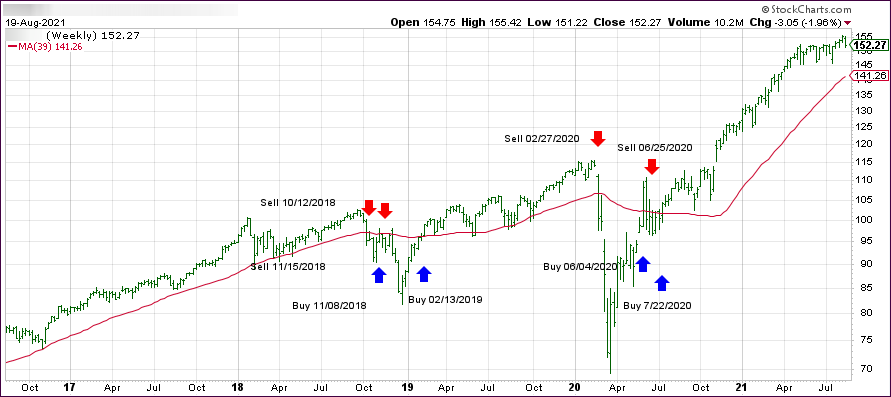

- Moving the markets

The futures markets already indicated a strong opening, which is exactly how things played out. The major indexes roared out of the gate with all three of them displaying solid gains, but the leader was the Nasdaq by showing off with an advance of +1.55%.

Last week’s weakness was shoved in the rear-view mirror, when Fed VP Kaplan, after Friday’s close, uttered those words that markets are dying to hear, namely that “he’s open to adjusting his view that the Central Bank should start tapering sooner rather than later if the Delta variant persists and hurts economic progress.”

Wow, how much clearer can he be to announce that talk about tapering was just that: Empty talk.

