Do you want to know which ETFs are hot and which ones are not? Then you need my High-Volume ETF Cutline report. It tells you how close or far each of the 311 ETFs I follow is from its long-term trend line (39-week SMA). These are the ETFs that trade more than $5 million a day, so they are not some obscure funds that nobody cares about.

The report is split into two parts: The winners that are above their trend line (%M/A), and the losers that are below it. The yellow line is the line of shame that separates them. You can see how many ETFs are in each group and how they have changed since the last report (275 vs. 278 current).

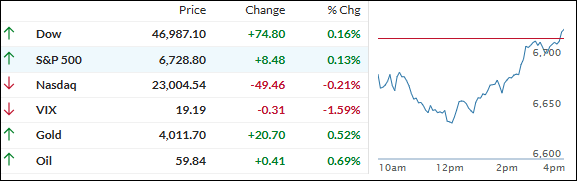

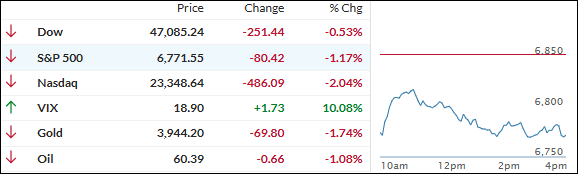

BITCOIN BOUNCES, GOLD RECOVERS—BUT STOCKS STAY IN THE RED

[Chart courtesy of MarketWatch.com]

Moving the market

Stocks stumbled out of the gate this week, with tech once again leading the decline. Big names in artificial intelligence took a hit, dragging the major indexes into the red.

Nvidia dropped another 3% Thursday, bringing its weekly slide to 10%. Oracle matched that loss, while Palantir sank 14% and Broadcom slipped 6%. Even Microsoft, Tesla, and AMD joined the selloff, weighing heavily on the broader market.

Adding fuel to the fire, October job cut data came in hot — marking the worst layoff numbers for that month in over 20 years. That makes 2025 the roughest year for job losses since the 2009 recession.

All three major indexes are down for the week, with the Nasdaq taking the biggest hit. Despite a late-week bounce, this was still its worst performance since the post–Liberation Day drop in April. Investors are growing wary of sky-high tech valuations and the increasingly narrow leadership in the market.

Still, there’s a glimmer of hope. A year-end rally could be on the table if the government shutdown wraps up and tariff tensions ease. Nvidia’s earnings report in two weeks might reignite the AI story — and if the Fed throws in a December rate cut, we could end 2025 on a high note.

