1. Moving the Markets

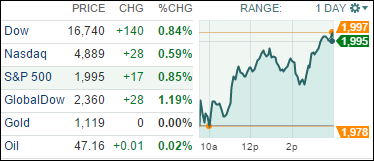

Stocks rallied Wednesday afternoon with the Dow gaining 140 points on the day, after the Federal Reserve kicked off its long-awaited 2-day policy meeting on interest rates. In one of the most important Fed meetings in recent times, economists and analysts alike are divided on whether the Fed will move forward to raise interest rates.

A quarter of a percentage point boost in the fed funds rate likely would marginally push up borrowing costs for consumers and businesses, including mortgages, car loans and corporate bonds, tempering such borrowing and, as a result, economic activity. However, some economists say it’s time to start gradually raising rates for the first time in nearly a decade given that the U.S. job market has allegedly more or less recovered. Others argue rates should remain on hold amid global stock market turmoil and China’s slowdown, among other factors. Which side will win out? We’ll find out tomorrow.

On the earnings front, FedEx (FDX) reported quarterly profit of $2.42 per share, which was 4 cents below estimates, with revenue matching forecasts. CEO Fred Smith said the company is doing well considering weaker than expected global economic conditions. Separately, FedEx will increase rates by 4.9% at its FedEx Express service, which will take effect on Jan.4. The stock closed down 2.84%. Also, Oracle (ORCL) gained slightly today after the company beat analysts’ earnings forecasts but posted disappointing revenue numbers in its first fiscal quarter earnings report. The main problem, it seems, is that software license sales are falling as the tech world shifts to Web-delivered cloud products.

All of our 10 ETFs in the Spotlight stayed with this week’s upward momentum and closed higher. The winner of the day was the Mid-Cap Value ETF (IWS) with +1.24%, while the laggard was Healthcare with +0.28%.