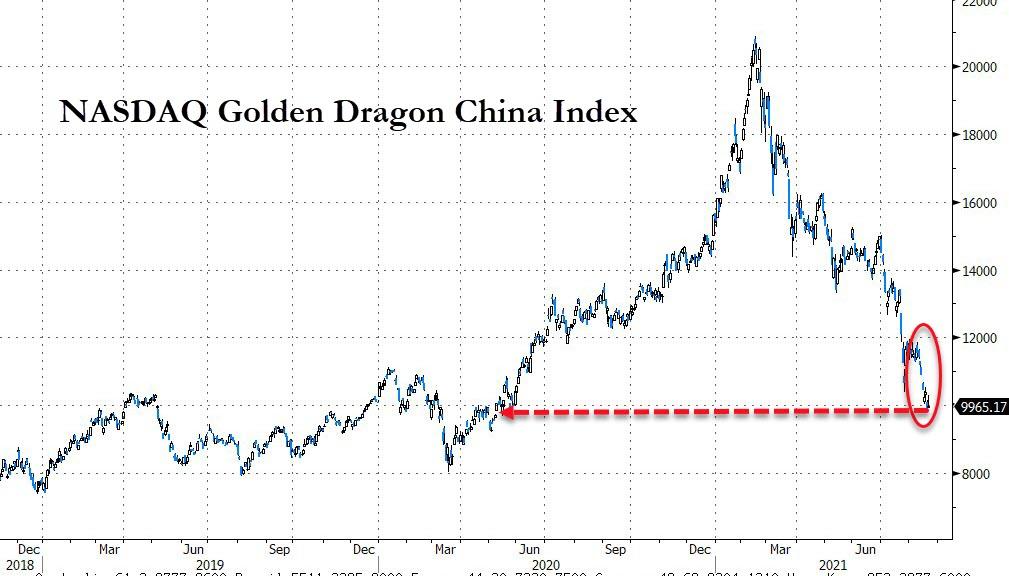

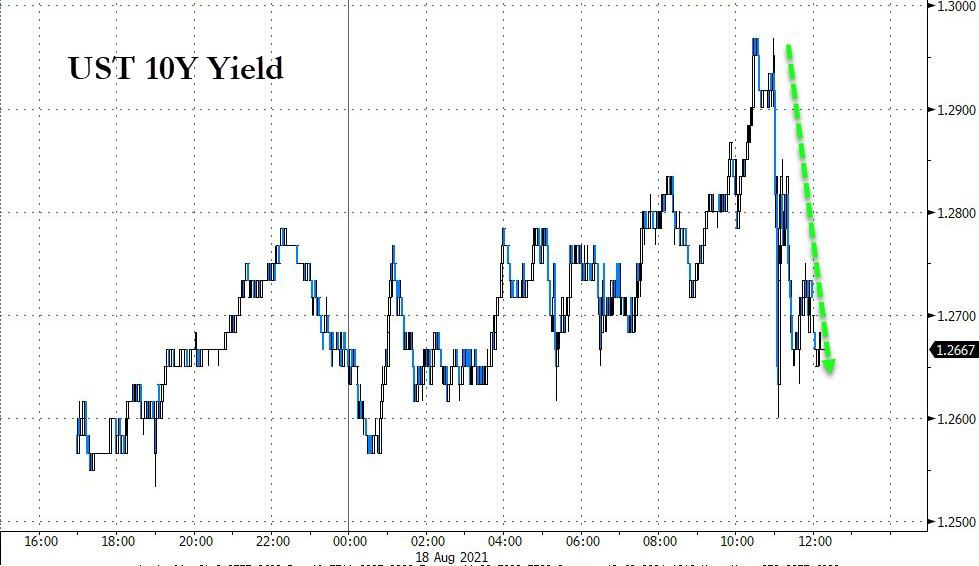

Be that as it may, market reaction was broadly bullish with even the international arena recovering from its recent swoon and participating in today’s “Ramp-A-Thon.” The US Dollar took a swan dive, with bond yields joining in, as the 10-year dropped to 1.25%.

That caused Gold to take off with the precious metal not only rebounding +1.26% but also reclaiming its psychologically important $1,800 level.

The key event is the upcoming Jackson Hole, WY virtual symposium and Fed head Powell’s highly anticipated speech later this week causing a wave of speculations. Here’s one:

Our base case is that the FOMC will announce a taper in September if the August non-farm payrolls is strong,” said Joseph Capurso, head of international economics at CBA. “We anticipate the taper will be implemented in October or November, though the recent increase in Covid infections and deaths in parts of the U.S. may give Powell pause.

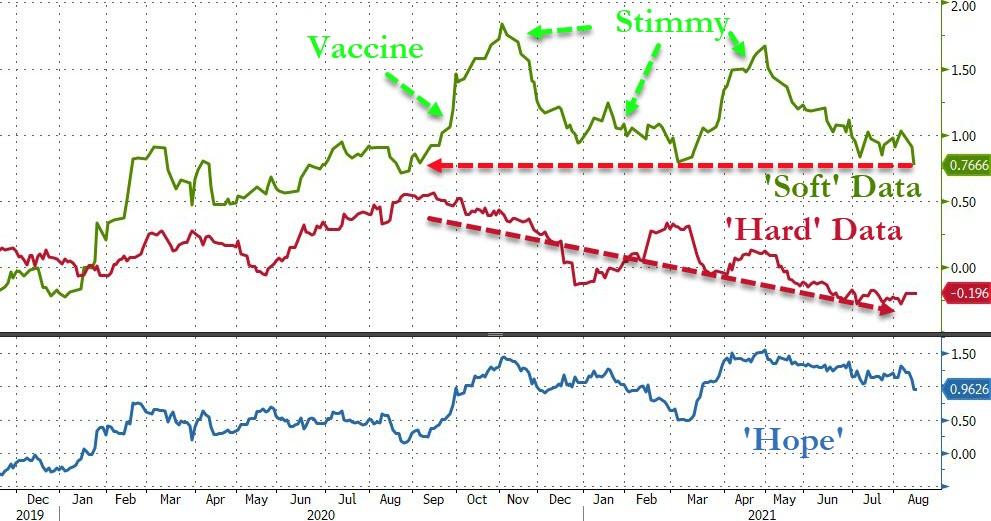

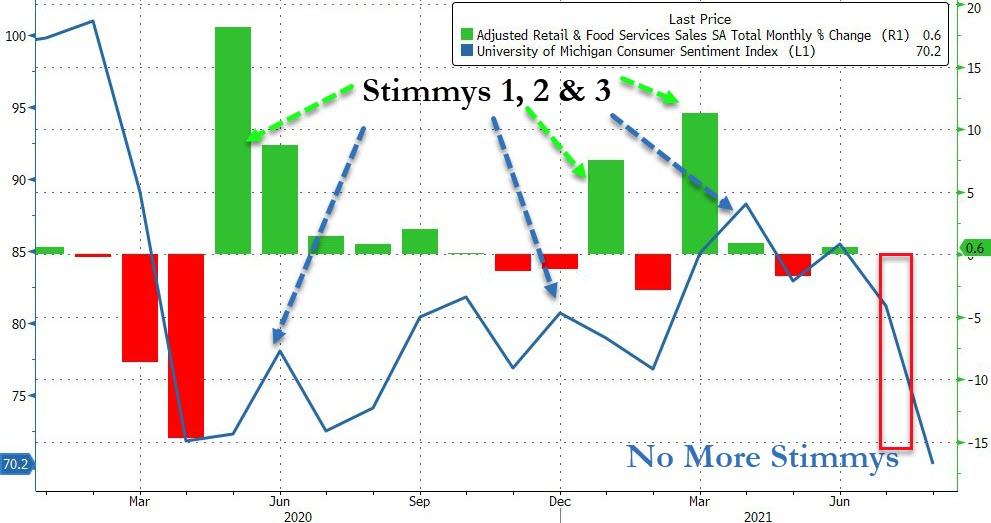

It seems something went awry in the markets today, as equities totally disconnected from the bond markets, as Bloomberg demonstrates in this chart leaving me pondering as to who will be right in the end.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}