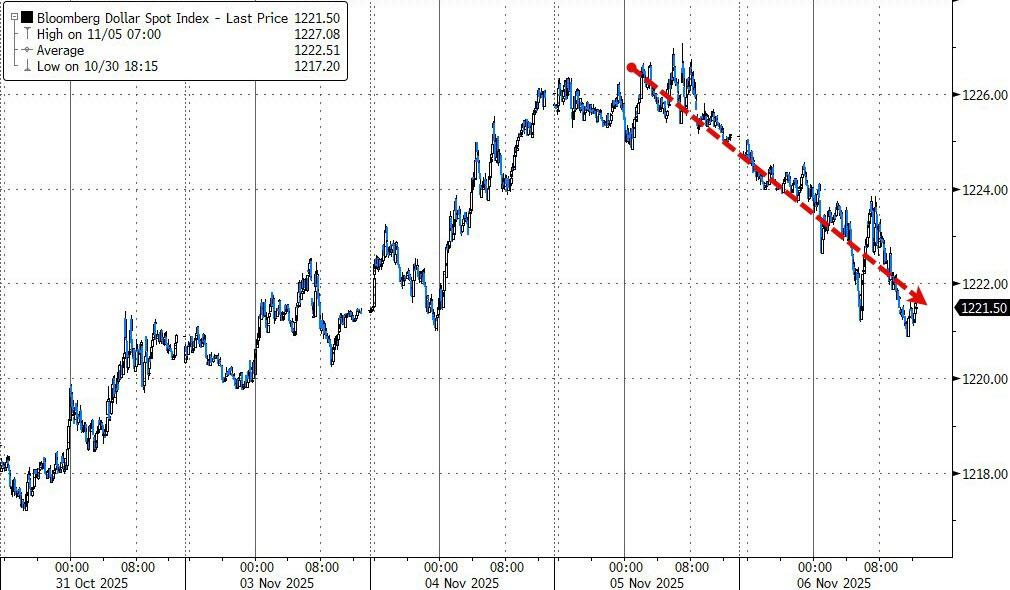

Meanwhile, bond yields dipped, the dollar paused, and bitcoin flirted with the $100k level before bouncing back above $103k. Gold, after two rough weeks, clawed its way back above $4,000.

So, with the week ending in the red, the big question is: Will next week’s economic data bring a turnaround—or are we in for more sideways action as the year winds down?

ETF Data updated through Thursday, November 6, 2025

How to use this StatSheet:

Out of the 1,800+ ETFs out there, I only pick the ones that trade over $5 million per day (HV ETFs), so you don’t get stuck with a lemon that nobody wants to buy or sell.

Trend Tracking Indexes (TTIs)

These are the main indicators that tell you when to buy or sell Domestic and International ETFs (section 1 and 2). They do that by comparing their position to their long-term M/A (Moving Average). If they cross above, and stay there, it’s a green light to buy. If they fall below, and keep going, it’s a red light to sell. And to make sure you don’t lose your shirt if things go south, I also use a 12% trailing stop loss on all positions in these categories.

All other investment areas don’t have a TTI and should be traded based on the position of each ETF relative to its own trend line (%M/A). That’s why I call them “Selective Buy.” In other words, if an ETF goes above its own trend line, you can buy it. But don’t forget to use a trailing sell stop of 12%, or less if you’re feeling nervous.

If some of these words sound like Greek to you, please check out the Glossary of Terms and new subscriber information in section 9.

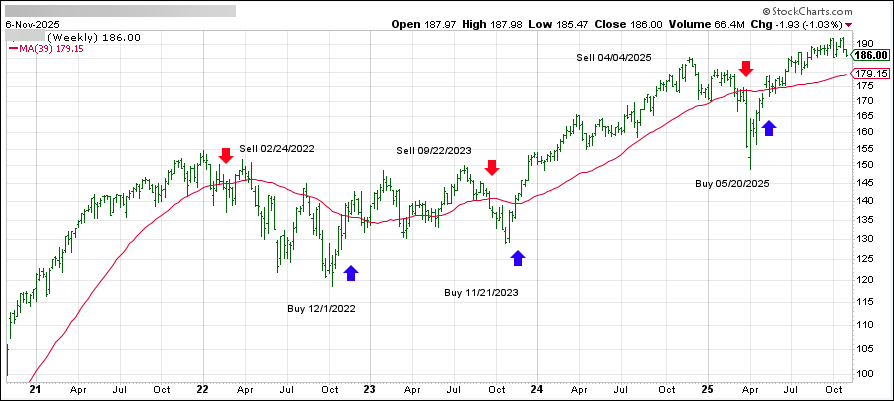

DOMESTIC EQUITY ETFs: BUY— effective 5/20/2025

Click on chart to enlarge

This is our main compass, the Domestic Trend Tracking Index (TTI-green line in the above chart). It has broken above its long-term trend line (red) by +3.95% and remains in “Buy” mode, with our new holdings being subject to our trailing sell stops.

