- Moving the markets

Today’s session turned into another wild ride, when an early 350-point ramp in the Dow was wiped out, with major indexes retreating to their unchanged lines, only to see them as a springboard for a last hour rebound to intra-day highs.

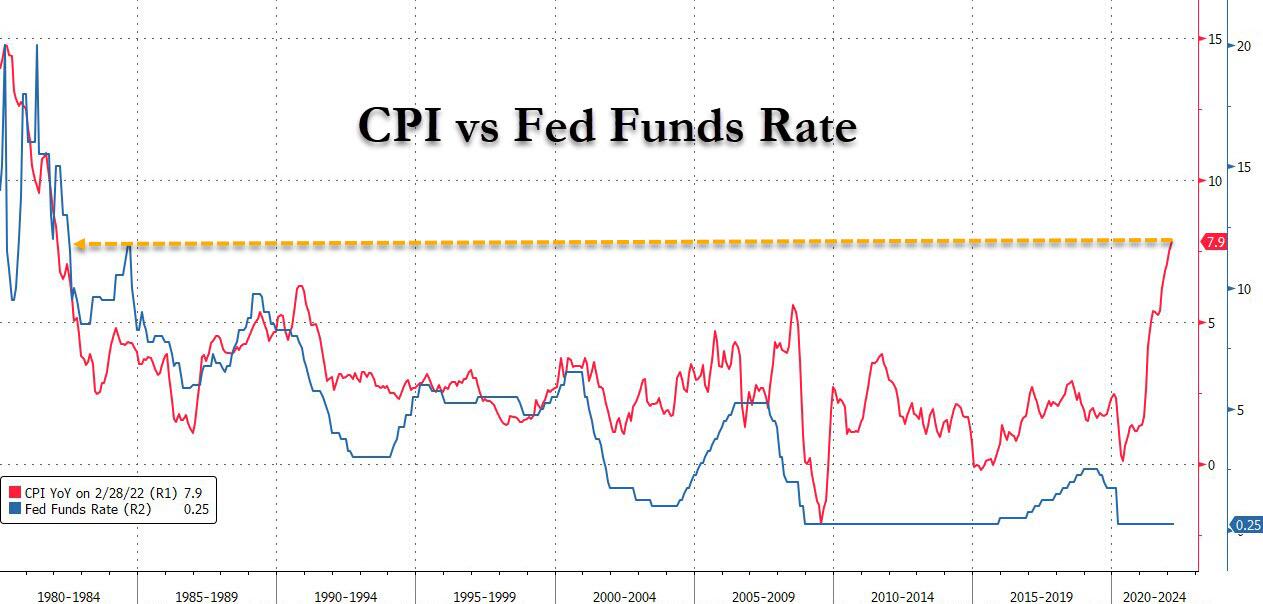

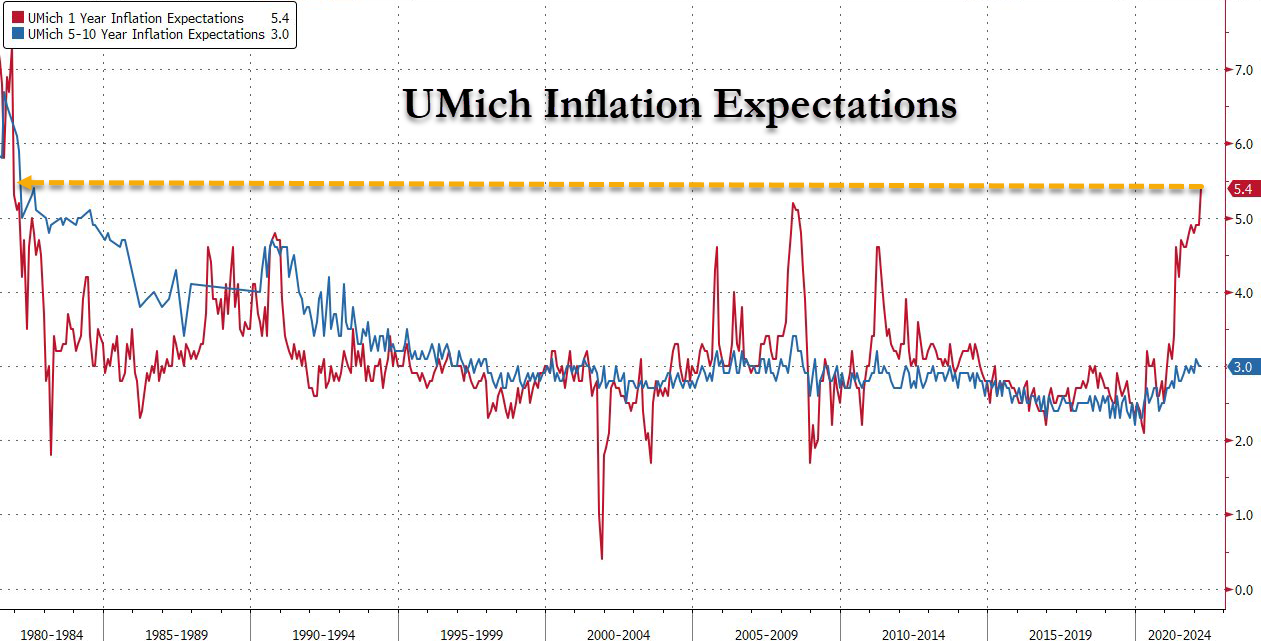

Today we learned that the Fed, as expected, raised their Federal Funds rate from zero to +0.25%, however, I could not find any explanation as to how that tiny change will fight 7.9% runaway inflation.

ZeroHedge added some color by explaining that the Fed is way behind the curve with any inflation fighting efforts, because the last time the CPI was at the current number (1982), the Fed Funds rate was at 13%, as this chart shows.

Makes me wonder how they possibly can expect that such a tiny hike will make a difference. Of course, it won’t, and we all know that any serious attempt to extinguish the inflation monster via a serious increase in rates would instantly prick the various bubbles and destroy the financial and real estate markets.

What caused the markets to stage a comeback late in the session? The Fed expects 6 more rate hikes in 2022, as did the market, or one at every meeting. Yet, once the word was out, rate hike odds plunged, and set the stage for the late rebound, which ZH explained this way:

Because with even the Fed now forecasting a big slowdown to growth coupled with a surge in inflation…

… the most likely outcome now is stagflation. This immediately manifested itself in a plunge in 30Y yields…

… culminating with the 5s10s inverting, a clear sign that a recession – the same recession which the Fed hopes to induce to crush commodity demand – is now coming.

… confirming that the Fed, which was trapped long before today’s rate hike, will be forced to ease and/or resume QE in the not-too-distant future even as inflation continues to rage. Translation: policy error.

In short, the more hawkish Powell gets, the bigger the liquidity firehose he will have to unleash in a few months when the economy plummets into an all-out recession, if not depression.

There is a good chance that, if markets continue to view this as a positive for stocks, we may find ourselves back in domestic equities—if only on a temporary basis, and before the bottom drops out.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}