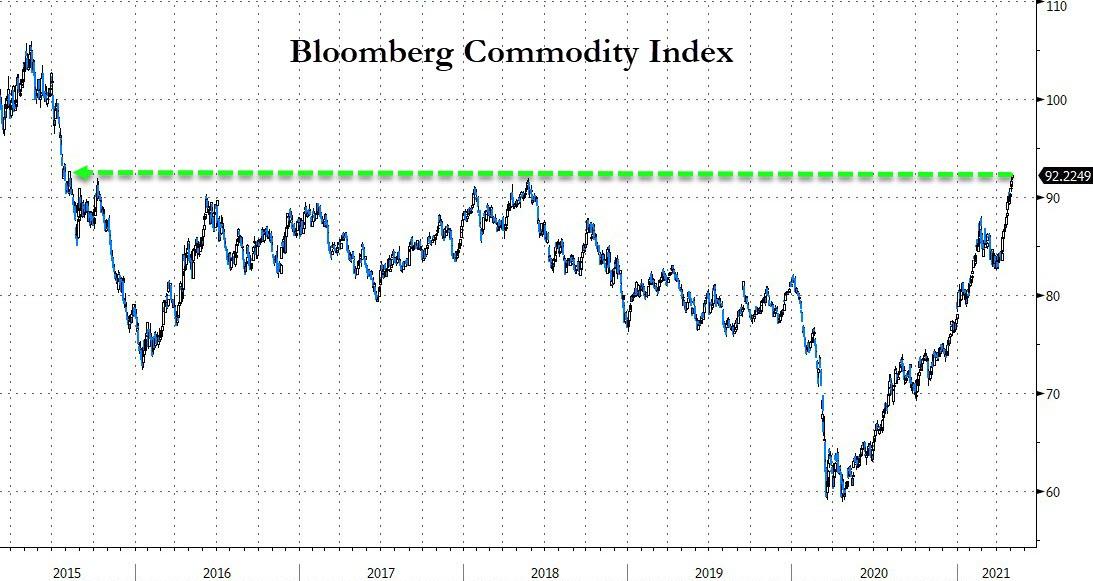

Commodities continued their run to towards taking out the 2011 high with the index being up an amazing 65% YoY, which is a record spike, according to ZH.

All the uncertainty, with inflationary concerns on the rise, benefited Gold, which not only ended at $1,840, its highest level in 3 months, but also had its best week since last November.

I think, as inflation turns out not to be “transitory,” as the Fed would have us believe, the precious metal may just be in the early stages of a new bull run.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}