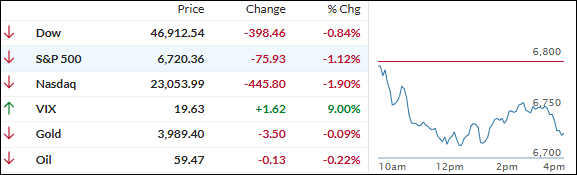

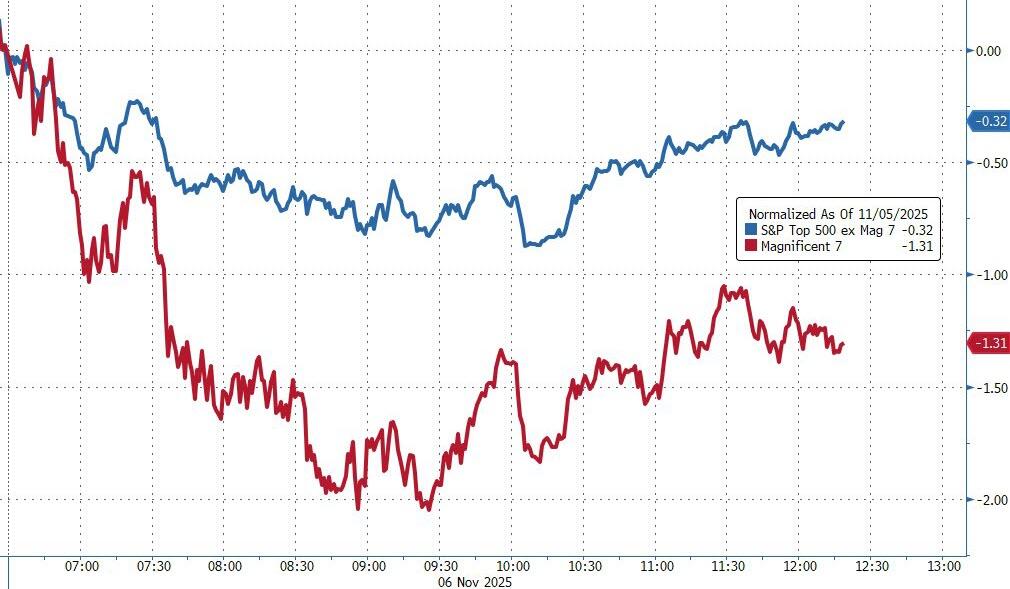

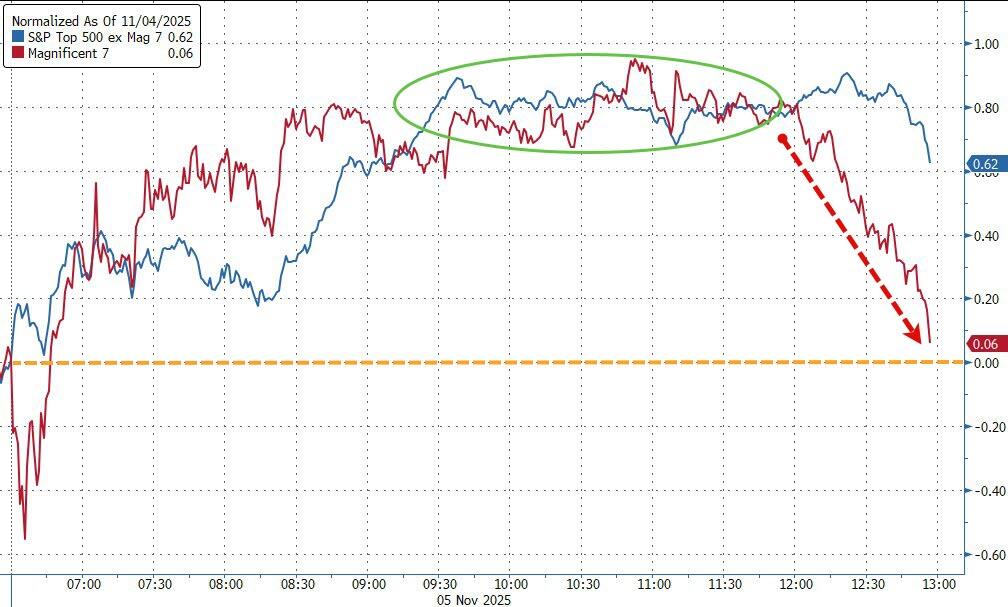

Stocks took a hit today, with the sell-off gaining steam as the session wore on. The usual suspects in the AI space were under pressure again, as investors grew increasingly uneasy about sky-high valuations.

Adding fuel to the fire were fresh concerns about the job market. October saw a wave of layoff announcements—over 153,000 job cuts, to be exact. That’s a whopping 183% jump from September and the worst October for layoffs in 22 years. In fact, 2025 is shaping up to be the roughest year for job losses since the 2009 recession.

