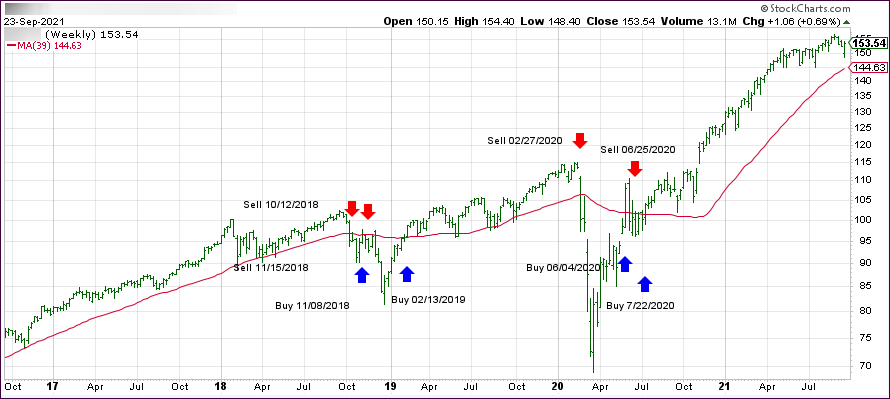

- Moving the markets

The bulls and bears were engaged in a tug-of-war session with the former seemingly storming ahead only to be pulled back down to reality by the latter. Gains came and went and, when the closing bell rang, only the Dow & S&P 500 were able to barely stay above their respective unchanged lines.

