- Moving the markets

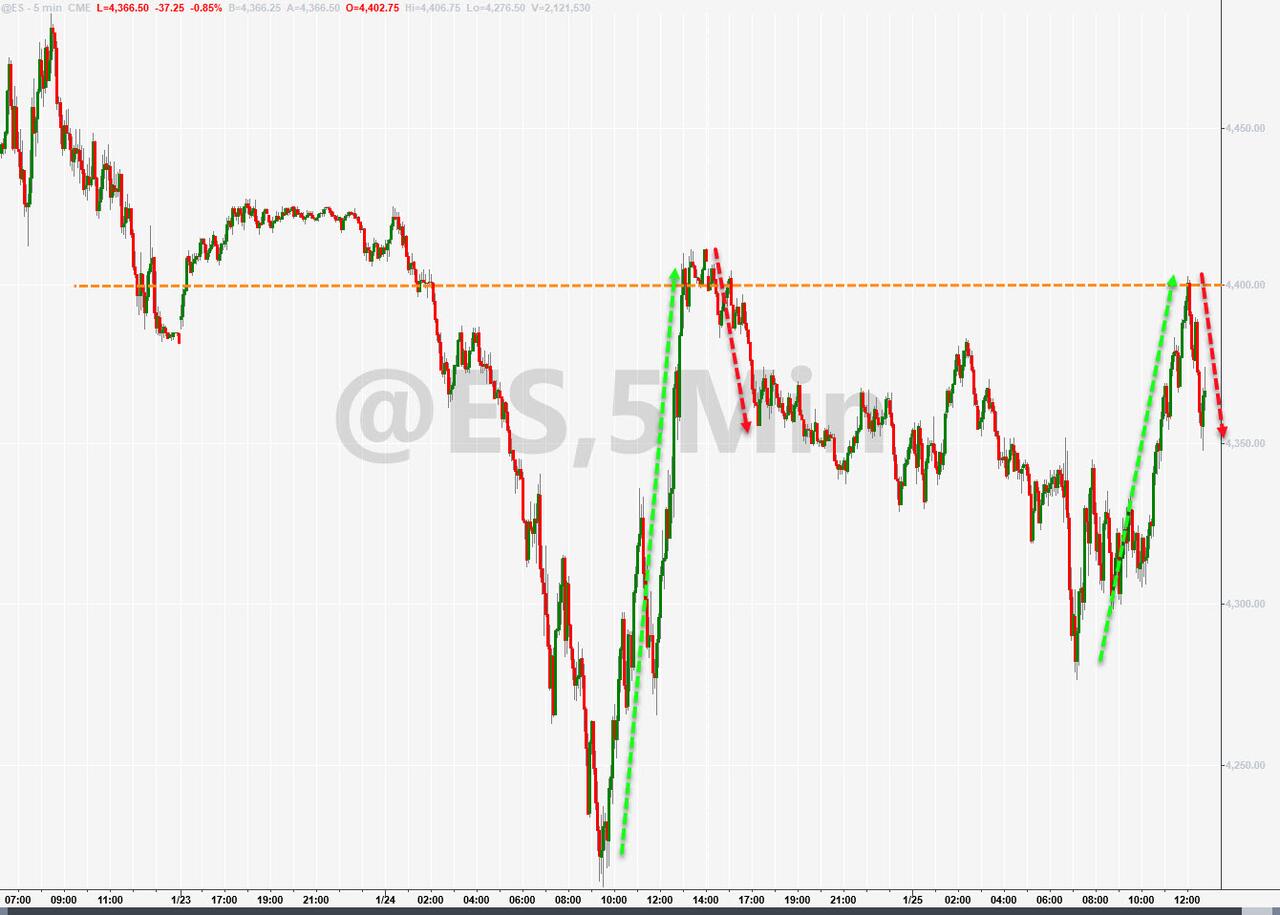

An early anticipatory rally bit the dust after the Fed’s announcement that they have plenty of room to raise interest rates before the economy would be negatively affected. The major indexes dove into the red but rebounded into the close.

