1. Moving the Markets

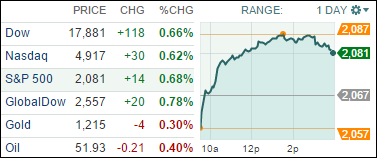

Stocks ended up higher after the release of minutes from the Fed’s meeting in March showed policymakers were divided on the timing of the first interest rate hike. The report remained consistent, however, with Fed policymakers’ forecasts that indicate the first hike in rates since 2006 is unlikely to take place before September.

Energy stocks and the oil were in focus today as oil prices slid on a build-up in U.S. inventories and a $70 billion oil merger was announced. U.S. benchmark crude fell 6% to close at $50.42 a barrel in New York after the Energy Information Administration reported a larger-than-expected increase in oil stockpiles last week. Chevron (CVX) dropped 1.7% and ExxonMobil (XOM) fell 2%.

In one of the largest corporate deals of the year, Royal Dutch Shell (RDS.A) agreed to buy Britain’s BG Group (BRGYY) for $70 billion in cash and stock. It is set to be one of the largest corporate deals of the year.

And earnings season began today with Alcoa (AA) reporting after the closing bell. Earnings beat estimates, but revenue was a shortfall. Wall Street analysts remain bearish on Q1 earnings and expect profits for S&P 500 companies to contract 2.8%.

8 of our 10 ETFs in the Spotlight manage to close up in this non-directional day. Consumer Discretionaries (XLY) was the winner with a gain of +0.94%, which was closely followed by Healthcare (XLV) with +0.84%. On the downside, DVY led with a modest loss of -0.19%.