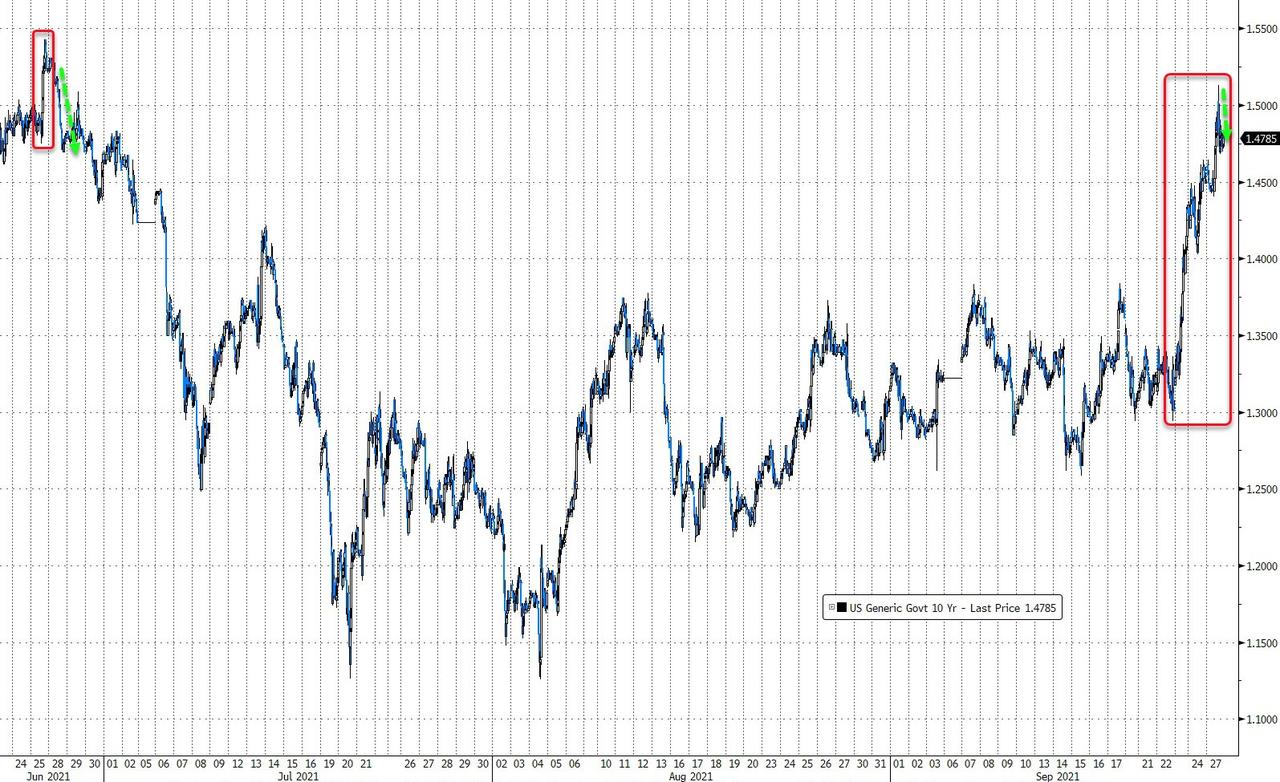

The culprit was the same as yesterday, namely bond yields, which rode the roller coaster again with the 10-year first dropping to 1.5% and then swinging higher in afternoon trading into the 1.54% area.

The Nasdaq followed this trend by being higher early on, as rates eased, but then lost altitude as yields again marched higher. As a result, the pressure was on “growth” with “value” and Small Caps benefiting.

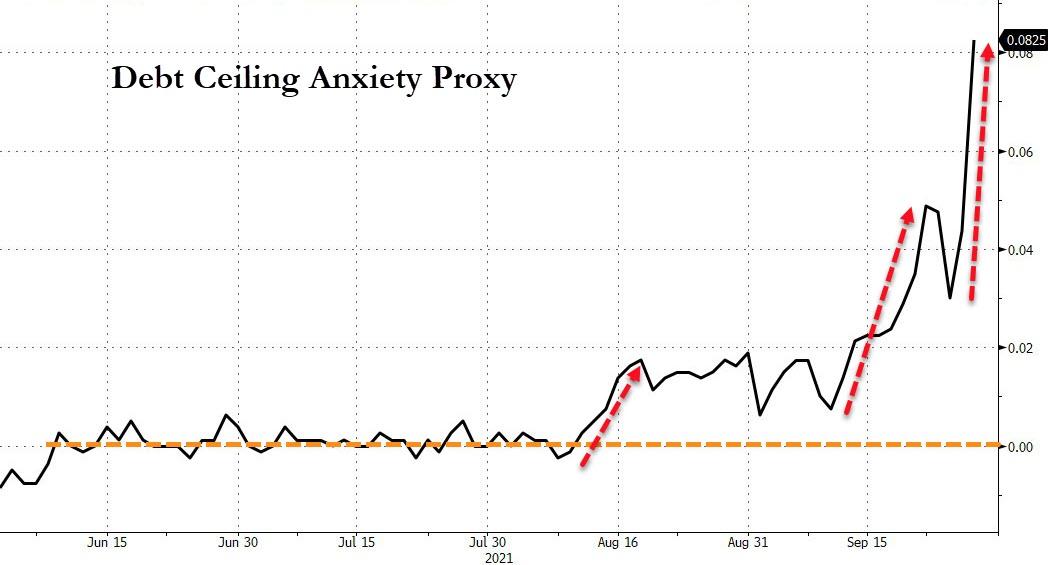

Giving an assist to bearish sentiment was the ongoing Washington debacle with debt ceiling doubts sending questionable messages to the international community about the ability of the USA to fulfill its obligations.