AI stocks stayed in the spotlight. Qualcomm dropped 2%, despite beating earnings expectations. AMD, which had a strong showing yesterday, gave back 5%. Palantir and Oracle slipped 2% and 3%, respectively. Even Nvidia and Meta, two of the “Magnificent Seven,” couldn’t escape the downturn.

Meanwhile, traders kept one eye on Washington, where the Supreme Court is reviewing the legality of tariffs imposed during the Trump administration. Based on the justices’ comments, many expect a ruling that could roll back those trade taxes—potentially a bullish catalyst for stocks down the line.

But for now, sentiment stayed sour. Cleveland Fed President Beth Hammack made it clear that inflation is still public enemy number one. She said the Fed should keep tightening the screws to bring prices down, even if it means more pain in the labor market.

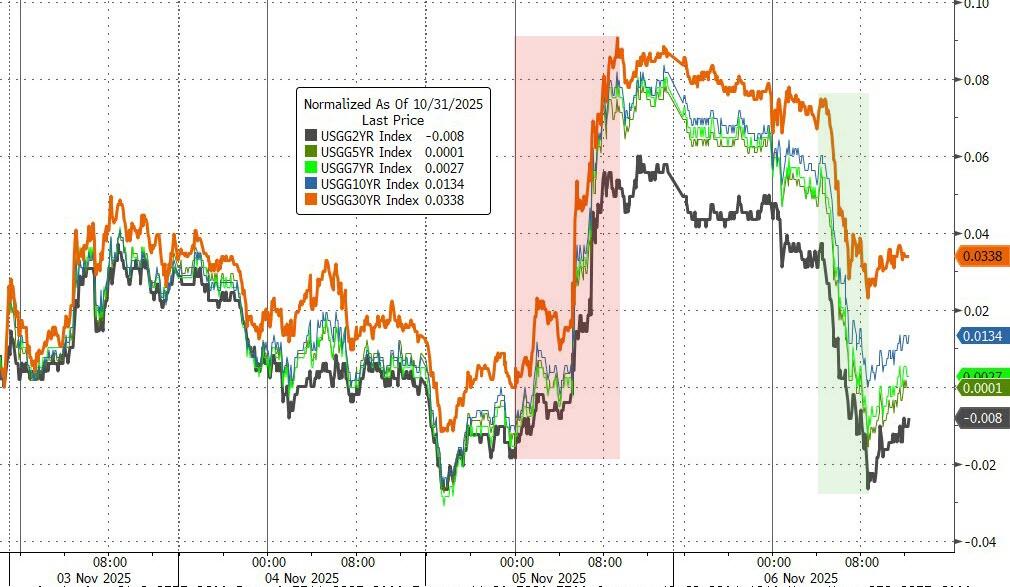

Tech stocks bore the brunt of the selling, with the Mag 7 once again lagging the rest of the S&P 500. Bond yields dipped, the dollar softened, and gold got a brief lift—but couldn’t hold the $4,000 mark. Bitcoin also slid with tech, though it found support around $101,000.

Some analysts think markets could bounce once the government reopens, but the odds of that happening by November 15 have dropped below 50%.

So, here’s the big question: Is this just a temporary shakeout, or are we looking at the start of a broader risk-off shift?

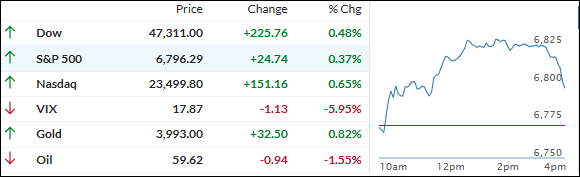

The major indexes snapped back from Tuesday’s shakeout, with buyers jumping back in and sending chipmakers like Advanced Micro Devices, Broadcom, and Micron Technology surging 3% to 6% as the broader artificial intelligence theme regained its footing.

Even Nvidia and Oracle managed to claw back some recent losses, hinting at fresh optimism in the high-flying tech sector.

The day’s rally came alongside some upbeat economic news: ADP payrolls and ISM services both topped expectations, signaling economic resilience.

