- Moving the markets

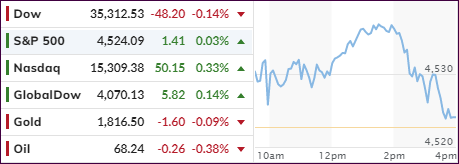

The markets stumbled into the first trading day of September with an early rally running out of steam, but the major indexes managed to stay close to their respective unchanged lines. The exception was the Nasdaq, which showed most of the staying power by not only remaining solidly in the green throughout the session but also hitting a new intraday all-time high.

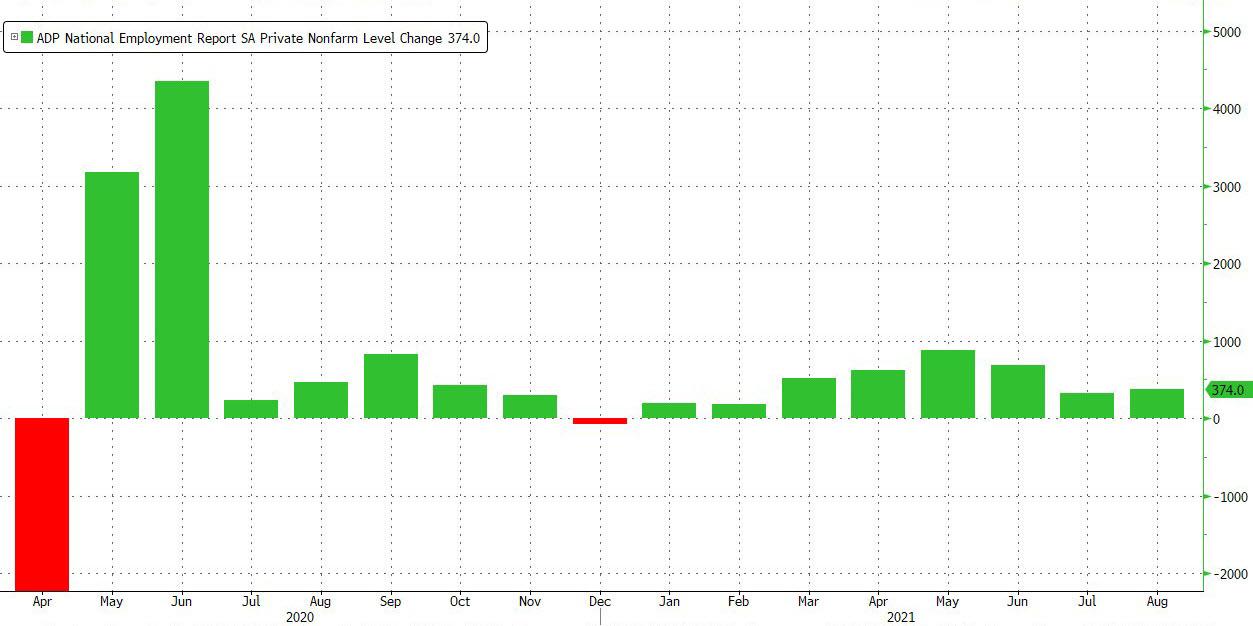

In the end, it may have been ADP’s dismal private payroll numbers, which took the starch out of the early bounce.

ZeroHedge explained it this way:

For the second month in a row, the ADP Private Payroll employment report has been a complete disaster, and one month after the the ADP missed by almost half printing at 330K in June (missing expectations of 683K), ADP reported that private payrolls in August rose just 374K, which while a modest improvement from July’s downward revised 326K (which was the lowest since February), was again a huge miss to the 638K expected, and was in fact below the lowest forecast by polled economists (+400K).

That has traders on edge, because this report is a precursor to the official August non-farm payrolls data due out this Friday. Expectations are the creation of 720k new jobs along with a drop in the unemployment rate to 5.2%.

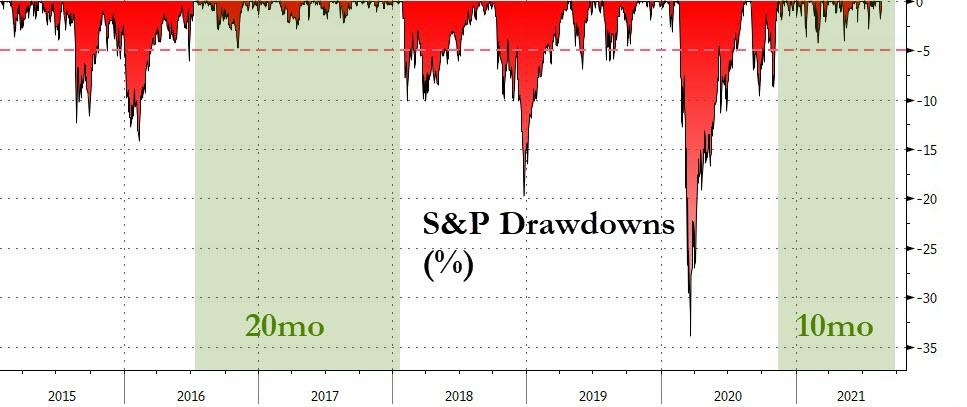

Some analysts are also concerned about a correction in September, which is historically the worst month of the year for equities. Additionally, stocks have not had a significant pullback since last October. However, given the Fed’s dovish attitude, who knows if history will repeat itself.