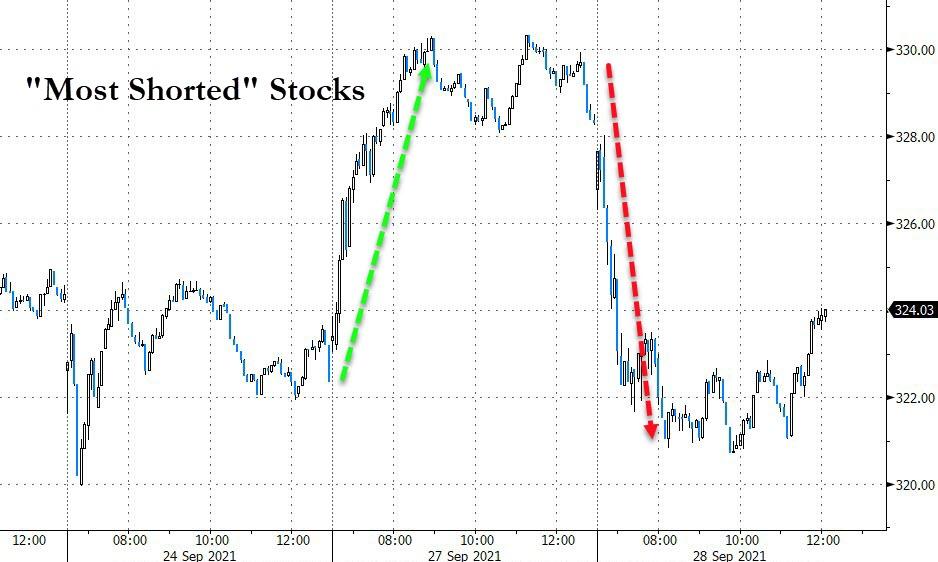

Choppy and sloppy best describes today’s equity moves, as dip buyers where present during the session but absent late in the day, as equities came off their highs. It now looks like the S&P 500 is on track to score its first monthly decline since January.

Zero Hedge called it this way:

While rising bond yields, Fed tapering, the delta variant and inflation help explain that, all of those will slow profit growth after rising earnings estimates and big beats helped fuel 2021’s stock rally until now with an always-optimistic eye for the ‘recovery’ and ‘return to normal’ that now seems ever further away.

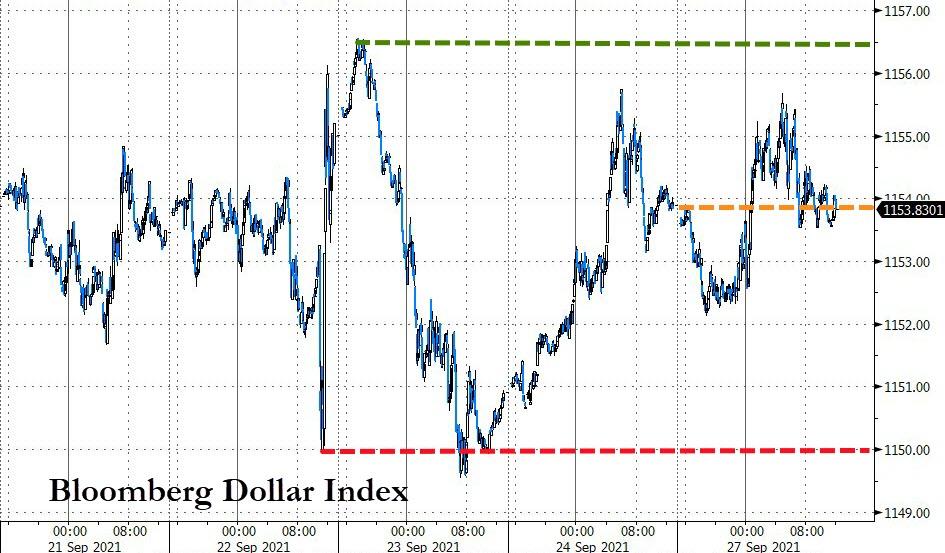

The US Dollar index, in the face of higher bond yields, continued its northerly path by registering its biggest 2-day jump since June, and it seems to be closing this September on a high note, just as it did in 2020.

