- Moving the markets

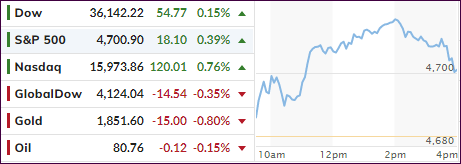

An initial bounce caused by strong October retail sales, as well as better-than-expected earnings report cards from Home Depot and Walmart, ran into some resistance mid-day, but the major indexes still managed to eke out a gain.

Leading the pack was the Nasdaq with a solid 0.76% advance, while the Dow lagged and barely stayed in the green. Traders took the above data as a sign that consumers are still in spending mode, however, their motivation may have been to buy now to avoid higher prices later.

The latest retail data showed that consumers increased their spending, as sales jumped 1.7%, a considerable increase from the prior month’s meager 0.8%. Online sales took top billing with an increase of 10.2% YoY, even though the CPI surged 6.2% YoY.

Despite the recent rut in the averages, MarketWatch noted that the Dow sits away from his record by 1.4%, while the S&P and Nasdaq hover within 1% of theirs.

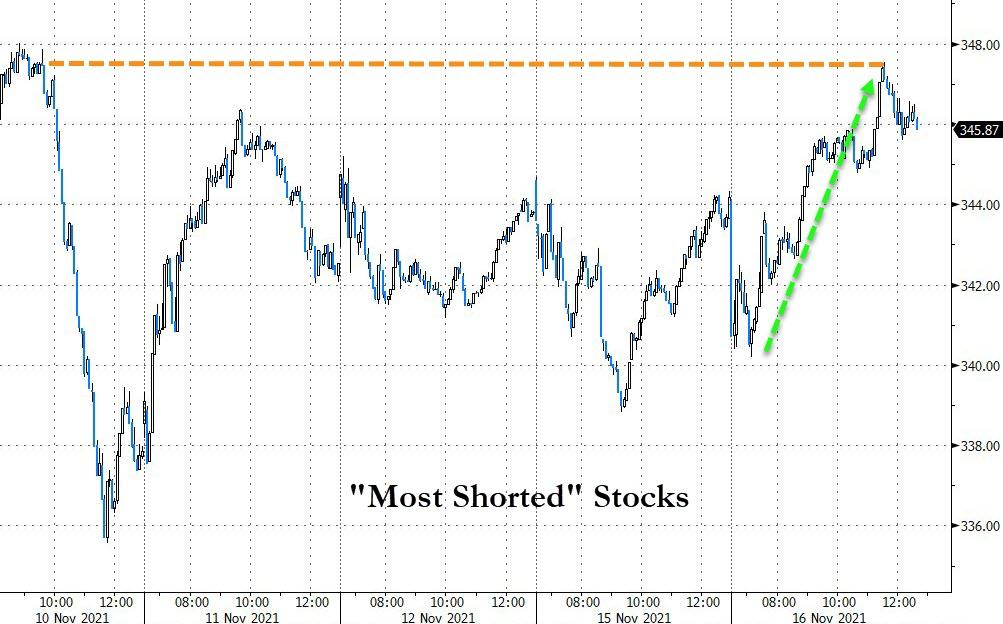

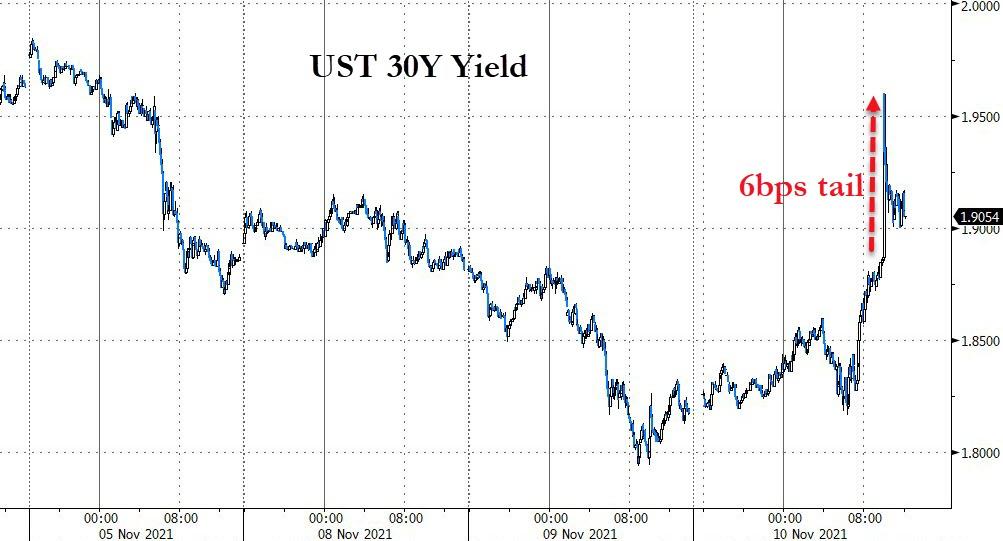

Today’s rebound was again helped by a short squeeze, which provided the much needed fuel to keep the markets on track for a green close, because bond yields continued their run. The 30-year again climbed above the 2% level but did not break out of November’s trading range—yet.

The US Dollar followed suit and touched a level last seen in September. None of these events proved beneficial to gold, so the precious metal slipped 0.79% but managed to successfully defend its $1,800 level.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}