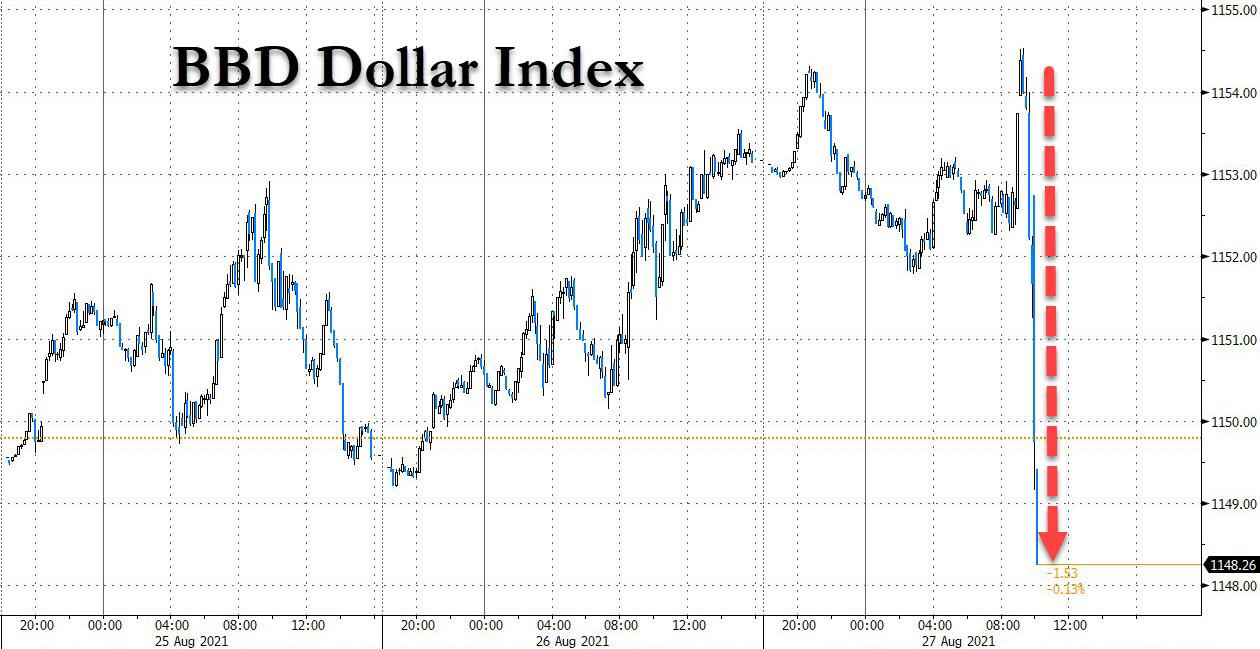

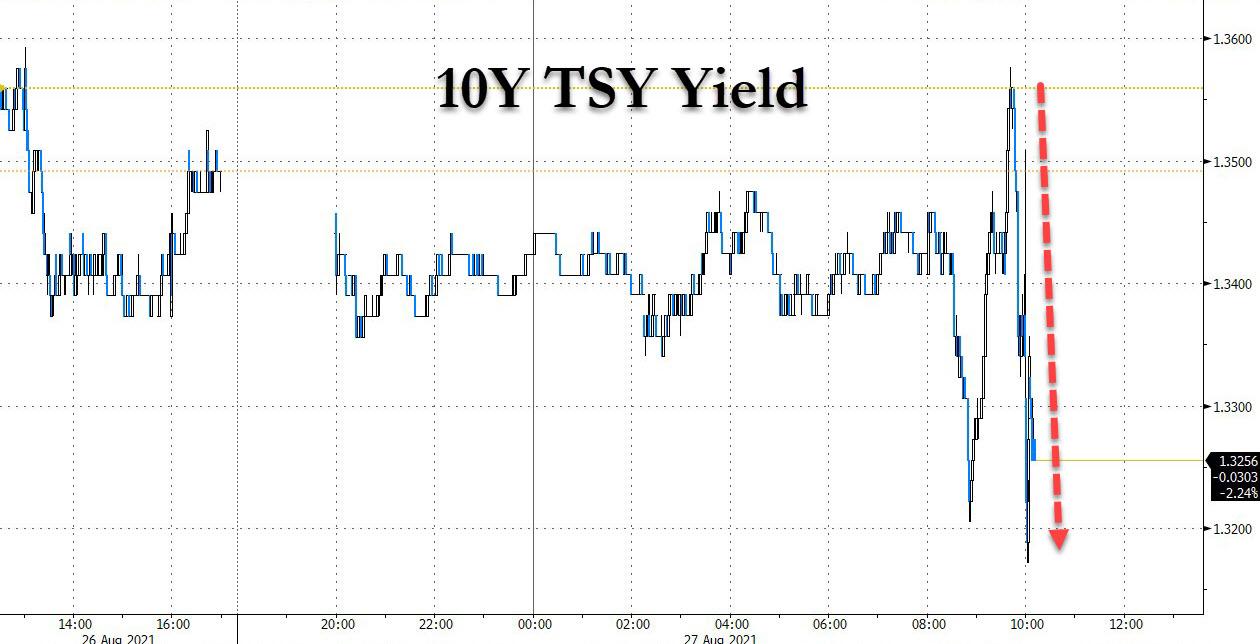

Bond yields took a dive early on, after the ADP report, yet bounced back with the 10-year ending at 1.3%. The US Dollar dropped moderately, and gold closed just about unchanged.

If Friday’s payroll report confirms that jobs growth is indeed slowing, this could have a negative effect on the economy, but a positive one the stock market.

Why?

It means that easy monetary policy will likely continue. In today’s twisted reality, that is how bad economic news becomes good news for the markets.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}