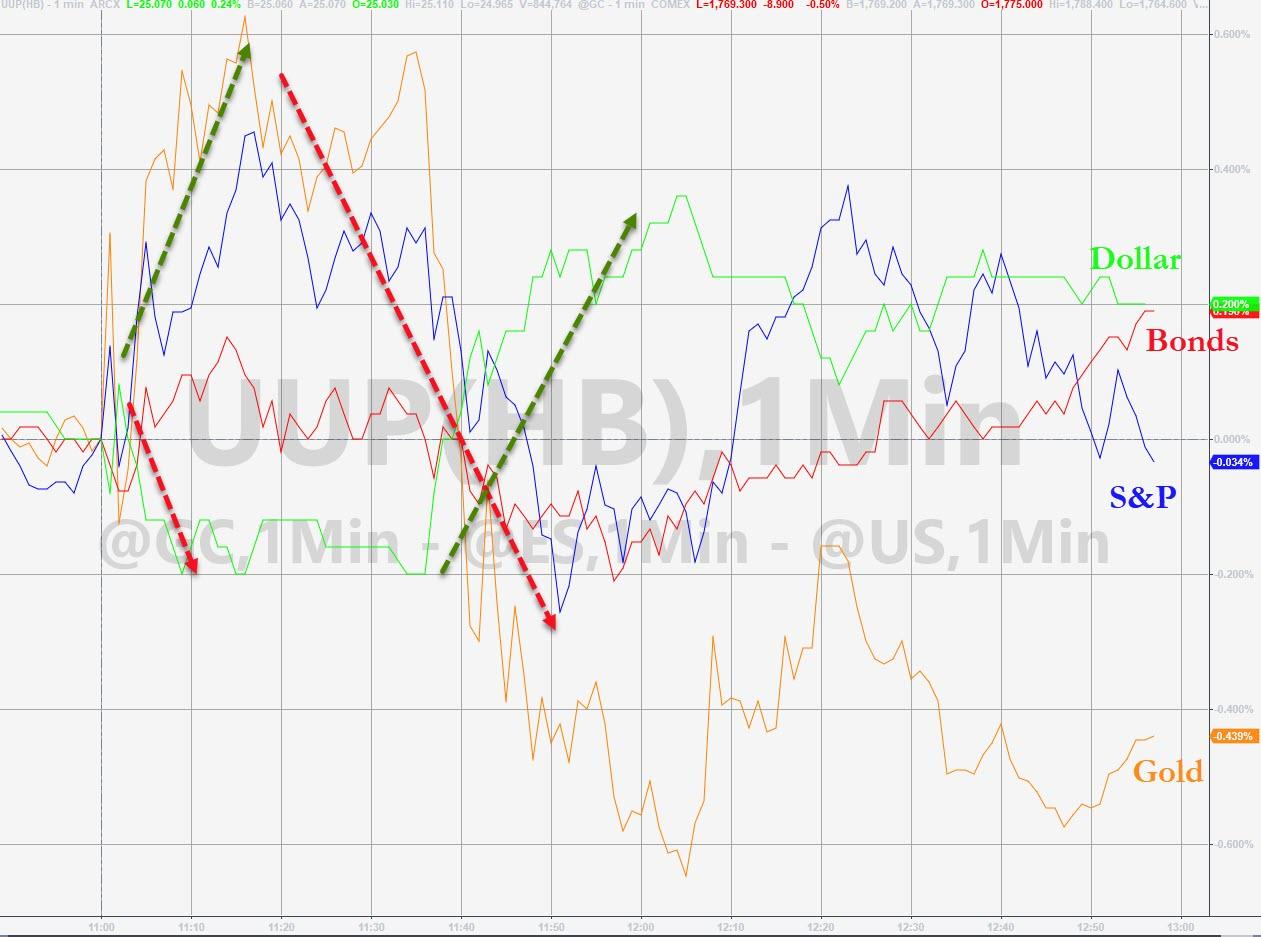

Again, higher bond yields and a rallying dollar combined to take the starch out of Gold which, despite a mid-day rally, was not able to hold on and retreated -0.72%.

So far, the analog to 1987 is right on track, as Bloomberg’s chart shows.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}