- Moving the markets

Much of the July/August rebound from deep bear market territory was based on hope that the Fed will have to abandon its hawkish interest rate policy and “pivot” towards dovishness, which would result in lower rates and hence a continuation of the bullish theme.

While this pivot may eventually happen, it may not occur as quickly as anticipated. The Fed and its mouthpieces have in the recent past pounced on the reality that their inflation fight will continue, a fact that traders conveniently ignored.

Analyst Peter Schiff explained that the end to interest hikes has been pushed back, which is a negative for growth stocks for two reasons:

- It means higher interest rates. That is a big negative for growth stocks because it discounts their future earnings by a higher interest rate.

- If the Fed is going to have to stay higher for longer, that means the economy will be weaker for longer. That will weigh down earnings.

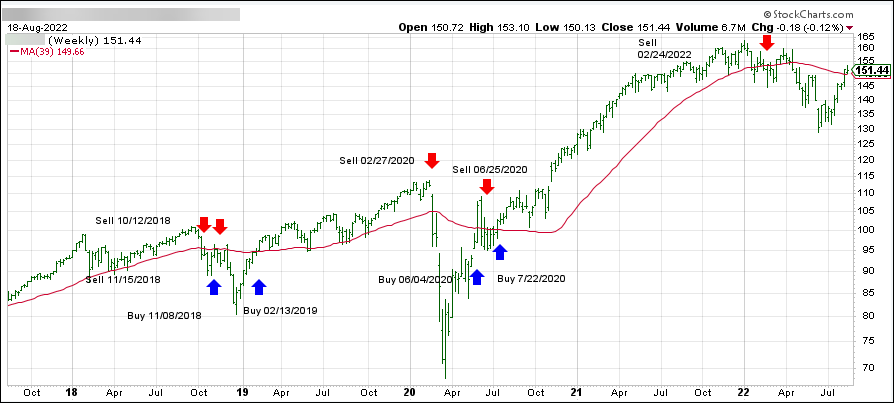

He thinks the sucker rally had ended and the primary trend (down) has resumed. I agree with his assessment as, technically speaking, our Domestic Trend Tracking Index (TTI) has plunged back into bear market territory (section 3.)

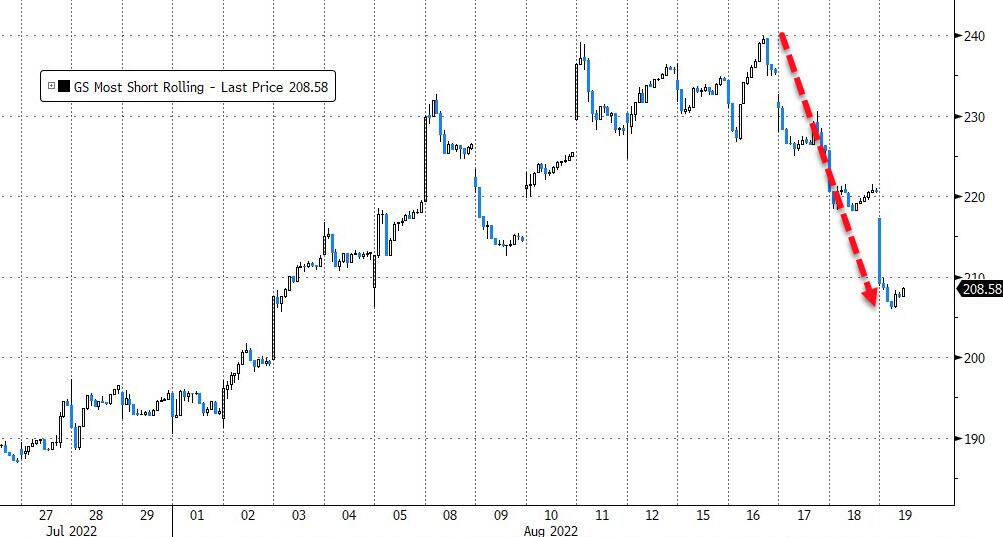

As a result, rate hike expectations are back at their highest since mid-July, as ZeroHedge pointed out, and subsequent rate-cut expectations have tightened as well.

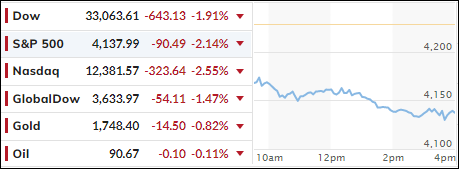

The major indexes took a dive, led by the Nasdaq, with all of them heading towards their 100-day M/As, after the 200-day M/As proved to be too much overhead resistance.

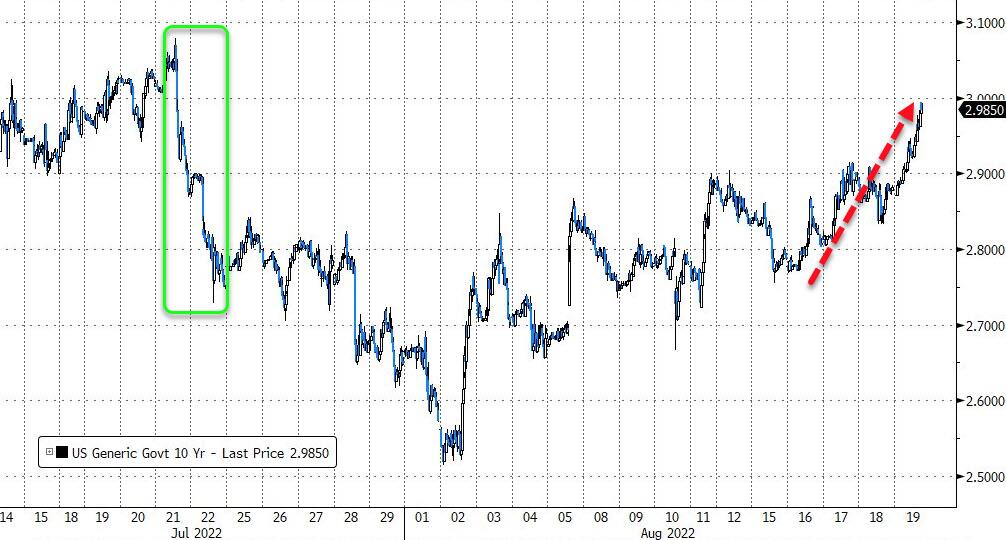

Bond yields climbed with the 10-year again conquering its 3% level and closing above it. The Euro crashed to its weakest against the US Dollar, which rallied to its highest close since June 2002, as ZeroHedge reported. Gold extended its losses below $1,800 due to the dollar’s strength.

The analog to 2008 appears to be on target—at least for right now.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}