ETF/No Load Fund Tracker StatSheet

————————————————————-

THE LINK TO OUR CURRENT ETF/MUTUAL FUND STATSHEET IS:

————————————————————

Market Commentary

MARKETS CLOSE QUIETLY HIGHER IN ANTICIPATION OF FED DECISION

1. Moving the Markets

Wall Street’s last session of the week was marked by a cautious tone, with stock prices cutting early losses and ending higher as traders awaited next week’s key decision on interest rates from the Federal Reserve. Traders’ trepidation over whether or not the Fed will hike rates for the first time in more than a decade when it breaks from its two-day policy meeting Thursday has Wall Street playing it conservatively and safe today. No one is willing to make a big bet ahead of the closely watched decision.

Adding to the angst on Wall Street of late was a research report from Goldman Sachs today that said there is a chance for U.S.-produced crude oil to dip as low as $20 a barrel due to persistent oversupply and lower demand expected from slowing emerging market economies. Oil prices have dropped in half over the last 12 months as the market adjusts to a global surplus and an economic slowdown in China. The emergence of new sources of oil from the U.S., where producers are tapping shale reserves, has also fueled the recent decline.

After a month of volatility and an announcement it will close dozens of under-performing stores, Macy’s (M) announced earlier this week that it will soon open Best Buy (BBY) shops within some of its department stores as a way to test selling consumer electronics. The rollout will begin in 10 Macy’s stores across the country starting in November. Macy’s Inc. President Jeff Gennette said that the companies will test the stores through the holidays and into 2016 before deciding on the next steps.

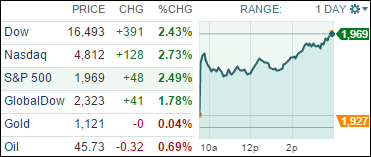

All of our 10 ETFs in the Spotlight inched higher as the indexes vacillated within a trading range. The bias was up, however, with the leader of the day being Consumer Discretionaries (XLY), which added +0.75%, while the Global 100 (IOO) lagged with +0.17%.