- Moving the markets

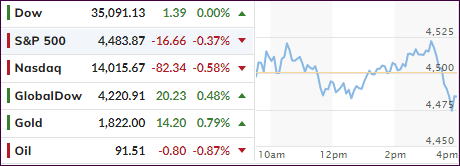

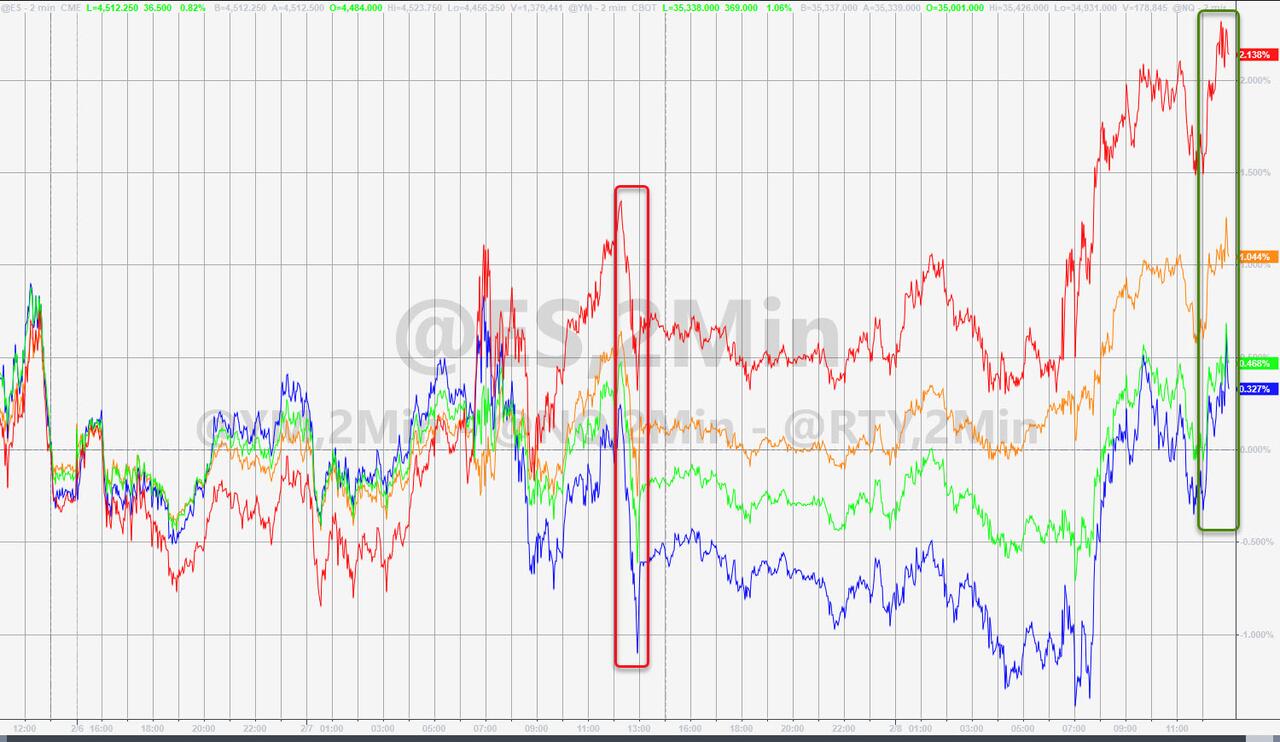

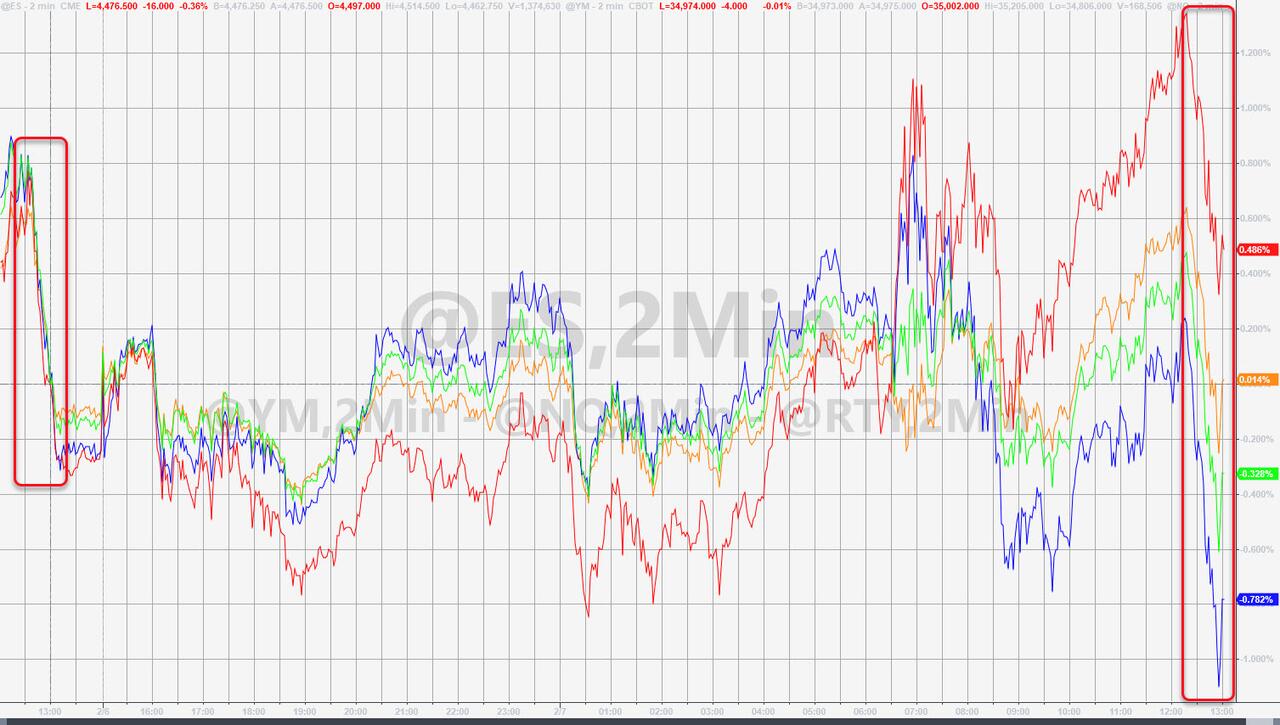

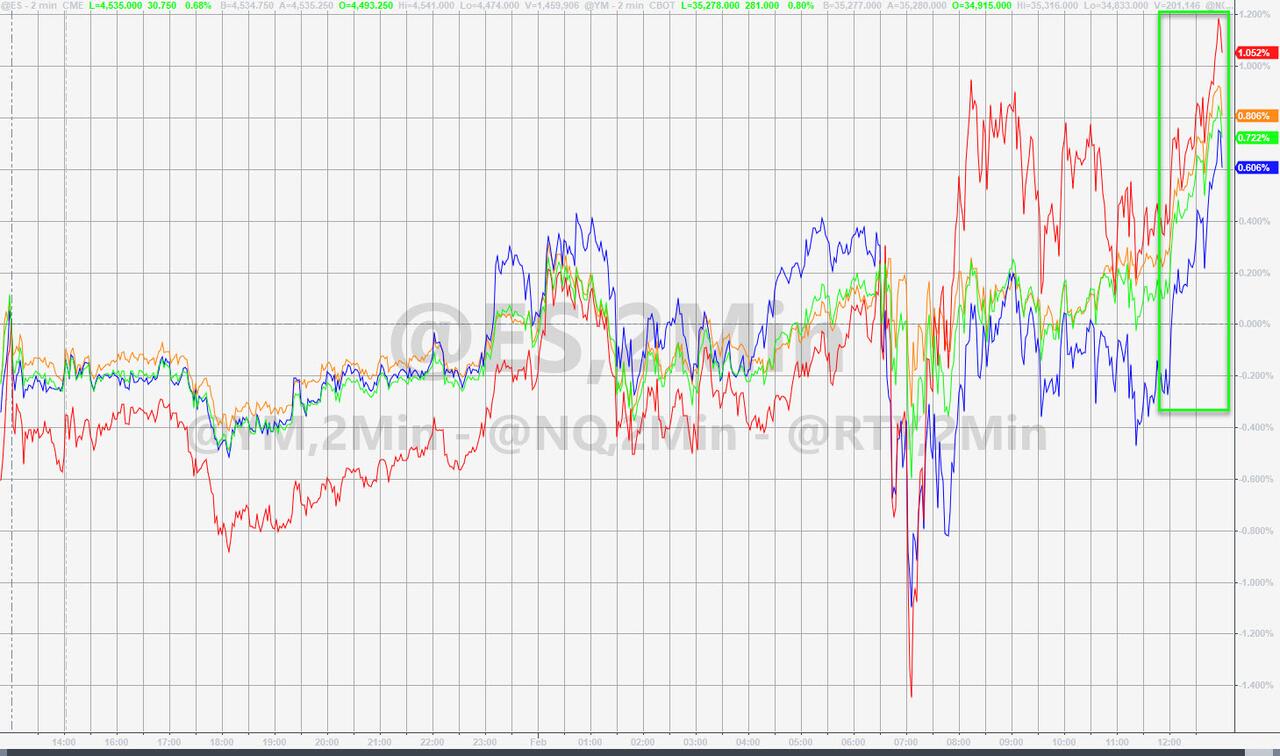

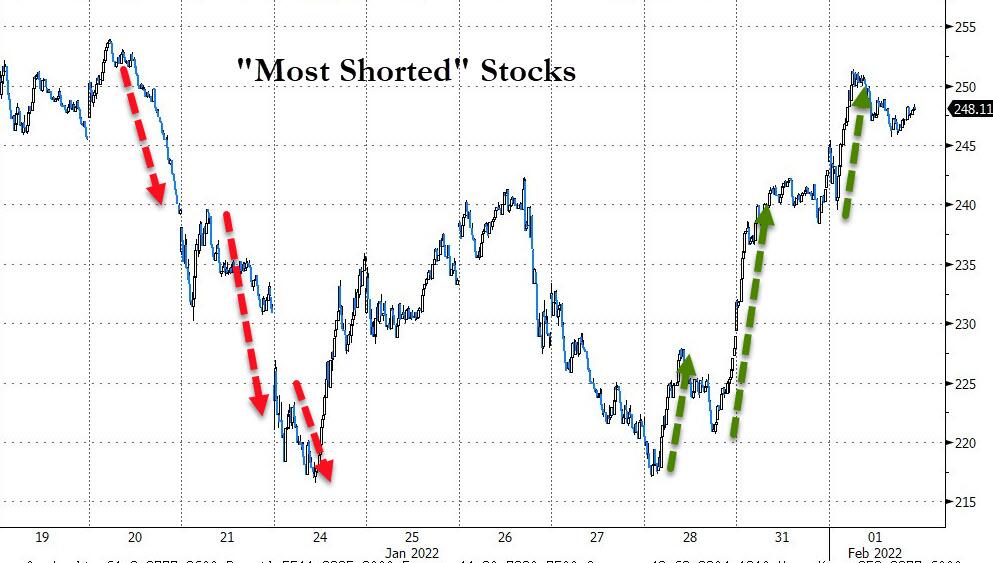

After several breakout attempts over the past two trading sessions, the market finally found some footing that served as a base for today’s last hour lift-a-thon and pushed the major higher without a late-day sell-off ruining another effort.

For a change, the rally was broad and led by the Nasdaq with the Dow in hot pursuit. Today’s driver turned out to be corporate earnings with Harley-Davidson reporting a surprise for the fourth quarter. Traders focused on value in the tech sector and the financials, the latter of which have greatly benefited by a steady rise in bond yields.