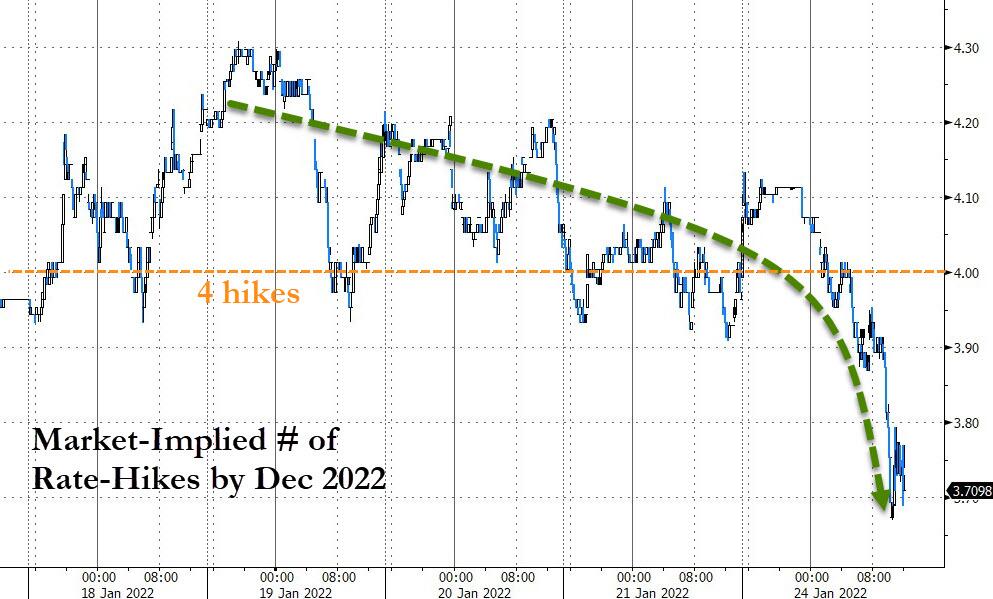

Rate hike expectations soared with traders now considering 4 hikes by year-end to be a real possibility, but the Fed did not lean towards outright hawkishness or dovishness. ZH summed it up like this:

- The Fed says it “will soon be appropriate” to raise funds rate.

- The Fed says asset-purchases will end in March…

- And The Fed says that balance-sheet-shrinking (QT) will start after rate-hikes commence.

- The Fed intends primarily to hold Treasuries in the longer run.

- Finally, The Fed believes, “overall financial conditions remain accommodative.”

In other words, Fed head Powell walked the tight rope, and in my mind was not hawkish enough in his intent to seriously fight inflation.

Analyst Danielle DiMartino Booth described the Fed’s dilemma most succinctly:

“The Fed’s biggest challenge is figuring out how to implement policy measures that are hawkish enough to lower inflation, but that also keep financial markets afloat, because volatility in financial markets may bleed into an economy that is already showing signs of slowing. The Fed is faced with choosing the lesser of two evils.”

In the end, the Fed statement did not contain any surprises, because an early end to tapering was not announced, and neither was an earlier start to rate hikes. The most feared words that a 50-basis point hike (as opposed 25 bps expected) might be on the agenda did not happen.

However, confusion reigned when Powell released this double speak (hat tip goes to ZH):

“Economy no longer needs sustained high levels of monetary support.”

BUT…

“Of course, the economic outlook remains highly uncertain.”

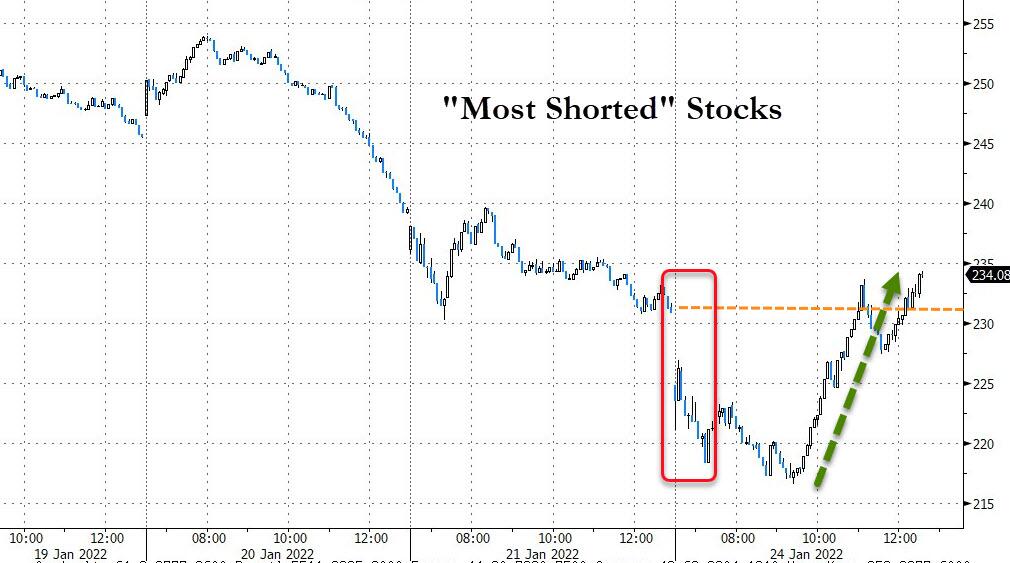

Bond yields spiked, as upcoming rate hikes are now a foregone conclusion with the 2-year ripping higher and scoring its biggest jump since March 2020 causing the US Dollar to surge and almost taking out its highest level for this year. That move took the starch out of gold, and the precious metal surrendered 1.94% but remained above its $1,800 level.

Please see section 3 below for the effect on our Trend Tracking Indexes.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}