That helped broaden out the gains, with positive breadth showing up across the market and small caps leading the way higher.

Meanwhile, the dollar’s recent climb paused, and bitcoin bounced off key support near $100,000.

Even though the Mag 7 basket lost some steam late in the day, the initial strength and improvement in market participation made for a more solid-feeling rally—at least for now.

Strong data also drove up bond yields, trimming odds of a third Fed rate cut in December. Gold nearly reclaimed its $4,000 mark, while silver pushed higher.

With the broader market joining in instead of just the AI favorites, will this turn into a more durable rally, or are traders just seizing another quick rebound before the next storm?

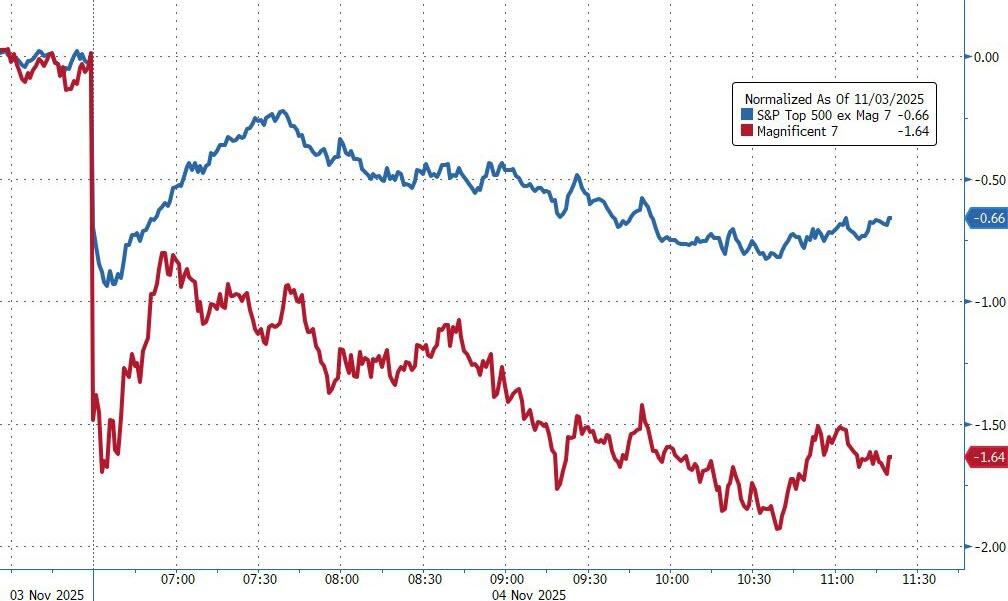

Stocks stumbled out of the gate today, dragged down by some of the biggest names in artificial intelligence.

Palantir took a 7% hit—even though it beat Wall Street’s Q3 expectations and offered strong guidance. The catch? Investors weren’t thrilled about the company’s lack of visibility for 2026, which left a sour taste.

Oracle slipped over 1%, trimming its impressive 50% gain this year. AMD, which has more than doubled in 2025, dropped more than 4%. Nvidia and other AI favorites also lost ground, adding to the pressure.

Adding fuel to the fire were some sobering comments from Wall Street heavyweights. Goldman Sachs CEO David Solomon warned of a possible 10–20% market pullback in the next year or two.

Morgan Stanley’s Ted Pick echoed the sentiment, saying we should be prepared for 10–15% drawdowns—even if they’re not triggered by a major economic shock.

Breadth was weak again, with over 300 stocks in the S&P 500 closing in the red. That’s raising eyebrows about how concentrated gains have been in just a handful of tech names.

And with November historically being a strong month for stocks, today’s across-the-board selloff—stocks, bonds, gold, silver, even bitcoin—makes you wonder if that seasonal strength is about to be tested.

The tech-heavy Mag 7 got hit harder than the broader market, while bond yields dipped and the dollar climbed to its highest level since May. Even alternative assets couldn’t catch a break.

So, with everything flashing red, the big question is: Are we seeing the start of a bigger sentiment shift—or will dip buyers swoop in and stabilize things before the week’s out?

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}