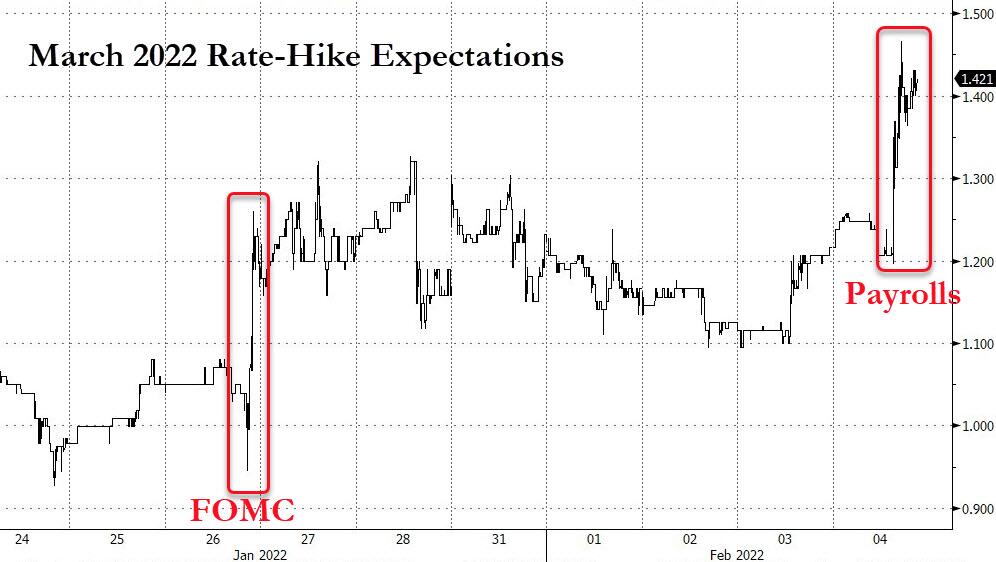

Despite today’s advance, equities will likely remain in a holding pattern prior to Thursday’s CPI release. Added MarketWatch:

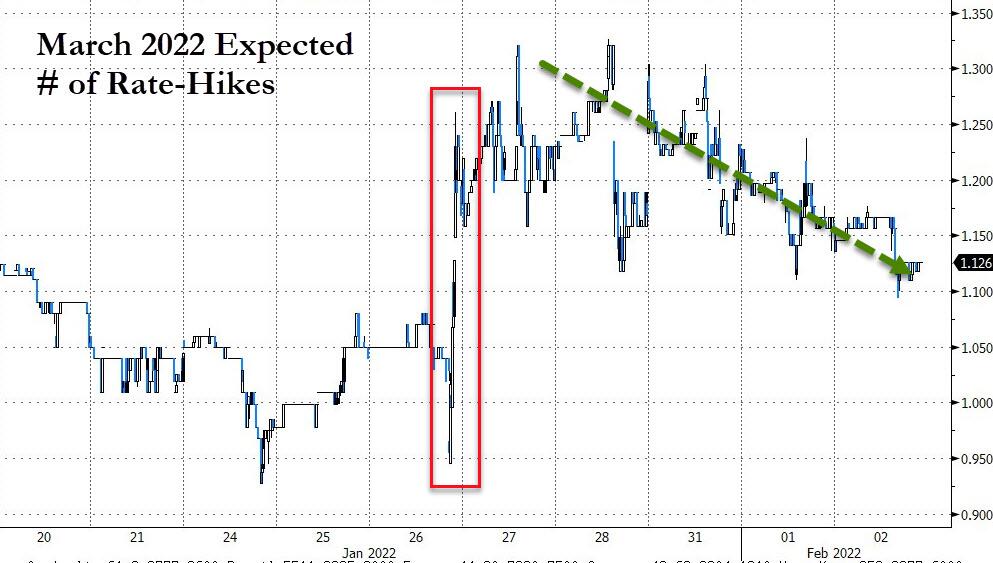

Wall Street is on edge watching how the Federal Reserve will react to the intensifying price pressures, with many investors eyeing Thursday’s consumer price index data release as a key event for markets this week. The inflation data is expected to show that prices rose 0.4% in January, for a 7.2% gain from one year ago, which would be the highest in almost 40 years.

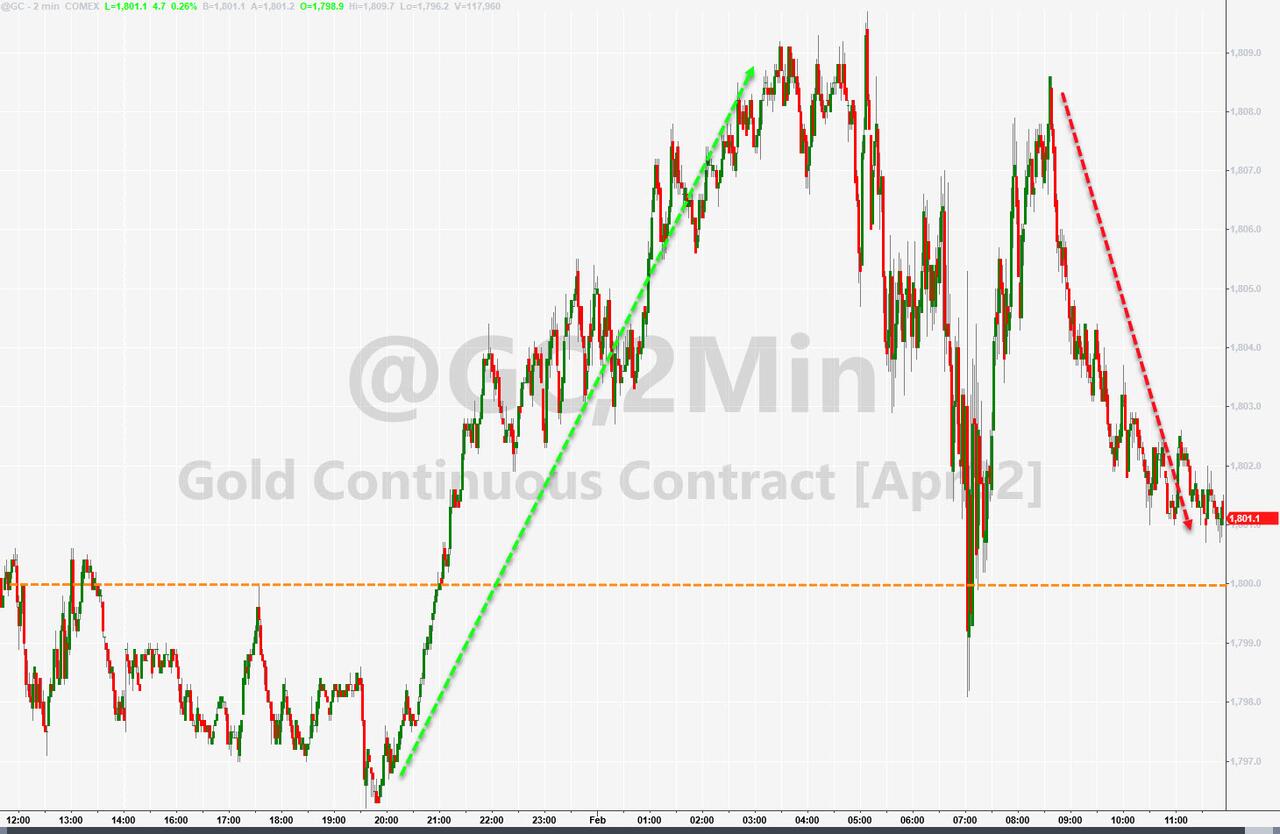

10-year bond yields spiked above the crucial 1.95% level to end then session at 1.96% with the psychologically important 2% level in danger to be broken. All other maturities were higher across the board as well.

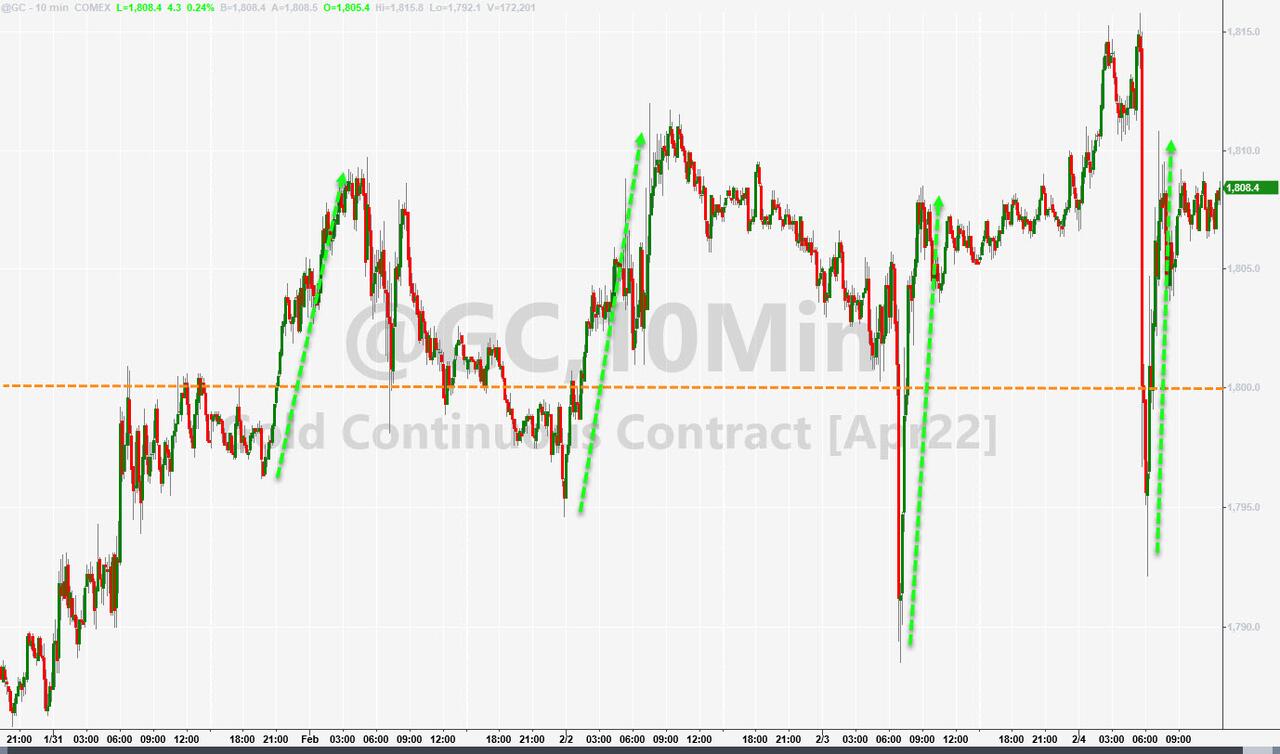

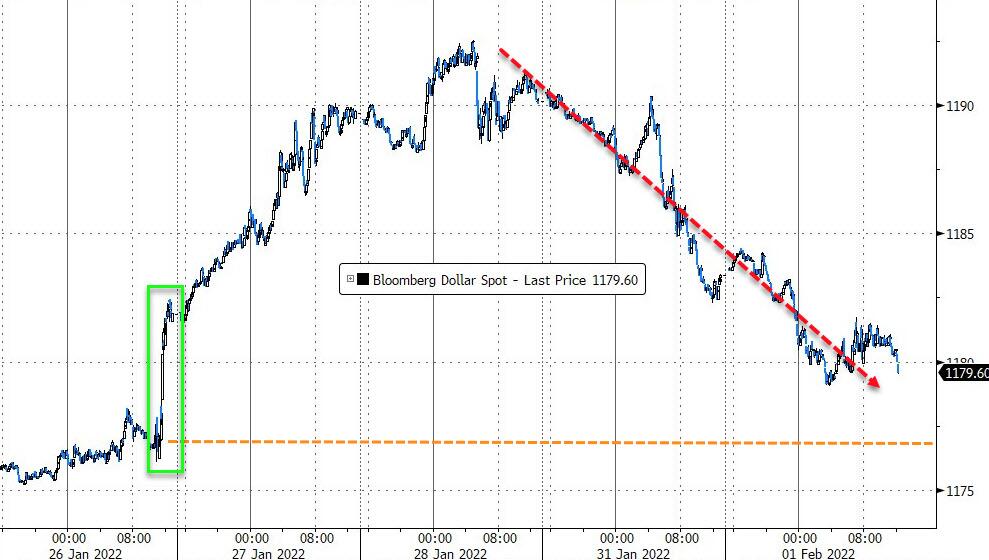

The US Dollar chopped around and closed marginally higher, while gold disregarded bond yields and a rising dollar and added 0.29% to solidify its position above the $1,800 level.

Most of today’s activity will not matter until the CPI is released on Thursday, the outcome of which will likely be determining future market direction. A better-than-expected reading will give the bulls more ammunition to ramp higher due to the then increasing likelihood of the Fed taking a more dovish stance towards future rate hikes. But the opposite will hold true as well.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}